Last Tuesday, a local shop owner named Sarah realized her primary manufacturing unit was failing just as a large contract arrived. She had a tough choice. She could spend $15,000 upfront or turn away the business. You’ve likely been there too. It’s frustrating to stare at a price tag for essential tools and wonder if your bank account can handle the hit. We agree that you shouldn’t have to risk your daily operations, which is why business equipment loans are such a vital tool for growth.

This guide shows you how to secure new tech while keeping your cash flow steady. You’ll learn how to leverage financing for growth, understand the real differences between leasing and borrowing, and discover how to qualify without the stress of big bank rejection. We’ll also break down the tax deductions that could make your 2026 upgrades even more affordable. At Kredline, we believe finding the right funding should be a partnership, not a battle with a faceless institution. Let’s explore how to get your business the tools it needs to thrive.

Key Takeaways

- Learn how to scale your operations by financing essential assets without draining the working capital you need for day-to-day expenses.

- Compare the long-term benefits of ownership against the flexibility of leasing to decide which structure protects your balance sheet most effectively.

- Navigate the true cost of business equipment loans by understanding how equipment age impacts your APR and where to find potential tax advantages.

- Identify the specific “Three Cs” lenders look for in 2026 to ensure your application and equipment invoices are positioned for a quick approval.

- Discover how a marketplace approach creates competition among lenders, helping you secure more favorable terms than a traditional single-bank inquiry.

Understanding Business Equipment Loans: More Than Just a Purchase

Business equipment loans function differently than a standard line of credit or a mortgage. At its core, this is a self-collateralized agreement. The asset you’re buying, whether it’s a commercial oven, a CNC machine, or a fleet of delivery trucks, acts as the security for the debt. This structure is a game changer for small business owners who want to grow without risking their personal assets or putting up their home as collateral.

