What if the lowest interest rate on paper actually costs your business more in the long run? It’s a common dilemma for owners looking at 2026 sba loan rates, especially when a 120 day application timeline might mean losing a key contract or a 20% discount on bulk inventory. You likely view these loans as the gold standard for growth, but the complexity of base rates and spreads often obscures the true monthly impact on your cash flow.

We’ll help you decode the math so you can stop guessing about your future overhead. You’ll learn how to calculate your exact payment impact and whether the strict collateral requirements of an SBA loan make sense for your current assets. Whether you’re bridging a 45 day gap between invoices or planning a major equipment purchase, this guide provides the framework you need to decide between government backed funding and faster alternatives. If the math feels heavy, Kredline is here to help you prequalify and compare your options without the typical bank headache.

Key Takeaways

- Understand how the federal guarantee keeps these loans accessible and why they often offer better terms than traditional bank financing.

- Demystify how sba loan rates are calculated using a base rate plus a negotiated spread so you can talk to lenders with confidence.

- Compare the 7(a) and 504 programs to determine which funding structure aligns best with your specific expansion or equipment needs.

- Identify the “hidden” expenses, such as guaranty fees and closing costs, that define the true total cost of your borrowing.

- Recognize when the “SBA Gap” makes a faster, more flexible alternative a better choice for your immediate cash flow requirements.

