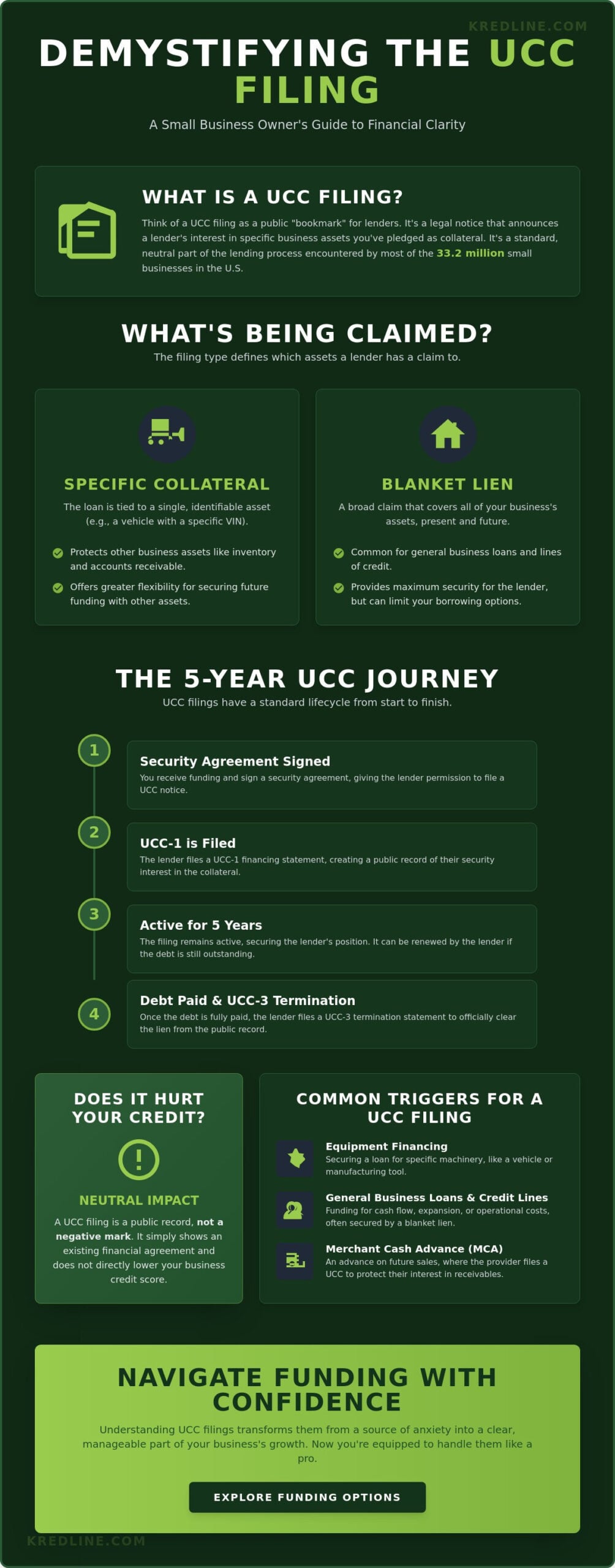

What if a three-page document you signed months ago is the only thing standing between you and your next round of growth capital? You likely remember the relief of securing your last loan, but the legal paperwork that followed probably felt like background noise. It’s completely normal to feel a surge of anxiety when you spot a ucc filing on your business credit report, especially if you worry about losing control over your equipment or inventory. Most of the 33.2 million small business owners in the U.S. encounter these documents at some point, yet few are given a clear explanation of what they actually mean for their future.

We believe that financial clarity shouldn’t be a luxury reserved for corporate lawyers. In this guide, we’ll strip away the legalese to show you exactly how these filings work and why they’re a standard, healthy part of the lending process. You’ll learn the practical differences between a UCC-1 and a UCC-3, how the five year expiration cycle affects your credit, and the exact steps to take to ensure a filing is removed once your debt is paid. By the end, you’ll have the peace of mind to treat these filings as what they truly are: a bridge to your next business milestone.

Key Takeaways

- Learn how a ucc filing acts as a public “bookmark” for lenders, signaling which business assets are currently pledged as collateral.

- Understand the distinction between specific collateral and blanket liens to see how much control you retain over your business’s equipment and inventory.

- Find out why these filings are considered neutral records rather than negative marks, and how they truly impact your business credit score.

- Discover the necessary steps to officially “terminate” a filing after your debt is paid to ensure your public record is accurately updated.

- Gain the confidence to navigate new funding opportunities by learning how to evaluate the fine print in any security agreement.

Understanding the Basics: What Is a UCC Filing?