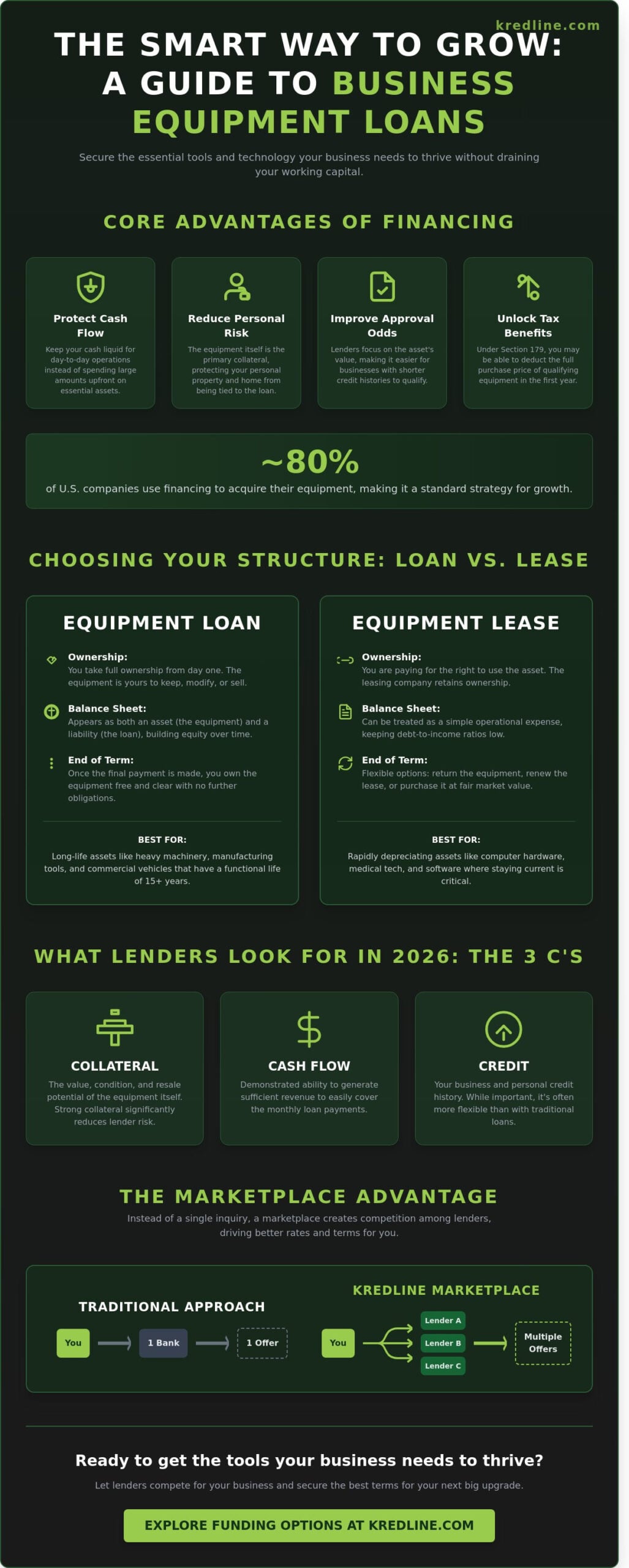

Lenders often find these easier to approve than general business loans because the risk is mitigated by the equipment’s resale value. If a borrower defaults, the lender can recoup costs by selling the asset. This reduces the need for the extensive personal guarantees that often accompany unsecured funding. It also helps maintain a healthier debt-to-income ratio. Since the loan is tied to a productive asset, it’s viewed as “good debt” that generates the very revenue needed to pay it back. According to the Equipment Leasing and Finance Association, nearly 80% of U.S. companies use some form of financing to acquire their equipment as of 2023. This approach offers several structural advantages:

- Reduced Personal Risk: The equipment itself is the primary security, protecting your personal property.

- Improved Approval Odds: Even businesses with shorter credit histories can qualify if the equipment holds strong market value.

- Tax Benefits: Depending on the structure, you may be able to deduct the full cost of the equipment in the first year under Section 179.

How Equipment Financing Protects Your Cash Flow

Many owners fall into the “cash trap” by spending large amounts of capital upfront. A $60,000 expenditure on new medical tech or kitchen hardware might seem like a sign of strength, but it leaves the business vulnerable to seasonal slowdowns or sudden repairs. By using equipment funding, you keep your cash liquid for operational emergencies. You can match your monthly payments to the revenue that the new equipment generates. If a new printing press brings in $4,000 of new business monthly, a $1,100 loan payment is easily absorbed without draining your reserves.

The Difference Between Equipment Loans and Traditional Business Loans

Traditional bank loans focus heavily on your company’s multi-year history and overall credit score. Equipment financing shifts that focus toward the asset’s value and its ability to produce income. This often leads to much faster funding times. While a standard SBA loan can take 60 to 90 days to process, an equipment loan can often be finalized in less than a week. The trade-off is the specific use-case. You can’t use these funds for payroll or marketing. The capital must go directly toward the hardware or software specified in the contract, ensuring the lender knows exactly where their money is working.

Choosing the Right Structure: Loans vs. Leases

Deciding how to finance your gear isn’t just about the monthly payment. It’s a strategic choice that affects your taxes, your debt-to-income ratio, and your ability to upgrade when technology shifts. When you look at business equipment loans, you’re essentially choosing between owning a long-term asset or paying for the utility of that asset over time. In 2026, where hardware cycles for AI-integrated tech are moving faster than ever, the “buy and hold” mentality doesn’t always win.

Industry standards often dictate the best path. If you’re in construction or manufacturing, heavy machinery like loaders or lathes can have a functional life of 15 years or more. In these cases, ownership usually makes the most sense. For those looking at major fixed assets, SBA 504 loans provide a reliable framework for long-term financing with competitive rates. However, if you’re running a medical lab or a data-heavy creative agency, the equipment you buy today might be obsolete in 36 months. That’s where the flexibility of a lease outweighs the equity of a loan.

Before you sign, you should explore different equipment funding options to see how each structure impacts your balance sheet. A loan appears as both an asset and a liability, while certain leases can be treated as a purely operational expense, keeping your credit lines open for other needs.

Equipment Finance Agreements (EFA) for Ownership

An EFA works much like a standard vehicle loan. You take ownership of the equipment at the start, and the lender holds a security interest until the final payment is made. This structure is ideal for building equity. Since you own the asset, you can often take advantage of Section 179 tax deductions, which allow you to deduct the full purchase price in the year you buy it. It’s the go-to choice for CNC machines, trailers, or any equipment with a long, productive life where you don’t mind the maintenance responsibilities.

Operating Leases and Fair Market Value (FMV) Options

If you prefer lower monthly payments and the ability to “walk away,” an FMV lease is a strong contender. You don’t pay for the full value of the equipment; you only pay for the portion you use during the term. At the end of the lease, you can return the equipment, buy it at its current market price, or upgrade to the latest model. This is the most efficient way to handle rapidly depreciating tech like servers or specialized medical scanners. It keeps your cash flow predictable and ensures you aren’t stuck with a warehouse full of outdated “paperweights” five years from now.

Finding the right balance between ownership and flexibility doesn’t have to be a headache. If you’re ready to see what’s possible for your next purchase, you can prequalify for funding in just a few minutes to get a clearer picture of your options.

Evaluating the True Cost: Rates, Terms, and Tax Benefits

Don’t get distracted by the sticker price of a new machine. The true cost of business equipment loans goes far beyond the monthly payment. You’ll likely encounter two ways lenders quote costs: Annual Percentage Rate (APR) and factor rates. APR is the gold standard because it includes both interest and fees over a full year. Factor rates, often expressed as a decimal like 1.2, multiply your total loan amount by that number. While factor rates seem simpler, they often result in higher costs because the interest doesn’t decrease as you pay down the principal. Before signing any contract, it’s helpful to review the FDIC guide to small business loans to see how these terms compare to traditional bank financing.