Understanding SBA Loan Rates in 2026: The Basics

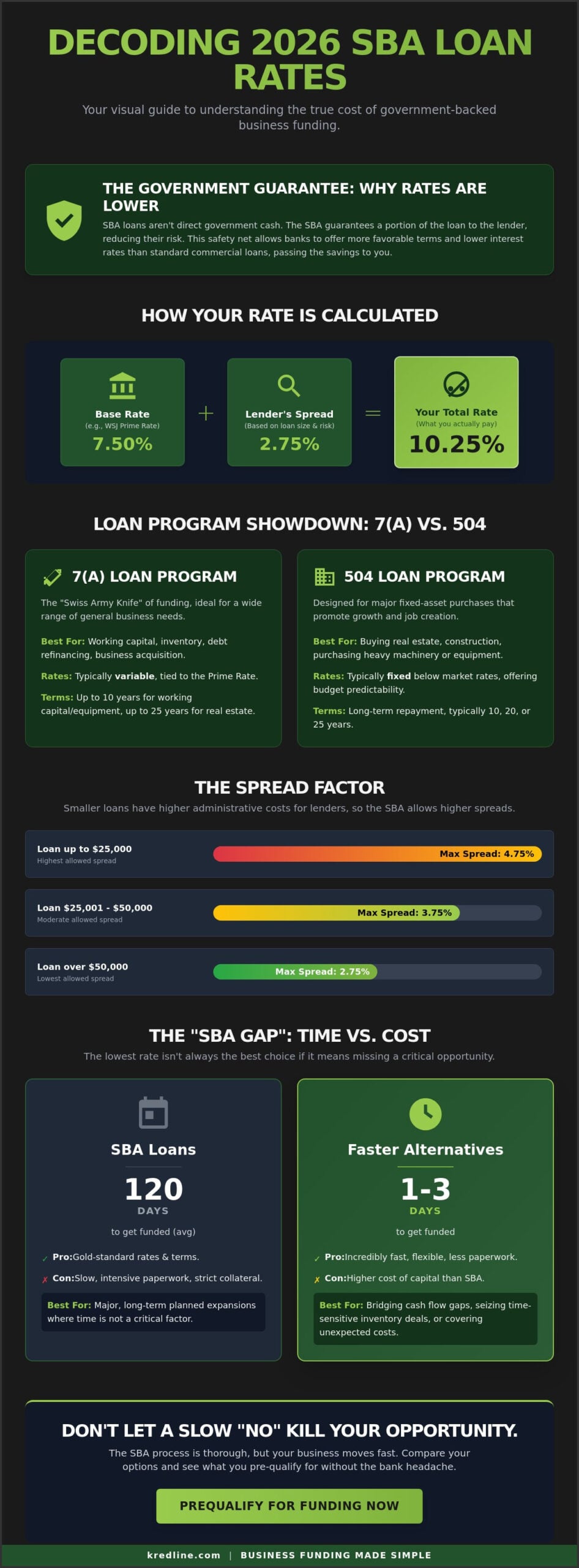

SBA loans are often misunderstood as direct government handouts. They aren’t. Instead, the U.S. Small Business Administration (SBA) provides a guarantee to private lenders, promising to pay back a portion of the loan if the borrower defaults. This safety net allows banks to offer much lower sba loan rates than you’d find with standard commercial products. Because the lender’s risk is minimized, they pass those savings on to you in the form of more affordable capital.

You’ll mostly encounter two primary paths: the 7(a) program and the 504 program. The 7(a) is the “Swiss Army Knife” of business funding, used for everything from working capital to debt refinancing. Its rates are typically variable, fluctuating with the market. The 504 program is different. It’s designed for major fixed assets like real estate or heavy machinery, often featuring long-term, fixed rates that provide more predictability for your monthly budget. Each has a different purpose, but both aim to put growth within reach for those who might not qualify for traditional conventional financing.

Why SBA Rates Are Considered the Gold Standard

The real draw of these loans isn’t just the interest percentage; it’s the repayment structure. SBA loans offer terms that traditional banks rarely match on their own. You can get up to 25 years for real estate and 10 years for equipment or working capital. These longer windows significantly drop your monthly debt service, freeing up vital cash flow for payroll or inventory. It’s the difference between struggling to breathe each month and having the room to actually run your business.

The SBA also enforces a strict “cap” system. Lenders can’t just charge whatever they want. They’re limited to a maximum markup, or spread, over the base rate. This protection ensures that even in a volatile market, you aren’t being price-gouged. These sba loan rates typically benefit established businesses with a solid track record and collateral, though they remain the most cost-effective way to scale if you can meet the requirements. If the strict SBA criteria don’t align with your current timeline, you might want to look at other funding options that offer more speed and flexibility.

The 2026 Economic Context

Heading into 2026, the lending landscape has shifted. After the inflationary spikes of the mid-2020s, the Federal Reserve’s policy has moved toward a period of stabilization. The Prime Rate remains the primary driver for most small business debt. Most 7(a) loans are pegged directly to this number. The “Base Rate” serves as the foundation of your total interest cost, representing the starting point before the lender adds their specific margin based on your creditworthiness.

In 2026, federal shifts have focused on increasing loan availability for smaller loan amounts under $150,000, though the competition for larger funds remains high. While the market is more predictable than it was two years ago, the “cost of money” is still a major factor in your bottom line. Before you commit to a long-term application, it’s often helpful to prequalify for business funding to see where you stand in the current environment. Understanding these benchmarks helps you negotiate with lenders from a position of strength and clarity.

How Your SBA Interest Rate is Actually Calculated

Understanding sba loan rates doesn’t require a finance degree. It’s a simple addition problem. You take a base rate and add a lender’s markup, known as a spread. Most lenders use the Wall Street Journal Prime Rate as that base. In early 2026, if the Prime Rate sits at 7.50% and your lender adds a 2.75% spread, your total interest rate is 10.25%. This formula keeps things transparent, but the “spread” part is where the variables hide.

The SBA doesn’t just let lenders charge whatever they want. They set a ceiling called the Maximum Allowable Spread. This protection ensures small business owners aren’t gouged, but it also means your rate depends heavily on your loan size. Larger loans generally enjoy lower spreads. If you’re borrowing $500,000 to buy a warehouse, your spread will be significantly lower than a peer borrowing $20,000 for inventory. Smaller loans carry higher percentage rates because the administrative costs for the bank are roughly the same regardless of the check’s size.

The Role of the Prime Rate and Spreads

Lenders look at the WSJ Prime Rate as their primary index. For 7(a) loans over $50,000 with a maturity of seven years or longer, the SBA typically caps the spread at 2.75% over Prime. If you’re seeking a smaller loan, like those under $25,000, the SBA allows a spread of up to 4.75%. This is why a “small” loan can sometimes feel surprisingly expensive. To see how these percentages translate into monthly costs, it helps to estimate your SBA loan payments using a tool that accounts for both the interest and the mandatory SBA guarantee fees.