If you’ve ever applied for business funding, you might’ve heard the term “UCC filing.” It sounds like dense legal jargon, but the concept is actually quite straightforward. A ucc filing is a legal notice lenders use to announce their interest in a business asset. Think of it as a public bookmark. It tells other creditors which assets you’ve already pledged as collateral so they don’t try to claim the same property. A UCC-1 is a public notice filed by a creditor to protect their security interest in a debtor’s property. This document is the most common form you’ll encounter, and it typically stays active for five years unless the lender chooses to renew it.

When you sign a security agreement, you’re giving a lender permission to file this notice. It doesn’t mean they own your equipment or inventory. Instead, it means they’re first in line to get paid if things don’t go according to plan. Having this record in the public domain creates a transparent environment where lenders can see exactly what’s available for collateral before they approve a new request. It’s a standard part of the commercial lending world that helps keep the wheels of business moving smoothly.

The Purpose of the Uniform Commercial Code

The Uniform Commercial Code was first published in 1952 to solve a major headache for American businesses. Before it existed, every state had its own set of rules for contracts and debt, which made doing business across state lines incredibly risky and complicated. The UCC created a consistent framework that makes interstate commerce predictable. This protects the lender by ensuring they won’t lose their claim to collateral just because a business moves to a different state. It also helps you as a borrower by clarifying the terms of your debt. Most of these public records are managed by the Secretary of State, making it easy for any professional to verify a company’s financial obligations quickly.

Common Scenarios That Trigger a Filing

Lenders use a ucc filing to manage their risk whenever they provide significant capital. You’ll usually see one pop up in these specific situations:

- General Business Financing: If you’re securing a short-term business loan or a line of credit to manage cash flow, the lender will likely file a “blanket lien” on all your business assets.

- Equipment Financing: When you finance a specific piece of machinery, like a $60,000 CNC machine or a delivery van, that specific item acts as the guarantee. The lender files a notice specifically for that asset.

- Alternative Funding: Entering into a merchant cash advance agreement often triggers a filing to protect the provider’s interest in your future sales.

Understanding these triggers helps you stay in control of your business’s financial profile. It’s not a sign of trouble; it’s simply a record of a professional partnership between you and your funding provider.

Specific Collateral vs. Blanket Liens: What Is Being Claimed?

The impact of a ucc filing depends entirely on what the lender lists in the “collateral” section of the form. This part of the document defines exactly which parts of your business the lender has a claim to if you can’t repay the debt. It’s the difference between a lender having a key to one specific truck or a key to your entire building. If you don’t check these details, you might accidentally limit your ability to get more funding later.

Most business owners encounter two main types of claims. Specific collateral filings are surgical and precise, while blanket liens are broad and all-encompassing. According to a UCC filing guide from Forbes, these public notices serve as a “first in line” marker for creditors, making the scope of the collateral a critical detail for your balance sheet.

When Specific Collateral Makes Sense

Specific collateral filings are the standard for equipment funding. In these cases, the loan is tied to a single, identifiable asset like a delivery van, a CNC machine, or a commercial pizza oven. The filing will usually include a specific VIN or serial number to identify the item. This is a cleaner way to borrow because it leaves your other assets “free” or unencumbered.

- Asset Protection: Your accounts receivable, inventory, and other equipment remain untouched.

- Future Flexibility: You can still use your other assets as leverage for a different loan next month.

- Lower Risk: If you default, the lender only has a right to that specific piece of equipment.

Specific collateral filings are generally less restrictive for growing businesses because they don’t lock up your entire company’s value. This allows you to scale by adding new equipment through different lenders without those lenders tripping over each other’s claims.

The Reality of Blanket Liens

Blanket liens are much more common than many owners realize. Lenders use them when there isn’t one high-value piece of equipment to act as security. Instead, they take a “blanket” interest in almost everything the business owns: your inventory, your equipment, and even your bank accounts. This is the standard procedure for revenue-based financing, where the lender is securing their right to your future sales rather than a physical machine.

The practical impact isn’t that the lender owns your stuff; you still use your equipment and sell your inventory every day. It just means you can’t sell off those assets or close the business without the lender’s consent. Since these liens cover so much ground, they can make other banks hesitant to work with you until the original debt is settled. If you’re curious about how these filings might affect your current setup, you can prequalify for business funding to see which options fit your specific asset structure.

Does a UCC Filing Hurt Your Credit or Future Funding?

A common misconception among business owners is that a UCC filing acts like a tax lien or a court judgment. It doesn’t. In the world of commercial finance, a filing is a neutral public notice. It simply states that a lender has a legal interest in certain assets you’ve used to secure a loan. It’s a sign of active capital management, not a signal of financial distress. Most lenders view an active filing as proof that your business is established enough to qualify for professional financing.