The age of the asset you’re buying heavily influences your rate. New equipment acts as excellent collateral, so lenders offer lower rates and longer terms. Used machinery is different. If you’re buying a five-year-old delivery truck, a lender might limit the term to 36 months instead of 60. They do this because the resale value drops faster, increasing their risk. You should also look for “all-in” costs. Many lenders charge an origination fee between 1% and 4% of the total loan. Others add documentation fees for processing titles or UCC-1 filings. These small charges can add thousands to your total repayment amount. While you’re looking at your budget, comparing short-term business loans can help you decide if equipment financing or a quick cash injection is better for your current needs.

Maximizing the Section 179 Deduction in 2026

The IRS Section 179 deduction remains a massive advantage for small businesses. It allows you to deduct the entire purchase price of qualifying equipment in the first year instead of depreciating it over a decade. For 2026, the deduction limit is projected to exceed $1.29 million, with a phase-out threshold starting around $3.22 million. This means if you finance a $100,000 CNC machine, you could potentially deduct the full $100,000 from your taxable income immediately. In many cases, the tax savings in year one are actually higher than the total loan payments you made during those first 12 months.

Negotiating Terms for Seasonal Businesses

If your revenue fluctuates, don’t settle for a rigid payment schedule. Many providers of business equipment loans offer flexible structures. You can request “step-up” payments, where you pay less during the first few months while the equipment starts generating profit. Alternatively, “step-down” plans let you pay more upfront to reduce interest costs later. For industries like construction or landscaping, ask about seasonal skip-payments. This allows you to pause or reduce payments during your slowest months, ensuring your cash flow stays healthy when the weather stops your work. Always try to align the loan term with the useful life of the asset so you aren’t paying for a machine that’s already in the scrap yard.

Preparing Your Application: What Lenders Look for in 2026

Applying for business equipment loans in 2026 requires a shift in how you view your company’s financials. Lenders have moved beyond simple credit checks, focusing instead on the “Three Cs”: Credit, Capacity, and Collateral. Your personal credit still matters, but it’s no longer the only gatekeeper. Capacity refers to your actual cash flow; lenders want to see that your business generates enough monthly revenue to cover the new payment without strain. Collateral is the equipment itself, which serves as the primary security for the debt.

The equipment invoice is often the most critical document in your file. It’s not just a price tag. It tells the lender exactly what they’re financing, its expected lifespan, and its resale value. If you’re buying a $75,000 piece of medical imaging hardware, the lender evaluates its “liquidation value” from day one. You should also present a clear case for ROI. If this purchase allows you to fulfill 20% more orders per month or replaces a rental that costs $2,000 more monthly, put those numbers in writing. Lenders value seeing that the equipment pays for itself through increased efficiency.

Credit Score Requirements and Alternative Data

By 2026, the industry has shifted toward cash-flow underwriting. A FICO score of 640 might have been a deal-breaker in the past, but consistent daily or weekly revenue can now offset a lower rating. If your bank statements show steady deposits over the last 180 days, you’re in a much stronger position. Time in business is also becoming less of a hurdle. If the asset has a high resale value, some lenders will work with businesses that have been active for only 12 months rather than the traditional two-year minimum.

The Essential Document Checklist

Organization is the fastest way to build trust with a lender. You’ll need to provide the last 4 to 6 months of business bank statements to prove your liquidity. If the new equipment is meant to expand your capacity, include pro-forma statements that project your new revenue levels based on that growth. Finally, ensure your business is in good standing with the Secretary of State. A lapsed filing or an undisclosed tax lien is an automatic rejection trigger that no amount of revenue can fix.

Common mistakes like mismatched business names on your application and your bank accounts can delay your funding by weeks. Double-check every line before hitting submit. If you’re ready to see which terms your business qualifies for, you can explore your equipment funding options to get a clear picture of your borrowing power without the stress of a traditional bank’s red tape.

Finding Your Best Fit: Navigating the Equipment Marketplace

Most owners start their search for business equipment loans at the bank where they keep their checking account. It’s a convenient choice, but it’s rarely the most cost-effective path. Banks have narrow “appetites” for risk and specific asset classes. If you’re in a high-growth phase or a specialized industry like construction or logistics, a traditional bank might see your request as too risky. This often leads to higher interest rates or flat-out denials that can stall your progress for months. A marketplace approach changes this dynamic by forcing lenders to compete for your business, which naturally drives down costs and opens up more flexible structures.

