Last Tuesday, a local landscaping owner discovered her main truck needed a $4,200 engine overhaul just as the spring rush began. Even with $35,000 in outstanding invoices, she didn’t have the liquid cash to get back on the road by Wednesday morning. You’ve likely felt that same knot in your stomach when a 60 day payment cycle clashes with an immediate business need. It’s frustrating to watch growth stall because your capital is locked in someone else’s accounts receivable, which is why a business loc has become the preferred tool for modern cash flow management in 2026.

We’ve designed this guide to help you stop reacting to cash flow gaps and start outrunning them. You’ll learn how a strategic line of credit provides a flexible safety net that adjusts to your revenue, rather than forcing you into a rigid monthly payment. We’ll explore the current lending landscape, including how Kredline helps owners qualify with a simple three page application instead of a bulky business plan. By the end, you’ll know exactly how to use revolving credit to seize inventory discounts and handle repairs without the stress of a traditional term loan.

Key Takeaways

- Understand how a revolving credit limit provides more flexibility than a standard loan, allowing you to draw and reuse funds only when your business needs them.

- Learn how to strategically use a business loc to bridge seasonal gaps and ensure your team is paid during slower revenue months.

- Discover the specific financial documents and credit benchmarks you need to prepare to streamline your application and secure a faster approval.

- Find out how responsible borrowing helps build your company’s credit profile, making it easier to qualify for larger expansion funding in the future.

- See why looking beyond a single bank increases your options and how to navigate a network of providers to find the right fit for your specific needs.

What is a Business Line of Credit (LOC) and How Does It Work?

