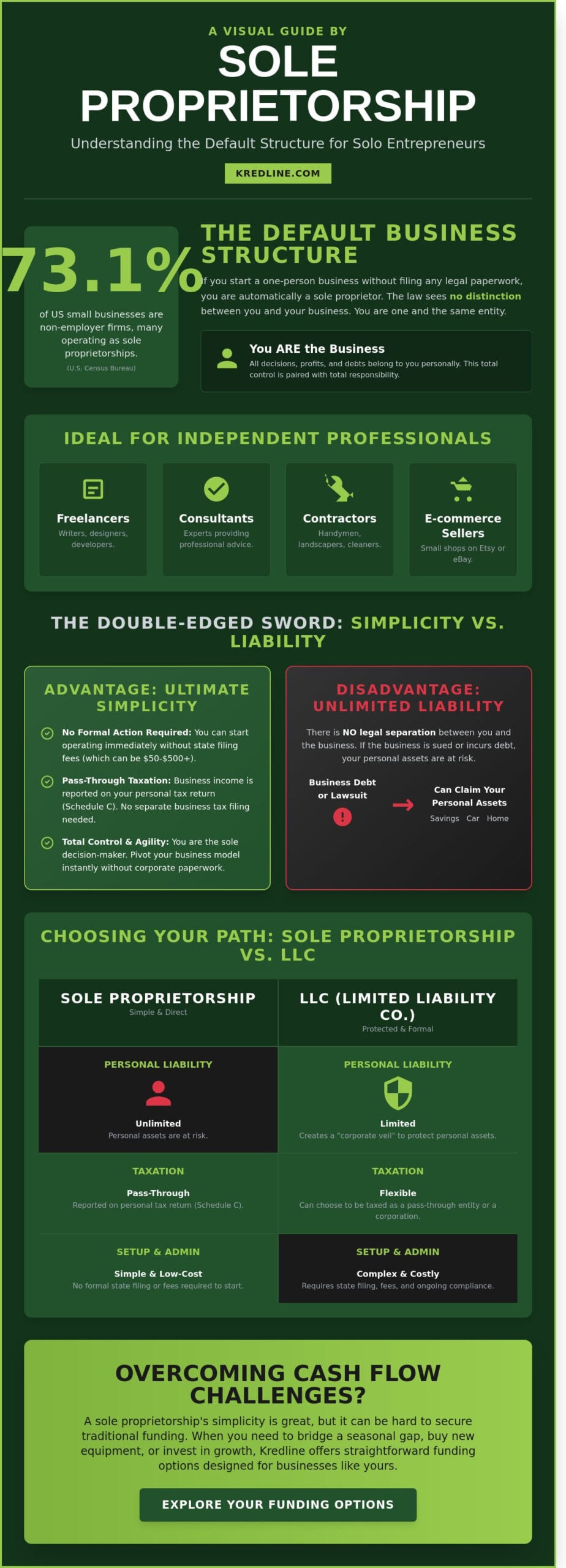

Last Tuesday, Sarah, a freelance graphic designer, realized her personal savings account was also her business’s only safety net. It’s a common realization for the 73.1% of US small businesses that operate as non-employer firms according to Census Bureau data. When you’re the only one calling the shots, the freedom is great, but you’re probably asking: what is a sole proprietorship and how do I stop it from complicating my personal finances? The legal and financial overlap can feel heavy, especially when you’re worried about what happens if a business debt suddenly becomes a personal one.

We believe the logistics of running a business shouldn’t get in the way of your passion. You’ve worked hard to build something on your own, and you deserve a clear path forward. This guide breaks down exactly how this structure works, from your specific tax obligations to the reality of personal liability. We’ll also help you recognize the signs that it’s time to transition to an LLC and show you how to find funding through resources like Kredline when you need to bridge a gap or invest in new equipment without a complex corporate history holding you back.