Your business credit score typically remains unaffected by a filing as long as your payments stay on schedule. For those asking What is a UCC filing? in the context of credit health, it functions much like a mortgage record on a home. It’s a transparent part of doing business. Problems only arise if a “default” is recorded, which happens when payments stop. Otherwise, having a history of satisfied filings can actually help you secure larger loan amounts in the future because it proves you can handle significant debt obligations.

The real challenge with a ucc filing isn’t the credit score; it’s the “stacking” concern. If you already have three or four active filings, a new lender might worry that your cash flow is stretched too thin. They want to ensure they aren’t the fifth person in line to get paid if things go south. However, if your revenue is strong, most lenders will see this as a sign of a growing, ambitious company rather than a risk.

Impact on Business Credit Reports

Filings appear on reports from Experian Business, Equifax, and Dun & Bradstreet. You might see multiple entries for the same loan if a lender filed an amendment or a “continuation” to extend the five-year term. It’s important to distinguish between an active filing and a defaulted lien. An active filing shows you’re currently utilizing capital. A defaulted lien shows you failed to pay. If you see old, paid-off filings still listed as active, you should contact the lender to file a UCC-3 termination statement immediately to clean up your profile.

Navigating Future Funding Requests

When you apply for new capital, transparency is your best tool. If a new lender sees an existing ucc filing, they might ask for a “subordination agreement.” This is a simple document where your current lender agrees to let the new lender move to the front of the line for specific assets. Being upfront with your broker about existing debt speeds up the approval process by days. If you find yourself managing too many separate payments, you can use a business line of credit to consolidate those smaller debts. This allows you to pay off multiple lenders, clear their filings, and leave yourself with one clean, manageable record.

How to Remove or Amend a UCC Filing

Paying off your debt is a huge milestone for your business. However, a common misconception is that a ucc filing automatically vanishes the moment your balance hits zero. It doesn’t. Think of it like a lien on a house; the record stays public until a specific document is filed to clear it. To ensure your credit report and asset records are clean, you must go through the formal termination process.

The first step is verifying your balance is exactly zero. Request a formal payoff letter from your lender. This document is your primary evidence that the obligation is met. Second, ensure the lender files a UCC-3 Termination Statement with the Secretary of State. While many lenders do this automatically, some might overlook it in their administrative queue. Finally, follow up after 30 days. Use your state’s online business registry to confirm the status has changed to “lapsed” or “terminated.”

What Is a UCC-3 Statement?

A UCC-3 is a multi-purpose form used to update the original filing. Lenders use it for three main reasons. They file a “continuation” if the debt isn’t paid within 5 years, as filings expire after that period. They use “amendments” to fix typos or change collateral details. Most importantly, they use “terminations” to end the lien. If you spot an incorrect ucc filing on your record, an amendment or termination is the only way to legally correct the public record.

DIY Termination: Can You File It Yourself?

You might feel tempted to file the termination yourself if a lender is slow. Don’t do this without express written consent. Filing without authorization is considered a “wrongful termination,” which can lead to legal penalties or damage your relationship with future creditors. Instead, use the law to your advantage. Under UCC Section 9-513, most states require lenders to file a termination within 20 days of receiving a formal written demand from the borrower.

If a lender refuses to act, send a formal “Information Demand” via certified mail. This starts the 20-day clock and provides a paper trail. Keeping your record clear is vital when you want to prequalify for business funding for your next project. A lingering filing can slow down new approvals, so staying proactive pays off. We can help you look at your options once your records are clear.

Navigating Business Funding with Confidence

A ucc filing shouldn’t be a source of anxiety for a growing company. It’s a standard part of the financial landscape. Many business owners see the word “lien” and immediately worry about their credit or their control over the business. In reality, these filings are simply tools that allow lenders to provide the capital you need for inventory, payroll, or expansion. If you understand the terms, you can use these tools to your advantage without any surprises down the road.

Our team at Kredline acts as your navigator through this process. We help you look past the sales talk and focus on the fine print of any security agreement. It’s about transparency. You deserve to know exactly which assets are at stake before you commit to a new source of capital. By understanding the mechanics of these agreements, you can make decisions that protect your long-term interests while fueling your immediate growth.

Reviewing Your Funding Options

Not all funding products treat your assets the same way. A merchant cash advance (MCA) often requires a blanket lien, which covers nearly all business assets. In contrast, a short-term business loan or equipment financing might only name specific pieces of machinery or a single bank account. Comparing these offers side-by-side is the only way to avoid over-collateralizing your business.