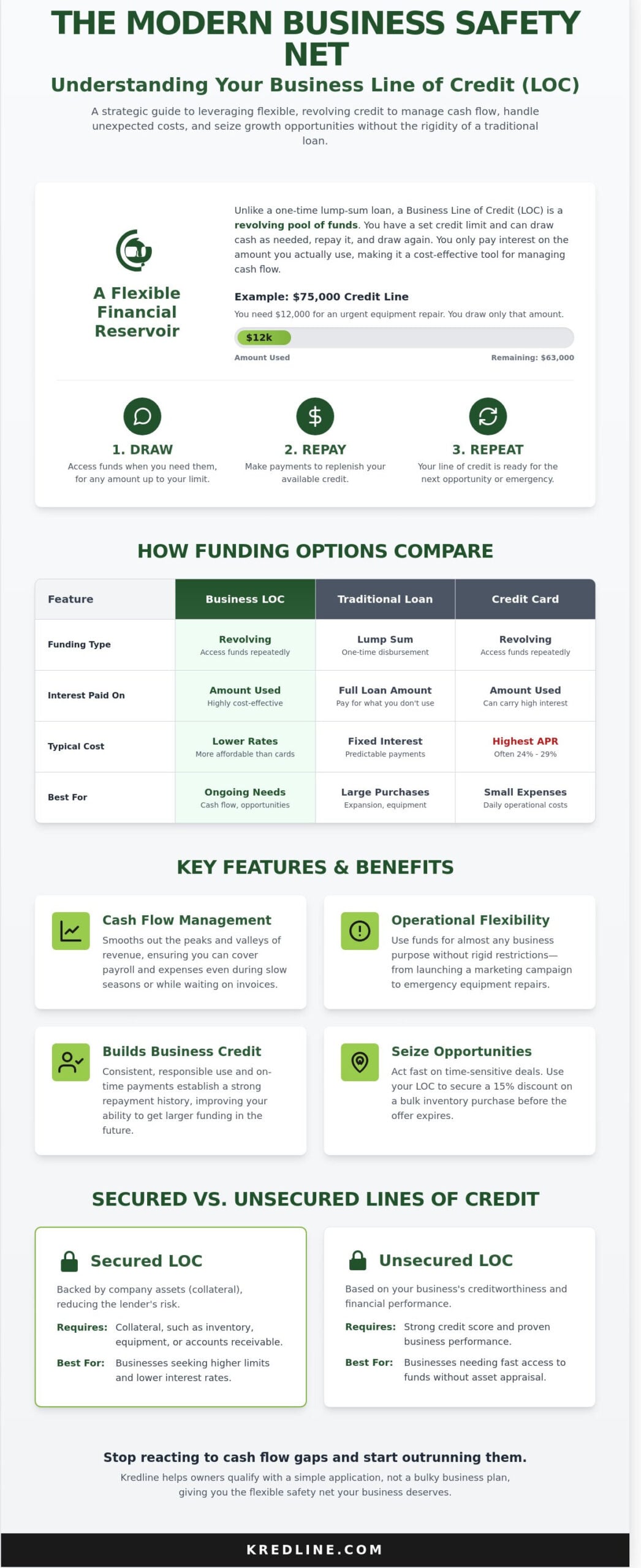

Think of a business line of credit as a flexible financial reservoir. Unlike a traditional loan where you receive a lump sum and pay interest on the whole amount from day one, a line of credit gives you access to a pool of funds that you can tap into whenever a need arises. You might wonder, What is a Business Line of Credit (LOC) exactly? In simple terms, it’s a revolving credit limit that allows you to draw funds, repay them, and draw them again as long as the account remains open. It’s designed to provide liquidity exactly when your cash flow hits a temporary dip.

The easiest way to understand a business loc is by comparing it to a high-limit credit card. You have a maximum credit limit, for example, $75,000. If you only need $12,000 to cover a temporary payroll gap or to buy discounted inventory for a sudden seasonal rush, you only draw that $12,000. You don’t pay interest on the remaining $63,000. This makes it a highly cost-effective safety net for unpredictable expenses. You’re in control of the timing and the amount, which is a level of freedom most fixed-term loans simply don’t offer.

The revolving nature is the biggest strength of this tool. As you make payments toward the principal you’ve borrowed, those funds become available for use again. It’s a continuous cycle of capital. If a business pays off its balance in full, the entire credit limit is ready for the next opportunity or emergency without the need to go through the application process all over again. In 2026, where market shifts happen in days rather than months, having this business loc ready to go is a strategic advantage for any small business owner.

Revolving vs. Non-Revolving Credit

A standard term loan is non-revolving; once you spend the money and pay it back, the contract ends. A revolving line of credit can stay open for years, providing a permanent safety net. This persistent access is why it’s the preferred tool for managing working capital. It allows you to act quickly. If a supplier offers a 15% discount for an early bulk purchase, you can use your line of credit to secure that deal immediately rather than waiting weeks for a new loan approval. It’s about having capital ready before you actually need it.

Secured vs. Unsecured Lines of Credit

Secured lines of credit require collateral, such as inventory, equipment, or accounts receivable. Because the lender has an asset to fall back on, these often come with higher limits and lower interest rates. Unsecured lines of credit don’t require physical assets; instead, lenders look at your credit score and business performance. For small businesses needing immediate liquidity, unsecured options are typically faster to set up. You won’t spend weeks getting assets appraised, which is vital when you need to bridge a gap between invoices and expenses right now.

Key Features and Benefits of a Business Credit Line

A business credit line functions differently than a standard loan because it prioritizes your company’s agility. Instead of receiving a one-time lump sum, a business loc gives you access to a predetermined pool of capital that you can draw from whenever a need arises. You only pay interest on the amount you actually use, which makes it one of the most cost-effective tools in a founder’s toolkit. Recent data from 2024 shows that approximately 43% of small businesses rely on these lines to manage day-to-day operations and unexpected hurdles.

- Cash flow management: It smooths out the inevitable peaks and valleys of monthly revenue, ensuring you aren’t caught off guard during a slow season.

- Building business credit: Consistent, responsible use helps establish a strong repayment history. This improves your future borrowability and can lead to higher limits or lower rates later on.

- Operational flexibility: There aren’t rigid restrictions on how you use the funds. Whether you’re launching a targeted marketing campaign or repairing a delivery vehicle, the choice is yours.

- Lower costs: Interest rates for a credit line are typically much lower than the 24% to 29% APR often found on high-limit business credit cards.