Key Takeaways

- Clear up the confusion around what is a sole proprietorship by understanding how this default structure merges your personal and business identity.

- Learn the real-world implications of unlimited personal liability and how it affects your personal assets during legal or debt challenges.

- Compare the simplicity of a solo setup against the “corporate veil” of an LLC to determine which legal path fits your current growth stage.

- Follow a straightforward checklist for registering your DBA and obtaining an EIN to ensure your business foundation is solid and compliant.

- Discover practical strategies for bridging seasonal cash flow gaps and how Kredline can help you explore funding options to keep your momentum.

Understanding the Sole Proprietorship: The Default Business Structure

Most entrepreneurs start their journey without even realizing they’ve already chosen a business structure. If you’ve started selling services as a consultant or products through an e-commerce shop without filing formal paperwork, you’re likely already operating one. By definition, what is a sole proprietorship is the simplest and most common form of business ownership in the United States. According to the U.S. Census Bureau, over 23 million businesses operate under this structure, accounting for the vast majority of small businesses nationwide.

The core concept is straightforward: there’s no legal distinction between the owner and the business. You aren’t just the owner; you are the business. This means you have total control over every decision, but you’re also personally responsible for every debt and legal obligation. It’s the default status for solo workers because it requires no formal action to “exist” in the eyes of the law. Common examples of people who thrive in this setup include:

- Freelancers: Writers, graphic designers, and developers who work project-to-project.

- Consultants: Experts who provide professional advice to other firms.

- Local Contractors: Handymen, landscapers, or cleaners who operate independently.

- E-commerce Sellers: Individuals running small shops on platforms like Etsy or eBay.

The “Single Member” Concept

Being a “single member” means you’re the sole decision-maker. You don’t have to consult a board of directors or a partner before making a move. You’re the recipient of all profits, which can be a huge motivator. However, the IRS treats your business income as personal income. You report your earnings and expenses on your personal tax return using a Schedule C. This differs significantly from partnerships or corporations where profits are shared and control is divided among multiple stakeholders. While the simplicity is great, remember that if the business owes money, you personally owe that money. This is why many owners eventually look into short-term business loans to manage cash flow without risking their personal savings during slow months.

Why Simplicity is the Greatest Advantage

The lack of formal state filing requirements is a major draw. You don’t have to pay the heavy incorporation fees that come with an LLC or a Corporation, which can range from $50 to over $500 depending on your state. Administrative costs stay low because you don’t need to maintain complex corporate bylaws or hold annual meetings. This structure offers the flexibility to pivot your business model instantly. If you’re a consultant who wants to start selling digital products, you don’t need to update any legal documents to make that change. You simply start. This “pincushion” agility allows you to respond to market shifts faster than larger, more rigid entities. When you’re ready to scale or need to purchase new equipment, you can explore funding options that fit your specific revenue patterns without the red tape of a corporate structure.

The Reality of Personal Liability and Tax Obligations

Choosing what is a sole proprietorship as your business structure means you and your company are legally one and the same. This simplicity is a double edged sword. While you have total control, you also carry unlimited personal liability. According to the legal definition of a sole proprietorship, the owner is personally responsible for every debt and legal obligation the business incurs. There’s no separation between your kitchen table and your office desk in the eyes of the law.

If your business faces a legal judgment or fails to pay a $25,000 vendor invoice, creditors don’t just look at your business bank account. They can legally pursue your personal savings, your vehicle, and in many states, your home. Unlike a corporation or an LLC, there’s no “corporate veil” to protect your private life from business failures. This makes risk management a daily necessity rather than a secondary concern for solo owners.

Navigating the Tax Landscape

Tax season is relatively straightforward because of pass-through taxation. You don’t file a separate business tax return. Instead, you report your net profit or loss on Schedule C of your personal Form 1040. This means your business income is taxed at your individual income tax rate, which can be a benefit if your business is just starting and has more expenses than revenue.

