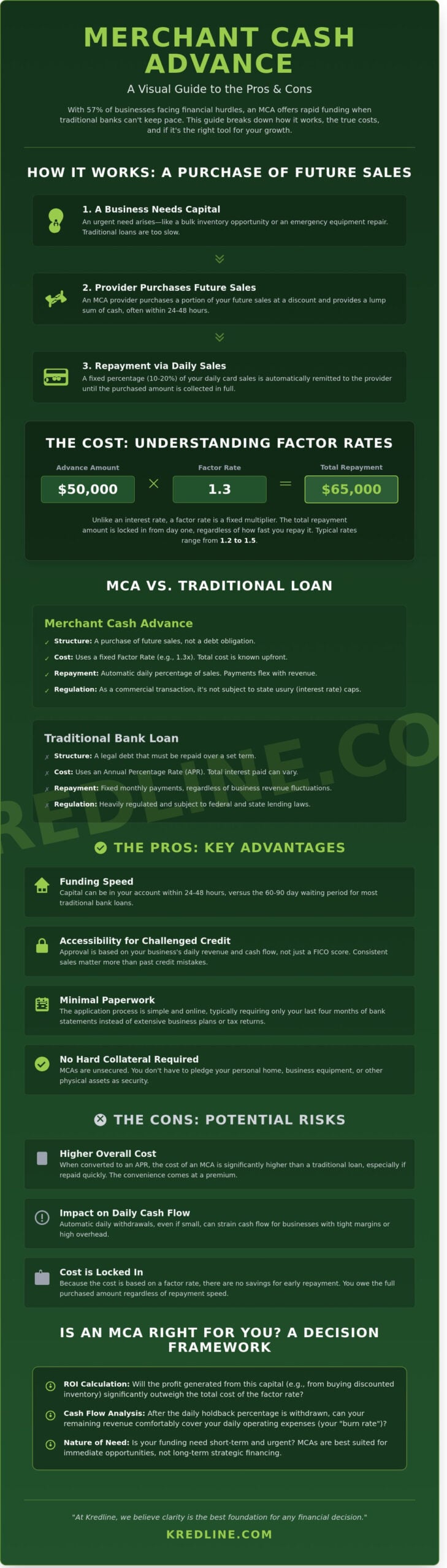

Recent data from the 2024 Small Business Credit Survey shows that 57% of firms face persistent financial challenges, yet traditional bank approval remains a slow, uphill battle. This is why many owners weigh the merchant cash advance pros and cons when they need to move faster than a standard loan allows. You’ve likely felt that frustration when a growth opportunity appears, but your bank’s paperwork mountain stands in the way. It’s exhausting to wait weeks for an answer while your seasonal revenue fluctuates and your credit score doesn’t tell the full story of your company’s health.

We understand that when you need working capital to bridge an invoice gap or stock up for a busy season, you don’t have time for red tape. This guide provides a transparent breakdown of how these advances work so you can decide if this alternative is a tool or a trap. We’ll strip away the jargon to reveal the real costs and how these funding options actually impact your bottom line in 2026.

At Kredline, we believe clarity is the best foundation for any financial decision. We’ll explore the mechanics of daily remittances, the reality of factor rates, and a simple framework to determine if this funding aligns with your specific goals. By the end, you’ll know exactly how to evaluate an offer without the usual stress or sales pressure.

Key Takeaways

- Understand why an MCA is technically a purchase of future sales rather than a traditional loan, and how this structure affects your legal protections.

- Navigate the merchant cash advance pros and cons to determine if the benefit of 24-hour funding justifies the higher costs and daily cash flow impact.

- Compare MCAs against alternatives like business lines of credit to identify which funding source best aligns with your specific growth goals.

- Apply a simple ROI framework to calculate whether the profit generated by the new capital will outweigh the total cost of the factor rate.

- Learn how to evaluate your “burn rate” to ensure your remaining daily revenue can comfortably cover overhead after automatic withdrawals.

Understanding the Merchant Cash Advance (MCA) Structure

A merchant cash advance isn’t a loan in the traditional sense. It’s technically a commercial transaction where a funding provider purchases a specific portion of your future credit card or debit card sales at a discount. Because this is a purchase of an asset (future revenue) rather than a borrowed sum of money, it doesn’t carry the same legal obligations as a bank loan. This distinction is vital because it means MCAs aren’t subject to state usury caps that limit interest rates on standard debt products. When weighing the merchant cash advance pros and cons, you have to start with how the money is actually classified.