Don’t assume the maximum spread is a fixed price. While the SBA sets the limit, you can still negotiate with your lender. A business with five years of clean tax returns and strong collateral has more leverage to ask for a lower spread than a startup. It’s always worth asking if the lender can shave off 0.25% based on your credit history.

Fixed vs. Variable: Choosing for Your Cash Flow

Most SBA 7(a) loans come with variable rates. These usually adjust on a quarterly basis, though some lenders might adjust monthly. In a 2026 economy where inflation or Federal Reserve policy might shift, a variable rate carries risk. If the Prime Rate climbs, your monthly payment climbs with it. This can squeeze your working capital during a seasonal slowdown.

Fixed rates provide a different kind of value: predictability. You lock in one rate for the entire life of the loan. While fixed rates are often slightly higher at the start, they protect your cash flow from market volatility. If you’re planning a long-term project with tight margins, locking in a rate might be the safer bet. If you’re unsure which structure fits your current revenue, you can prequalify for business funding to see what specific offers look like for your situation. Choosing between the two often comes down to whether you prefer a lower rate today or a guaranteed payment tomorrow.

Current Rate Comparison: 7(a) vs. 504 vs. Microloans

Choosing the right program isn’t just about how much capital you need. It’s about what you plan to do with the money. The SBA categorizes loans based on the “use of proceeds,” and this choice directly dictates your interest costs. In 2026, sba loan rates continue to reflect the Federal Reserve’s efforts to balance growth, making the distinction between short-term capital and long-term asset financing more critical than ever for your bottom line.

Here is a snapshot of the typical rate ranges you’ll see in the 2026 market:

- SBA 7(a) Loans: 11.5% to 15.0% (Variable)

- SBA 504 Loans: 6.8% to 8.5% (Fixed)

- SBA Microloans: 13.0% to 16.0% (Fixed)

SBA 7(a) Rates for Working Capital

The 7(a) program is the SBA’s most popular tool because it’s incredibly flexible. If you need to stock up on inventory for a seasonal peak or cover payroll during a expansion phase, an SBA 7(a) working capital loan is usually the primary tool. These loans are also excellent for debt refinancing to improve monthly cash flow. For 2026, these rates typically land between 11.5% and 15% depending on your credit profile and the loan size. If you opt for an SBA Express loan to get faster processing, expect a slightly higher rate, usually 4.5% to 6.5% over the prime rate, as a trade-off for the speed.

504 Loans for Real Estate and Equipment

If you’re buying a warehouse or heavy machinery, the 504 program offers significantly more stability. It uses a unique two-part structure where a private bank covers 50% of the project, a Certified Development Company (CDC) covers 40% through a debenture, and you provide a 10% down payment. This structure allows for fixed, below-market sba loan rates that are often 2% to 4% lower than 7(a) options. However, these lower rates come with specific requirements. You’ll generally need to show that the project creates or retains one job for every $75,000 borrowed, though this limit increases to $120,000 for small manufacturers.

Microloans serve a different niche, providing up to $50,000 for very small businesses or startups. These are managed by community-based non-profit lenders who provide extra coaching and support. Because the loan amounts are smaller and the risk is often higher, the rates sit between 13% and 16% in 2026. They’re more expensive than a 504 loan, but they’re often the only viable path for an entrepreneur who doesn’t have years of tax returns or substantial collateral to pledge.

The Real Cost of Borrowing: Beyond the Interest Rate

When you look at sba loan rates, it is easy to focus solely on the percentage attached to the principal. However, the interest rate is just one piece of the puzzle. To understand what you will actually pay each month, you have to look at the Annual Percentage Rate (APR). This figure bundles the interest rate with mandatory fees and closing costs, providing a more honest look at your total capital expense. If your base rate is 9% but you are paying 3% in upfront fees, your APR is significantly higher than the headline number suggests.