You’re also responsible for the full 15.3% self-employment tax, which covers both the employer and employee portions of Social Security and Medicare. While individual income tax brackets are expected to shift after 2025, the self-employment tax rate is projected to stay at 15.3% through 2026. Tracking every single business expense is the most effective way to lower this bill. Every $1,000 in valid deductions can save you roughly $153 in self-employment taxes alone.

Protecting Yourself Without an LLC

Since you lack a legal shield, insurance becomes your primary defense. General liability insurance protects you from physical accidents, while professional liability insurance covers errors in your work. These policies act as a financial buffer between a client’s lawsuit and your personal bank account. It’s the most important investment you can make to sleep better at night.

Contracts are another essential tool. Clear, written agreements with clients can limit your exposure by defining the scope of work and setting liability caps. Even though the law treats your money and the business money as one, you should still open a separate business bank account. This makes it much easier to track cash flow and prove your expenses during a tax audit. If you need to cover a gap in working capital without draining your personal savings, you might consider prequalifying for business funding to keep your personal accounts protected during lean months.

Sole Proprietorship vs. LLC: Choosing the Right Path

Deciding between staying a sole proprietor or forming a Limited Liability Company (LLC) is a major crossroad for every entrepreneur. A sole proprietorship is the default for about 73% of all American businesses because it costs almost nothing to start. You might only pay a small fee for a “Doing Business As” (DBA) name, which usually ranges from $10 to $100 depending on your local county office. In contrast, an LLC requires formal filing with the state, which can cost anywhere from $50 to $500, plus ongoing annual fees. For example, California LLCs must pay a minimum $800 annual franchise tax regardless of income.

The biggest difference lies in the “corporate veil.” This legal concept separates your personal assets from your business liabilities. Understanding what is a sole proprietorship means realizing that no such veil exists. If your business is sued or fails to pay a debt, your personal savings, car, and home are legally accessible to creditors. When you transition to an LLC, you create a protective barrier. This shift often marks a psychological change in how you view your work. You stop seeing yourself as a freelancer picking up gigs and start acting like a business owner building an entity with its own identity.

Attracting partners or investors is also much harder without a formal structure. Most professional investors won’t even look at a business that isn’t incorporated or organized as an LLC. If you need more than just your own effort to grow, choosing a business structure that allows for shared ownership is a necessary step for long-term scalability.

When Should You Transition?

Many owners look for specific milestones before making the switch. A common trigger is reaching $50,000 to $100,000 in annual net profit. At this level, the tax flexibility of an LLC, specifically the ability to be taxed as an S-Corp, can save you thousands in self-employment taxes. You should also consider the risk level of your industry. If you work in construction, food service, or any field where physical injury or property damage is a daily possibility, a sole proprietorship is often too dangerous. Hiring your first W-2 employee is another clear signal to change. Employees bring additional legal risks; an LLC ensures that an employment dispute doesn’t threaten your personal bank account.

Financing Differences Between Structures

Banks often view sole proprietors as higher-risk borrowers. Without a separate legal entity, the business’s survival is tied entirely to one person. If you get sick or can’t work, the revenue stops, which makes traditional lenders nervous. Because there is no legal separation, your personal credit score is the primary gatekeeper for any capital you seek. Most lenders will require a personal guarantee anyway, but having an established business structure helps build a separate business credit profile over time. If you need capital to bridge a gap while you’re still growing, you can explore short-term business loans tailored for solo owners who need quick, flexible solutions without the red tape of a big bank.

Step-by-Step: Setting Up Your Sole Proprietorship Correcty

Setting up your business doesn’t have to be a bureaucratic nightmare. While the simplicity of the structure is a major draw, skipping small steps now can cause tax or legal issues later. You’re building a foundation for growth, so it’s vital to handle the paperwork with precision. Understanding what is a sole proprietorship involves more than just starting to work; it requires a few specific registrations to stay compliant.