This structure is specifically designed for businesses that process a high volume of card transactions but might lack physical collateral like real estate or heavy machinery. Retailers, restaurants, and service providers often use this to manage working capital. The Purchase Price represents the immediate cash injection a business receives, while the Total Repayment Amount is the predetermined sum of future sales the provider now owns. For a deeper dive into the history and regulatory environment of this industry, Understanding the Merchant Cash Advance (MCA) Structure via Wikipedia provides a helpful foundation.

How an Advance Differs from a Traditional Loan

In a standard loan, you have a legal obligation to repay a debt over a set period. With an MCA, the funder takes ownership of your future receivables. There is no fixed maturity date or “term” in the contract; the agreement stays active until the funder collects the full amount of purchased sales. You won’t find an interest rate here. Instead, providers use factor rates to determine the cost. This means the total amount you owe is locked in from day one, regardless of how long it takes to pay it back. If you’re looking for more traditional debt options, a short-term business loan might be a better fit for your needs.

The Role of Factor Rates and Future Sales

Factor rates typically range from 1.2 to 1.5. If you receive $50,000 at a 1.3 factor rate, your total repayment amount is $65,000. This doesn’t change even if your sales skyrocket or dip. Repayment happens through a “holdback percentage,” which is a fixed portion of your daily card sales, often between 10% and 20%. This is where the flexibility shines. On a slow Tuesday, if you only process $500 in sales, a 10% holdback is just $50. On a busy Saturday with $5,000 in sales, the payment jumps to $500. Understanding these mechanics is the first step in evaluating merchant cash advance pros and cons for your specific business model. This revenue-aligned approach ensures your payments stay proportional to what you’re actually earning each day.

The Pros: Why Business Owners Choose MCAs

When you look at merchant cash advance pros and cons, speed is usually the first thing that stands out. Traditional bank loans often involve a 60 to 90 day waiting period. In contrast, an MCA can put capital into your account within 24 to 48 hours. This makes it a tool for urgent needs, like a sudden refrigerator breakdown in a restaurant or an unexpected bulk inventory discount that expires in three days.

Security is another major draw. Unlike traditional term loans, an MCA doesn’t require you to pledge your personal home or business equipment as primary security. This lack of collateral requirements protects your physical assets if sales take an unexpected dip. Because the provider is purchasing a portion of your future sales, the evaluation focuses on your bank statements rather than a stack of property deeds.

The merchant cash advance pros and cons often center on the application process itself. You can usually finish everything online using only your last four months of bank statements. You won’t need to draft a complex business plan or provide three years of audited tax returns like you would for a bank. This simplicity saves dozens of hours of administrative work for busy owners.

Accessibility for Challenged Credit

Traditional lenders often reject applicants with a FICO score below 680. MCAs look at the bigger picture. If your business generates consistent daily revenue, a provider cares more about that cash flow than a credit mistake from five years ago. This makes it a bridge for owners who have the revenue to grow but don’t fit the rigid bankable mold. It’s a way to prove repayment ability through actual sales rather than an arbitrary score.

Flexible Repayment During Slow Periods

The pay-as-you-earn model is built for seasonal industries. If you run a retail shop and sales drop 30% in January, your payment drops too. You aren’t stuck with a fixed monthly bill that drains your reserves during a slow month. This structure keeps your cash flow breathing when you need it most. While these advantages are clear, balance is necessary. Part of Navigating the Risks and Costs involves understanding how these daily percentages impact your long-term margins.

If you’re curious about how this fits your specific revenue profile, you can explore our merchant cash advance options to see if the flexibility matches your business goals.

The Cons: Navigating the Risks and Costs

Speed and accessibility are the primary drivers for this type of funding, but they come with significant trade-offs. To balance the merchant cash advance pros and cons, you have to look at the total cost of capital. Unlike a traditional bank loan that might carry a 7% or 9% interest rate, an MCA uses a factor rate. If you receive a $50,000 advance with a 1.3 factor rate, you owe a total of $65,000. That $15,000 fee is locked in the moment you sign the contract. It doesn’t matter if your business explodes with growth or hits a temporary wall; that cost remains the same.

One of the biggest hurdles for small business owners is the lack of early payoff benefits. In most financing models, paying off a debt early saves you money on interest. With an MCA, the “interest” is actually a fixed purchase of your future sales. Paying the balance off in three months instead of six rarely reduces the total amount you owe. This makes it a rigid financial commitment compared to more flexible options like a business line of credit.