A broker or marketplace navigator acts as your advocate in this process. They translate “bank-speak” into plain English so you can understand the real impact on your bottom line. Instead of being at the mercy of one loan officer’s decision, you gain leverage. You’ll know exactly why one offer has a lower monthly payment but a higher total cost of capital, allowing you to make a choice based on data rather than desperation.

Why a Marketplace Approach Beats a Single Bank

When you use a marketplace, you gain access to specialized lenders who actually understand your specific field. A lender who focuses on medical imaging understands the long-term value of a 2026 CT scanner better than a general branch manager does. This industry expertise usually translates to lower down payments and better leverage. You’ll see multiple offers side-by-side, allowing you to compare the fine print, such as early buyout options or seasonal payment structures that match your revenue cycles. Instead of spending 15 to 20 hours filling out individual applications, you complete one set of documents that reaches dozens of vetted providers. This efficiency is vital when a piece of gear you need is available now but might be gone by the time a slow-moving bank approves your file.

How Kredline Simplifies the Search for Capital

We don’t just provide a list of names; we act as a partner in your growth. Our process is designed to take the weight off your shoulders by handling the heavy lifting of lender communication. We focus on your cash flow health first. We’ll help you determine if a new piece of tech or machinery will truly pay for itself within your current budget before you sign any contracts. Our goal is to ensure the funding solves a problem rather than creating a new one. You can prequalify for funding without a hard credit pull to get a clear picture of your options. This step protects your credit score while giving you the data needed to make a confident decision for your company’s future.

Putting Your 2026 Growth Plan Into Motion

Success this year depends on having the right tools at the right time. Whether you’re looking at Section 179 tax benefits to offset costs or weighing the long-term equity of a purchase against the flexibility of a lease, your choice impacts your cash flow for years. Lenders in 2026 prioritize clear financial records and a solid understanding of how new machinery drives revenue. Securing business equipment loans shouldn’t feel like a second job. It’s about finding a structure that supports your daily operations without draining your working capital.

We act as your financial navigator, providing expert guidance to help you make sense of the current marketplace. Our team connects you to a national network of 3rd-party providers, ensuring you see a wide range of possibilities tailored to your specific industry. You can explore these paths without any pressure or commitment.

See your equipment financing options with Kredline through our simple, no-obligation prequalification process. We’re excited to help you build a stronger, more efficient future for your business.

Frequently Asked Questions

What credit score is needed for a business equipment loan?

Most lenders look for a credit score of 620 or higher to qualify for competitive rates on business equipment loans. While some specialized providers accept scores as low as 550, they often require additional collateral or a larger down payment to offset the risk. At Kredline, we look at your full financial picture, focusing on cash flow and business health rather than just a single credit number.

Can I get equipment financing if my business is new?

You can secure equipment financing for a new business, though most lenders prefer at least six months of operational history. Startups often need to provide a 20% down payment or a personal guarantee to move the process forward. If your company is less than two years old, having a solid business plan and proof of consistent monthly revenue will help you secure better terms.

Is a down payment required for equipment loans?

A down payment of 10% to 20% is standard for many equipment purchases, but 100% financing is available for established companies with strong credit. Paying a portion upfront is often a smart move because it reduces your monthly installments and total interest costs. If you want to keep your cash in the business, we can help you explore options that require zero money down at closing.

What is the difference between a lease and an equipment loan?

The main difference is ownership; a loan means you own the asset from day one, while a lease functions like a long term rental. With a loan, the equipment sits on your balance sheet as an asset and you can claim depreciation. Leases typically offer lower monthly payments and make it easier to swap out gear for newer models every three to five years.

Can I finance used equipment or must it be new?

You can finance both new and used equipment, provided the used machinery has a documented appraisal and enough remaining life to last the duration of the loan. Lenders usually require used items to be less than 10 years old so they maintain enough value as collateral. Buying used is a practical way to save 30% or more on costs while still getting high quality tools.

How long does the approval process take for equipment funding?

Approval for equipment funding typically takes between 24 hours and three business days when working with online lenders. Traditional banks often take two weeks or more to review financial statements and process the paperwork. Kredline simplifies this by focusing on efficiency, so you can get the tools you need without the stress of long waiting periods or endless office visits.

Are there tax benefits to financing equipment rather than paying cash?

Financing equipment offers major tax advantages through Section 179 of the IRS code, which lets you deduct the full purchase price in the year you acquire the asset. In 2024, the deduction limit was set at $1.22 million for qualifying equipment. This allows you to lower your taxable income immediately, even if you are still making monthly payments on the equipment over several years.

Can I finance software or just physical machinery?

You can finance software, cloud subscriptions, and even installation costs through modern business equipment loans. Many lenders now include “soft costs” like training and implementation in the total loan amount. Since digital infrastructure is vital for growth, these loans aren’t restricted to heavy machinery; they’re designed to cover whatever technology keeps your specific business running smoothly and efficiently.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.