Naming Your Business

By default, your business name is your own legal name. If you want to operate as “Sunrise Consulting” instead of “John Doe,” you’ll need a Doing Business As (DBA) name. Before you commit to a brand, check the USPTO TESS database for trademark conflicts. This prevents expensive legal disputes after you’ve already invested in branding. Filing a DBA usually happens at your local county clerk’s office or through the Secretary of State. Fees vary by location, but you can typically expect to pay between $10 and $100 for the registration.

Operational Basics

Privacy is a major concern for many owners. Using your Social Security Number on every W-9 form exposes you to unnecessary identity risk. You can apply for an Employer Identification Number (EIN) for free on the IRS website. It acts like a social security number for your business and makes opening a bank account much easier. Even if you don’t have employees yet, an EIN keeps your personal data safer.

You also need to stay on top of the IRS schedule. If you expect to owe $1,000 or more in taxes for the year, you must pay estimated quarterly taxes. These payments are due in April, June, September, and January. Setting up a simple bookkeeping system early on helps you track these obligations. Many owners set aside 25% to 30% of their gross income in a separate account to ensure they aren’t caught off guard when tax season arrives.

- Apply for local permits: Check with your city or county. Even home-based businesses often need a home occupation permit.

- Industry-specific licenses: If you’re in construction, hair styling, or food service, you’ll need specific state-level certifications.

- Open a business bank account: Never mix your grocery money with your client payments. Clean records are essential if you ever need to prove your income for a loan.

Once your accounts are separated and your registrations are complete, you’ll have a much clearer picture of your cash flow. This organization is the first step toward scaling your operations. If you’re ready to take the next step in your business journey, you can prequalify for business funding to see what growth opportunities are available to you. Understanding what is a sole proprietorship is just the beginning; managing your capital effectively is what keeps the doors open.

Overcoming Funding and Cash Flow Challenges

Operating as a solo owner brings a unique set of financial hurdles. When you’re researching what is a sole proprietorship, the focus is often on taxes and simplicity, but the reality of daily cash flow is where the real work happens. You’re responsible for every expense, from the smallest software subscription to major equipment repairs. A study from U.S. Bank found that 82% of small businesses fail because of poor cash flow management. This risk is even higher for sole proprietors who don’t have a board of directors or a dedicated finance team to lean on.

Seasonal dips can hit hard. A retail shop might see a 40% surge in December followed by a stagnant January. Slow-paying clients are another common pain point. If you finish a project on the 1st but the client doesn’t pay until the 45th, you’re stuck covering your own costs for six weeks. Bridging this gap requires a proactive strategy rather than a reactive one. Capital should be a tool you use to stay ahead, not a last-minute rescue for a crisis.

Managing Working Capital

Working capital is the lifeblood of your operation. It’s the money that keeps the lights on while you wait for your hard work to turn into deposited funds. One of the most effective tools for this is a flexible credit limit. Understanding how a business line of credit supports solo growth can change how you view your monthly budget. It gives you the ability to pull funds for payroll or inventory only when you need them, keeping your interest costs lower than a standard term loan.

You can also improve your cash flow cycle by refining your internal processes. Try these practical steps:

- Send invoices immediately upon project completion instead of waiting until the end of the month.

- Request a 25% or 50% deposit upfront for projects that take longer than two weeks.

- Set up automated payment reminders to nudge clients five days before a bill is due.

Leveraging Your Revenue for Growth

Growth often requires spending money before you’ve actually earned it. If you’re a florist needing to stock up for Valentine’s Day or a contractor needing a new van, you need capital now. Many traditional lenders require five years of corporate history, which isn’t helpful for someone still learning what is a sole proprietorship in practice. If your business has consistent daily sales, Merchant Cash Advance options provide a path forward by looking at your credit card volume rather than just your years in business.