Bridging the Gap Between Invoices

Waiting for clients to pay can be the most stressful part of running a business. If you operate on Net-30 or Net-60 terms, you might have $50,000 in accounts receivable but struggle to cover a $10,000 payroll on Friday. An LOC removes that “waiting game” anxiety. It allows you to keep your operations moving while your customers take their time to pay. Many savvy owners also use their line to pay vendors early; if a supplier offers a “2/10 Net 30” discount, using your LOC to pay within 10 days can save you 2% on your total invoice. Over a year, those small percentages significantly pad your profit margins.

Emergency Preparedness and Growth

Business doesn’t always go according to plan. A server crash or a sudden roof leak can require an immediate $5,000 investment you didn’t budget for. Having a credit line already in place means you don’t have to scramble for high-interest emergency funding. This aligns with Small Business Administration guidance which emphasizes using credit lines strategically for short-term operational needs.

This strategic use of funds also extends to proactive investments in technology. For companies managing complex sales partnerships or distribution channels, using a line of credit to implement automated management tools can be a smart move. As an example, the solutions provided by Computer Market Research are designed to help enterprises streamline these very processes, turning operational capital into a direct driver of growth.

Beyond emergencies, an LOC helps you seize “flash” opportunities. If a supplier announces a 20% clearance sale on inventory you know you’ll need in three months, you can buy in bulk immediately. While a short-term business loan is excellent for a specific, one-time purchase, the revolving nature of an LOC is better suited for these unpredictable moments. If you’re ready to see what’s available for your company, you can explore your business loc options to find a fit that matches your specific revenue cycle.

Strategic Use Cases: When to Draw from Your Line

A business loc works best when it’s used as a surgical tool rather than a permanent crutch. It provides the liquidity you need to handle short-term hurdles without giving up equity or taking on the rigid structure of a term loan. Most successful owners use their credit line to manage the 15 to 30 day gaps that naturally occur in a growing company’s cash flow. It’s about having the confidence to say yes to an opportunity because you know the capital is already sitting there, ready to be deployed.

Late payments are a common headache for small firms. Statistics show that roughly 39% of invoices in the B2B sector are paid past their due date. When a major client check is delayed by three weeks, your payroll obligations don’t move. Drawing from your business loc ensures your team stays paid and focused while you wait for those receivables to clear. This keeps morale high and prevents the stress of “robbing Peter to pay Paul” every Friday. You can also use this flexibility to test new growth levers. If you want to spend $4,500 on a targeted social media campaign to see if it moves the needle, a credit line allows you to fund that experiment without draining your operational reserves.

Before you tap into your funds, it is a smart move to compare business lines of credit to see how different lenders handle draw fees and repayment structures. Every dollar you save on interest is a dollar that stays in your bottom line.

The Seasonal Business Strategy

For a landscaping company in the Northeast, revenue might drop by 75% between December and March. A line of credit acts as a bridge to cover fixed costs like warehouse rent and key staff salaries during these quiet months. The goal is to borrow only what is necessary to maintain stability. A good rule of thumb is to avoid drawing more than 25% of your expected peak-season monthly revenue. This ensures that when the spring rush hits in April, you can pay down the balance quickly without suffocating your new cash flow.

Capitalizing on Bulk Discounts

Timing is everything in procurement. If a supplier offers a 12% discount for an upfront cash purchase of $40,000 in inventory, but your credit line interest for a 90-day draw is only 3%, the math is clear. You’ve effectively increased your profit margin by 9% just by being liquid. Having an active line allows you to move fast when these deals appear. In cases where you need a specific piece of machinery to fulfill a new contract, you might also look into equipment funding to keep your credit line open for other operational needs. This multi-tool approach to financing keeps your business agile and ready for 2026’s market shifts.

How to Qualify and Prepare Your Application

Securing a business loc in 2026 requires a shift in mindset. You aren’t just filling out a form; you’re presenting a data-backed case for your company’s reliability. Lenders have moved away from manual reviews, favoring automated systems that analyze your real-time financial health. To get the best rates, you need to have your digital and physical paperwork ready before you click apply.