Daily cash flow strain is another reality. Most providers require daily or weekly ACH withdrawals directly from your bank account. If your revenue drops during a seasonal slump, these automatic payments don’t always stop. This can create a situation where you’re struggling to cover basic overhead or payroll because a chunk of your daily sales is already spoken for. It’s a high-pressure cycle that requires meticulous cash management.

- The Risk of Stacking: This occurs when a business takes out a second or third advance to cover the payments of the first. Industry data from 2024 suggests that stacking is a leading cause of business insolvency in the alternative lending space.

- Fixed Costs: You can’t “refinance” a factor rate to a lower rate later.

- No Collateral, but High Personal Risk: While these aren’t typically secured by physical assets, they often require a personal guarantee.

The Reality of APR Equivalents

Factor rates can be deceptive because they look like small numbers. A 1.2 factor rate sounds like 20%, but when you calculate the Annual Percentage Rate (APR) based on a six-month repayment term, that figure often climbs into the triple digits. It’s common to see effective APRs ranging from 60% to 150%. Before committing, use an APR calculator to compare the cost against a short-term business loan. Understanding the true yearly cost helps you decide if the projected ROI on your project justifies the expense.

Impact on Merchant Processing

Some MCA providers insist that you switch your credit card processing to their preferred partner. This “split-funding” method allows them to take their cut automatically from every card transaction. Beyond the administrative headache of switching systems, you should also expect a UCC-1 filing. This is a public notice that the lender has a legal claim to your business assets. A UCC-1 filing can lower your credit score and might prevent you from qualifying for other types of financing until the advance is fully settled. At Kredline, we often help business owners review these terms to ensure they aren’t accidentally blocking their future growth paths.

MCA vs. Other Funding Options: A Practical Comparison

Choosing the right capital source isn’t just about getting the money; it’s about how that money impacts your bottom line over the next six to twelve months. While the speed of an advance is tempting, weighing the merchant cash advance pros and cons requires a side-by-side look at more traditional alternatives. For many owners, the high cost of an MCA is a fair trade for speed, but for others, it can create a cycle of debt that’s hard to break.

If your business has a predictable monthly income and a credit score above 620, a Short-Term Business Loan often makes more sense. These loans provide a lump sum with a fixed repayment schedule. Unlike an MCA, which uses a factor rate, short-term loans usually have lower total interest costs. This is especially true for service-based businesses that don’t rely heavily on credit card sales but still need quick liquidity for a specific project or expansion.

For tech startups or companies with high growth but fluctuating monthly receipts, Revenue-Based Financing offers a middle ground. It functions similarly to an MCA by tying payments to your sales, but it often carries more favorable terms for businesses with high gross margins. According to the 2023 Small Business Credit Survey by the Federal Reserve, only 9% of small businesses chose MCAs, while 43% applied for lines of credit, suggesting that most owners prefer more structured, lower-cost options when they qualify.

When a Line of Credit is Better

A Business Line of Credit is the most effective tool for handling recurring gaps in payroll or inventory cycles. You don’t pay for the whole amount at once; you only pay interest on the funds you actually draw. If you have a $50,000 line but only use $5,000 to cover a late invoice, your costs stay low. While a line of credit requires stronger credit and more documentation than an MCA, the long-term savings are substantial for businesses with ongoing cash flow needs.

The Case for Equipment Funding

If you’re looking to add a delivery van or a new oven, don’t use an MCA. Dedicated Equipment Funding is almost always the better choice for machinery. Since the equipment itself serves as collateral, lenders can offer much lower rates than an unsecured advance. You also get the benefit of Section 179 tax deductions, which allow you to write off the full purchase price of qualifying equipment in the year you buy it. This can save a business thousands of dollars in tax liability that an MCA simply can’t offer.

Every business has different needs, and the best way to find your fit is to look at the numbers. You can prequalify for business funding today to see which of these options matches your current revenue and goals.

Is an MCA Right for You? A Decision Framework

Choosing a merchant cash advance isn’t about finding the lowest interest rate. Since these aren’t traditional loans, the decision relies on speed and the specific return on investment you can generate with the capital. You have to weigh the merchant cash advance pros and cons against your immediate business needs. If the funding allows you to capture a profit that exceeds the cost of the factor rate, the math usually works in your favor.