This type of financing is designed for speed. It allows you to access a lump sum that’s repaid as a percentage of your future sales. It’s a dynamic solution that scales with your business; if sales are slow one week, your repayment amount adjusts accordingly. To get a clear picture of what’s possible, you can prequalify for business funding to see your options early. Having this information helps you make strategic decisions about when to expand and when to hold steady.

Moving Your Business Forward with Confidence

Understanding what is a sole proprietorship helps you weigh the ease of a simple setup against the weight of personal liability. While this structure is the most common path for the 27.1 million nonemployer firms in the United States, it shouldn’t leave you stuck when you need capital. You’ve learned how to manage your taxes and when it’s time to consider an LLC. Now, the focus shifts to maintaining healthy cash flow to handle payroll or inventory.

See your funding options as a small business owner and get the support you need to keep growing. You’ve built this business on your own terms; let’s make sure you have the resources to keep it that way.

Frequently Asked Questions

Can a sole proprietor have employees?

Yes, you can hire as many employees as you need to run your business effectively. While you remain the sole owner and legal representative, you’re free to build a team to handle daily operations or specialized tasks. You’ll just need to apply for an Employer Identification Number from the IRS and follow state-specific labor laws. Many owners use Kredline to explore funding options when they’re ready to cover the costs of their first few hires.

Do I need a separate bank account for a sole proprietorship?

You aren’t legally required to have a separate account, but it’s a smart move for any serious business owner. Mixing personal and professional funds makes it difficult to track your true cash flow and complicates your tax filings at the end of the year. Most lenders, including those in the Kredline network, typically ask for 3 to 6 months of dedicated business bank statements to verify your revenue when you apply for a loan.

Is a sole proprietor the same as being self-employed?

The terms are related, but they describe different things. Self-employed is a general tax category for anyone who works for themselves, while a sole proprietorship is a specific legal structure. If you’re a freelancer or contractor and haven’t registered as an LLC, you’re likely operating as a sole proprietor by default. Understanding what is a sole proprietorship helps you recognize that you and your business are viewed as a single legal and financial entity.

How do I pay myself as a sole proprietor?

You pay yourself through “owner’s draws” rather than a traditional W-2 salary with tax withholdings. You simply transfer money from your business account to your personal account whenever you need it. Because the IRS treats all business profit as your personal income, you don’t pay extra taxes on these specific transfers. It’s helpful to set a consistent schedule for these draws to keep your personal budget stable throughout the month.

What is the biggest disadvantage of a sole proprietorship?

The most significant drawback is unlimited personal liability for all business debts and legal issues. Since there’s no legal wall between you and the company, your personal assets like your home or savings can be seized to pay off business creditors. Data suggests that roughly 80 percent of small businesses eventually transition to an LLC to gain better protection. This risk makes it vital to maintain clear financial records and adequate insurance coverage.

Can a sole proprietorship have a 401(k) or retirement plan?

You can absolutely set up a retirement plan, with the Solo 401(k) being a popular choice for one person operations. For the 2024 tax year, the total contribution limit for a Solo 401(k) is 69,000 dollars, which allows you to save significantly more than a standard IRA. You can also look into SEP IRAs if you want a simpler setup with flexible annual contributions. These plans help you build a safety net while reducing your taxable business income.

Do I need an EIN if I do not have employees?

You don’t need an Employer Identification Number if you’re working alone; you can use your Social Security number for most tasks. However, getting an EIN is free and helps protect your personal identity when sending invoices to clients or opening business accounts. It also gives your business a more professional appearance to vendors and partners. If you’re looking at prequalifying for funding through Kredline, having an EIN can often speed up the documentation process.

How do I change from a sole proprietorship to an LLC later?

You can transition by filing Articles of Organization with your Secretary of State and paying the required filing fee. Once the state approves your new status, you’ll need to create an operating agreement and apply for a new EIN to reflect the change. You’ll also need to update your bank accounts and any existing contracts to the new business name. This move is a common milestone for owners who have reached a consistent level of growth and want more security.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.