Preparation starts with these five pillars:

- Review your FICO score: Traditional banks still hunt for a 680 or higher. However, 72% of alternative lenders now accept scores as low as 600 if your cash flow is strong.

- Organize your financials: You’ll need Profit and Loss (P&L) statements and balance sheets from the last two fiscal years. Keep your 1099s or K-1s handy if you’re a sole prop or partnership.

- Verify time in business: Most providers require at least 6 months of active operations. If you’ve hit the 2-year mark, you’ll likely see a 1.5% to 3% drop in offered interest rates.

- Calculate average monthly revenue: Lenders typically cap your credit limit at 10% to 20% of your annual gross sales. If you’re doing $50,000 a month, expect a limit around $60,000 to $100,000.

- Submit for prequalification: Always look for “soft pull” options first. This allows you to see estimated terms without dinging your credit score by the 5 to 10 points usually associated with a hard inquiry.

What Lenders Really Look For

In the current market, cash flow consistency is more important than a perfect credit score. Lenders look for “stable deposits,” meaning they want to see that money enters your account at regular intervals rather than in one giant lump sum once a quarter. This is why linking your bank account via secure portals like Plaid has become the industry standard. It gives the lender a 90-day window into your daily balances. If you operate in a high-risk industry like construction or transportation, expect shorter repayment draws, whereas professional services often get longer windows.

Common Objections and How to Overcome Them

The “personal guarantee” is the biggest hurdle for most owners. It’s a standard requirement for unsecured lines, meaning you’re personally responsible if the business fails to pay. If this feels too risky, ensure your debt-to-income ratio is below 35% to negotiate better terms. If your credit score is the main issue, you might not qualify for a traditional line immediately. In these cases, exploring revenue-based financing can help you bridge the gap and build the credit history needed for a future business loc. Always demand transparency regarding factor rates versus APR so you know exactly what the capital costs you over 12 months.

Ready to see what your business qualifies for without a hard credit pull? Apply for prequalification through Kredline today and get a clear view of your funding options in minutes.

The Marketplace Advantage: Why Navigating Options Matters

Approaching a single bank for a business loc often feels like putting all your eggs in one basket. If that one lender says no, your funding journey stops right there. This single bank approach is a primary reason why many entrepreneurs feel stuck when they need capital. In early 2026, the lending market is more fragmented than ever, which means the best rates often hide outside of the traditional branch on the corner. According to data from the 2024 Small Business Credit Survey, nearly 40% of small businesses were denied the full amount of credit they requested from large banks; a trend that has only intensified as credit standards tightened.

Kredline acts as your navigator in this complex environment. Instead of knocking on twenty doors yourself, you gain access to a network of third-party providers through a single point of contact. This isn’t just about getting a “yes,” it’s about finding the lowest cost of capital. When you see multiple offers side-by-side, you can compare the small details, like draw fees or repayment schedules, that have a massive impact on your monthly cash flow. Finding the right business loc means looking at the fine print without the pressure of a ticking clock.

Why a Broker Beats a Direct Lender for Small Business

Direct lenders only offer their own products. If you don’t fit their specific box, they can’t help you. A broker provides access to alternative funding options that traditional banks rarely mention. This saves you an incredible amount of time. Industry reports show that the average small business owner spends over 25 hours on paperwork for a single loan application. We’ve streamlined this so you can submit one application and see where you stand with multiple matches. It’s the most efficient way to prequalify for business funding without the typical stress of the unknown.

Finding the Right Fit for Your Business Stage

Every business has different priorities. You might need a credit line to manage weekly payroll during a seasonal dip, or perhaps you’re eyeing a bulk inventory purchase to fuel a 15% growth target. We help match your specific needs to the right product. For example, if your revenue comes primarily through credit card transactions, a Merchant Cash Advance might be a better fit than a standard credit line because the repayments fluctuate with your sales volume.