You also have to account for the “cost of time.” SBA loans are notorious for their lengthy approval cycles, often stretching between 60 and 90 days. For a business owner trying to seize a sudden growth opportunity or purchase inventory for a peak season, a three-month wait can be expensive. If waiting for an SBA approval means losing a contract worth $50,000 in profit, that delay is a hidden cost that doesn’t show up on a bank statement but hits your bottom line just as hard.

Common SBA Fees You Need to Budget For

The SBA charges a guaranty fee to offset the cost of the program to taxpayers. For loans over $150,000, this fee typically ranges from 2.25% to 3.75% of the guaranteed portion of the loan. While this can often be rolled into the loan amount, it still increases your total debt. You should also expect ongoing servicing fees, which are usually around 0.55% of the outstanding balance, baked directly into your monthly payments.

Closing costs can also take a bite out of your working capital. Depending on the loan type, you might pay for commercial appraisals costing $2,000 to $5,000, environmental studies, and legal fees. Some business owners hire consultants to manage the mountain of paperwork; these “packaging fees” are regulated by the SBA but still represent an out-of-pocket expense you must plan for before the funds hit your account.

Qualification Hurdles That Impact Your Terms

Your specific sba loan rates aren’t just determined by the market; they are heavily influenced by your risk profile. Lenders use the FICO SBSS score to pre-screen applicants, and a score below 155 often leads to an immediate rejection or much higher spreads. A “spread” is the additional percentage a bank adds on top of the Prime Rate. If your credit is borderline, the bank might charge the maximum allowed spread, making the loan significantly more expensive over its 10 or 25-year life.

Collateral also plays a major role in the terms you receive. While the SBA doesn’t always require a loan to be “fully secured” to get an approval, lenders are much more likely to offer their lowest spreads when you can back the debt with real estate or equipment. If the loan is under-collateralized, the lender perceives higher risk and will price the loan accordingly. To see where your business stands before committing to the long application process, you can check your prequalification status to get a clearer picture of your options.

Ready to see which funding path makes the most sense for your current cash flow? Explore our business funding options to compare SBA loans with faster alternatives.

When an SBA Loan Isn’t the Right Fit (and Your Alternatives)

SBA loans are often called the gold standard of business financing, but they aren’t a universal fix. There is a specific challenge known as the “SBA Gap.” This happens when a business needs capital in three days, but the bank needs three months. While 2026 sba loan rates remain a benchmark for affordability, the trade-off is a heavy administrative burden and a long wait time. If you’re facing a sudden equipment breakdown or a flash sale on inventory that expires in 48 hours, a government-backed loan won’t move fast enough.

Choosing an alternative often means accepting a higher rate in exchange for speed and accessibility. It’s helpful to view these options as strategic tools rather than permanent debt. You might use a short-term bridge to cover a seasonal spike and then pay it off once the peak passes. When comparing a traditional sba loan rates structure to a factor rate or a line of credit, don’t just look at the percentage. Look at the total dollar cost of the capital and how much revenue that capital will help you generate.

Speed vs. Cost: The Case for Short-Term Funding

A short-term business loan is designed for agility. These products can often be funded within 24 to 72 hours, which is a lifetime away from the 60 to 90 days common in the SBA world. One major benefit is the collateral requirement. Many alternative lenders don’t require you to pledge your personal residence, providing a level of personal security that SBA 7(a) loans often lack.

Think about your “opportunity ROI.” If a short-term loan helps you secure a bulk inventory discount or a new contract worth 10 times the interest cost, the higher rate is a secondary concern. The goal is to solve a specific cash flow problem quickly so you can get back to running your business without the weight of a months-long application process.

Flexible Options for Fluctuating Revenue

Traditional loans don’t always play well with seasonal businesses. If your sales vary from month to month, Revenue-Based Financing might be a better fit than a rigid bank loan. This structure allows your payments to fluctuate based on your actual sales volume, taking the pressure off during slow periods.

For businesses that rely heavily on credit card transactions, Merchant Cash Advances provide capital in exchange for a portion of future sales. It’s a straightforward way to access working capital without the strict credit requirements of a bank. At Kredline, we act as a navigator to help you compare these different paths. We believe you shouldn’t have to guess which option is best. We provide the clarity you need to see how these alternatives stack up against traditional funding, ensuring you make a decision that supports your long-term stability.