Working with a broker provides a distinct advantage here. We often find “UCC-light” options for businesses that already have existing debt. If a primary lender already has a blanket lien, we can help you find secondary funding that works around those existing restrictions. Always ask one specific question before signing: “What specific assets will be named in the UCC-1?” If the answer is “everything,” you need to decide if the capital is worth that level of exposure.

Next Steps for Your Business

Your first step should be a proactive review of your business credit reports. Data from industry analysts suggests that a significant number of reports contain “zombie” filings. These are old ucc filing records that remain active even after the debt is paid in full. If you find one, contact the lender immediately to request a UCC-3 termination statement. This simple cleanup can instantly make your business more attractive to future lenders.

Once your records are clean, you can use Kredline to explore funding that fits your current asset structure. We help you prequalify for business funding without the stress of hidden “gotchas” or aggressive legal language. Think of a UCC filing as a signpost on the road to a larger, more successful company. It’s a mark of a business that’s active, borrowing, and building for the future. With the right partner, you can sign those agreements with total peace of mind.

Take Control of Your Business Credit and Growth

Understanding a ucc filing doesn’t have to be a headache. It’s simply a public notice that a lender has an interest in your assets. While a blanket lien can limit your immediate borrowing capacity, specific collateral filings offer more flexibility for equipment or inventory purchases. The most important thing is keeping your records clean and ensuring old filings are terminated within 30 days of debt repayment. This proactive approach keeps your business ready for its next big opportunity.

Navigating the world of commercial finance is easier with a partner who prioritizes clarity over confusion. Kredline provides broker-led transparency and direct access to a national network of over 50 third-party lenders. We focus on business-first solutions, so you won’t face the personal loan pressure common at traditional banks. It’s about finding the right fit for your cash flow without the unnecessary stress or complex jargon.

Prequalify for funding and see your options in minutes

You’ve got the knowledge to protect your credit and manage your liens. Now it’s time to focus on what you do best: running your business.

Frequently Asked Questions

Is a UCC filing the same as a lien?

Yes, a UCC filing is a legal lien that lenders use to announce their claim against your business assets. It serves as a public notice to other creditors that specific property, like your machinery or inventory, is being used as collateral for a loan. It’s very similar to how a bank holds a lien on a car title until the auto loan is fully paid off.

How long does a UCC-1 filing stay on my record?

A standard filing remains active for 5 years from the date it’s recorded with the Secretary of State. If the debt isn’t settled within that window, lenders usually file a continuation statement during the 6 month period before the expiration date to keep the lien active for another 5 years. Once you’ve paid the debt, the lender should file a UCC-3 termination statement to remove the record.

Can I get a business loan if I already have an active UCC filing?

You can still qualify for financing, but it depends on the type of assets you’ve already pledged and the new lender’s risk tolerance. Many lenders are comfortable taking a second position behind an existing ucc filing, though they might offer different terms to account for the increased risk. At Kredline, we help business owners navigate these situations by reviewing their current debt to find the most efficient path to new working capital.

Do UCC filings affect my personal credit score?

These filings generally don’t appear on your personal credit report because they’re registered against your business entity. However, if you’ve signed a personal guarantee and the business fails to pay, the default will eventually impact your personal score. Since about 90% of small business loans involve some personal liability, it’s vital to stay on top of your business obligations to protect your own credit standing.

What happens to a UCC filing if my business closes or files for bankruptcy?

The filing stays in place and dictates the order in which creditors are paid from your remaining assets. In a bankruptcy scenario, a creditor with a perfected ucc filing is considered a secured creditor, meaning they’re first in line to collect value from the collateral listed in the filing. Unsecured creditors, who don’t have these filings, only receive payment if there’s money left over after all secured debts are satisfied.

How much does it cost to remove a UCC filing?

The state filing fees for a termination statement are usually quite low, typically ranging from $5 to $30 depending on your location. While the government fee is minimal, some lenders might charge a small administrative fee to process the paperwork. You should check your original loan agreement to see if these costs were outlined when you first took out the funding.

Can a lender file a UCC-1 without my knowledge or consent?

Lenders can’t legally file without your permission, but that consent is almost always included in the loan documents you sign. Most owners don’t realize they’ve agreed to it until they see the notice on a credit report or when they’re working with a resource like Kredline to prequalify for a new line of credit. It’s a standard practice in the industry for almost any type of secured business funding.

What is a “purchase money security interest” (PMSI) in a UCC filing?

A PMSI is a special type of filing that gives a lender first priority over a specific piece of equipment you just bought, even if another lender already has a blanket lien on your business. For example, if you finance a $45,000 forklift, the equipment lender can file a PMSI to ensure they’re the first to claim that specific forklift if you default. This is a common way for businesses to acquire new tools without violating existing loan agreements.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.