Securing your credit line is the final step toward gaining peace of mind. Once that safety net is in place, you can stop worrying about “what ifs” and start focusing on your next big move. Whether you’re bridging a 30-day gap or preparing for a major expansion, having the right financial partner makes all the difference in how quickly you can react to opportunities.

Securing Your Growth for 2026 and Beyond

Running a company means you’re always looking ahead. By 2026, having a flexible business loc won’t just be an advantage; it’ll be a necessity for managing the gaps between your 30-day invoice cycles and immediate payroll needs. You’ve seen how a line of credit provides the liquidity to grab inventory discounts or cover unexpected repairs without draining your cash reserves. The right preparation now, like organizing your last 6 months of bank statements, ensures you’re ready when opportunity knocks.

You don’t have to navigate these financial markets alone. We focus strictly on commercial growth, meaning we don’t handle personal loans. Instead, we connect you with a network of over 75 third-party funding providers to find a fit that actually makes sense for your specific industry. Our team provides transparent, human-first guidance to help you understand every term before you sign. Your business deserves a partner that values your time as much as you do.

See your funding options and prequalify with Kredline today.

Let’s get your capital working for you.

Frequently Asked Questions

How does a business line of credit differ from a traditional business loan?

A business line of credit provides flexible access to funds up to a set limit, while a traditional loan delivers a one-time lump sum. You only pay interest on the amount you actually draw from your business loc, which helps manage 30-day invoice gaps. Unlike a $50,000 fixed-term loan where you pay interest on the full balance, an LOC lets you take $5,000 today and pay it back to reset your limit.

What is the average interest rate for a business line of credit in 2026?

Interest rates for a business loc in 2026 typically range between 7.5% and 18.5% depending on your credit profile. Prime borrowers often see rates around 8.25%, while alternative lenders might charge 1.5% to 2% monthly for shorter-term draws. These rates are often variable, tied to the 2026 Wall Street Prime Rate, which currently sits at 7.0% for most commercial lending products.

Can I get a business line of credit with a low credit score?

You can secure a credit line with a personal score as low as 580, though terms will be more restrictive. Lenders often look for at least $15,000 in monthly revenue or 12 months of business history to offset lower scores. While a 720 score gets you the best rates, many fintech platforms focus on your real-time cash flow and 3-month bank average rather than just a single number from a credit bureau.

What documents do I need to apply for a business LOC?

Most lenders require your last 4 months of business bank statements and your most recent federal tax return. You’ll also need to provide your business EIN and a valid government ID for any owner with more than 25% equity. Digital lenders often use secure connections to your accounting software, like QuickBooks or Xero, to verify your $250,000 annual revenue or current accounts receivable quickly without manual paperwork.

How long does it take to get approved for a business credit line?

Approval times vary from 24 hours with online lenders to 3 weeks at traditional commercial banks. Fintech platforms often provide an initial offer within 60 minutes after you link your bank accounts. Once you sign the final agreement, funds are usually available in your account by the next business day. This speed allows you to meet a Friday payroll or catch a limited-time inventory discount without the wait.

Are there any annual or monthly fees for keeping a credit line open?

Many lenders charge an annual maintenance fee ranging from $95 to $500 to keep the facility active. You might also encounter a draw fee of 1% to 2% each time you transfer funds to your checking account. It’s important to check if there’s an inactivity fee, which some banks apply if you don’t use the line at least once every 6 months to cover their administrative costs.

Do I have to provide collateral for a business line of credit?

Unsecured lines of credit under $100,000 often don’t require specific physical collateral like real estate or equipment. Instead, lenders usually require a personal guarantee or a general lien on business assets. For larger limits exceeding $250,000, you might need to pledge specific accounts receivable or inventory. This security helps you land a lower interest rate and more favorable repayment terms for your growing company.

What happens if I cannot pay back a draw on my credit line?

Missing a payment typically triggers a late fee of $35 or 5% of the overdue amount. If the account remains unpaid for 90 days, the lender may freeze the entire line and initiate collection actions based on your personal guarantee. This can lower your credit score by 100 points or more. It’s better to contact your advisor at Kredline to discuss restructuring options before a deadline passes.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.