Choosing the Right Path for Your Business Growth

Navigating the financial landscape of 2026 requires more than just a glance at the headline numbers. You’ve seen how sba loan rates are only one piece of a larger puzzle. The true cost of capital involves factoring in origination fees and closing costs that can shift your monthly math significantly. Whether you’re eyeing a 7(a) loan for seasonal payroll or a 504 for a new facility, the key is finding a structure that protects your daily cash flow. Sometimes the best move isn’t an SBA loan at all; if you’re bridging a gap between invoices or need equipment fast, alternative options might offer the speed your business requires.

You don’t have to navigate these choices alone. Our team provides access to a network of 50+ lenders and dedicated funding advisors who understand the practical challenges of running a company. We focus on making the process transparent and stress-free so you can get back to your operations. Prequalify for business funding in minutes; compare SBA and alternative options today. Our no-obligation process won’t hurt your credit score. You’ve built something great, and with the right funding partner, there’s no limit to how far you can take your vision.

Frequently Asked Questions

What is the current Prime Rate for SBA loans in 2026?

The Prime Rate for 2026 fluctuates based on Federal Reserve policy, but it typically follows the benchmark set by the Wall Street Journal. As of early 2026, lenders use this base rate to calculate your specific sba loan rates by adding a negotiated spread. You should check the current WSJ Prime Rate daily, as even a 0.25% shift can change your monthly payment significantly over a ten year term.

Can I get an SBA loan with a credit score below 680?

You can qualify for an SBA loan with a score below 680, though the process requires more documentation of your business’s health. While many traditional banks prefer a 640 to 680 minimum, the SBA doesn’t set a strict floor for the 7(a) program. Lenders will look closely at your debt-to-income ratio and whether your business has generated consistent revenue over the last 24 months to offset a lower personal score.

How long does it actually take to get funded after my SBA rate is quoted?

It usually takes between 30 and 90 days to see funds in your account after you receive a rate quote. SBA Express loans are the fastest option, often closing within 30 days for working capital needs. Standard 7(a) loans for real estate take longer because they require third-party appraisals and environmental reports that can add four weeks to the timeline.

Are SBA loan rates fixed or variable?

SBA loans offer both options, but the majority of 7(a) loans use variable sba loan rates that adjust quarterly. These rates are tied to the Prime Rate, meaning your payment could increase if the Federal Reserve raises interest levels. If you prefer a fixed rate for long term stability, the SBA 504 program is a better fit for purchasing heavy equipment or real estate.

What is the maximum interest rate an SBA lender can charge?

The SBA limits the maximum spread a lender can add to the Prime Rate to protect small business owners. For loans over $50,000 with a maturity of seven years or longer, the maximum rate is currently capped at Prime plus 2.75%. Smaller loans under $25,000 can have higher spreads, sometimes reaching Prime plus 6.50%, to cover the lender’s administrative costs.

Do SBA loans require a personal guarantee from all owners?

Every individual who owns 20% or more of the business must provide an unconditional personal guarantee. This legal commitment means you’re responsible for the debt if the business can’t make its payments. If no single person owns a 20% stake, the lender will usually require at least one person to provide a guarantee to ensure someone is personally accountable for the loan.

Is there a penalty for paying off an SBA loan early?

Prepayment penalties only apply to SBA loans with terms of 15 years or more, such as real estate debt. If you pay off the loan within the first three years, you’ll face a fee: 5% in the first year, 3% in the second, and 1% in the third. Most working capital and equipment loans have shorter terms and don’t carry any penalty for early payoff.

How do SBA rates compare to a standard business line of credit?

SBA rates are almost always lower than a standard business line of credit, which can carry interest rates 5% to 10% higher than government-backed options. A line of credit is better for short term gaps like waiting for a 30 day invoice to clear, but it’s much more expensive for long term growth. Kredline can help you look at both options to see which one protects your cash flow best as you scale.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.