Before you sign, check your daily “burn rate.” An MCA is repaid through a percentage of your daily sales. You must ensure your remaining revenue covers your fixed costs like rent, utilities, and payroll. According to a 2023 Federal Reserve report on small business credit, 37% of firms used financing to cover operating expenses, but those who used it for growth often saw better long-term stability. Ensure your cash flow can handle the daily or weekly “holdback” without choking your operations.

Calculating Your ROI on the Advance

Imagine a scenario where a supplier offers you a 40% bulk discount on $50,000 worth of inventory if you pay upfront. If you don’t have the cash, you miss out on $20,000 in savings. If an MCA costs you $12,000 in total fees to get that $50,000 immediately, you still come out $8,000 ahead. In this case, the “cost of doing nothing” is higher than the cost of the capital. To determine if a growth opportunity justifies the funding cost, divide your projected net profit from the investment by the total cost of the advance.

How to Prequalify and Compare Offers Safely

The safest way to navigate the merchant cash advance pros and cons is to avoid “one-and-done” lenders who pressure you into high-fee contracts. Using a marketplace like Kredline allows you to see offers from multiple vetted providers simultaneously. This creates competition for your business, which often leads to better factor rates and more flexible terms. It also protects your credit score, as you can see your real numbers before committing to a hard pull.

Before you finalize any agreement, ask the following questions to flush out hidden costs:

- What is the total “buy rate” versus the “sell rate” after all fees are included?

- Are there administrative or origination charges taken out of the initial funding amount?

- Is there a discount for early repayment, or is the factor rate fixed regardless of when you finish?

- Does the provider require a personal guarantee or a lien on business assets?

If you’re ready to see what your business qualifies for without any obligation, the next step is simple. You can prequalify for business funding to explore your options and see exactly how much capital you can access to fuel your next growth phase.

Moving Your Business Forward with Confidence

Deciding on your next funding move requires balancing immediate capital needs with your company’s long-term health. We’ve explored the merchant cash advance pros and cons to help you see where this speed fits into your growth strategy. While rapid access to funds helps with urgent payroll or inventory, the higher costs require a clear plan for repayment. Data from the Federal Reserve’s 2023 Small Business Credit Survey shows that 57% of firms faced credit shortfalls. Knowing your alternatives is vital for stability.

You don’t have to navigate these complex financial waters alone. Kredline provides specialized expertise in revenue-based financing through a national network of 3rd-party providers. Our process is built on fast, transparent brokerage. We respect your boundaries and avoid the pressure of traditional personal loans. We’re here to help you translate these funding options into a solution that matches your actual daily revenue.

Explore your funding options and prequalify with Kredline today

Your next growth phase is well within reach when you have the right information and a reliable partner by your side.

Frequently Asked Questions

Is a merchant cash advance considered a loan?

Technically, a merchant cash advance isn’t a loan. It’s a commercial transaction where a provider purchases a specific dollar amount of your future sales at a discount. Because it’s a purchase of assets rather than a high-interest loan, it isn’t subject to the same federal usury laws that cap interest rates on traditional bank products. You’re selling a portion of your future revenue in exchange for immediate working capital.

How much does a merchant cash advance typically cost?

The cost is determined by a factor rate, which generally ranges from 1.1 to 1.5 depending on your business’s health and industry. If you receive $20,000 with a 1.25 factor rate, your total repayment will be $25,000. It’s vital to analyze the merchant cash advance pros and cons before signing, as the effective annual percentage rate can often exceed 50% when the repayment period is short.

Will an MCA affect my personal credit score?

Most providers perform a soft credit pull during the application phase, which doesn’t impact your score at all. Since the advance is based on your business’s daily sales volume, it usually doesn’t appear on your personal credit report as a debt obligation. However, if you sign a personal guarantee and the business fails to pay, the provider might seek a judgment that could eventually show up on your credit file.

Can I get a merchant cash advance with a 500 credit score?

Yes, you can often qualify with a credit score as low as 500 because providers care more about your cash flow than your past credit mistakes. Most companies look for at least $10,000 in monthly deposits and at least 6 months in business. While a lower score might result in a higher factor rate, the accessibility makes this a common choice for owners who can’t secure traditional bank financing.

What happens if my business has a slow month and I can’t pay?

If your advance is structured as a percentage of daily credit card sales, your payments will naturally decrease during slow periods. This flexibility is a core benefit, as the provider only takes their cut when you actually make a sale. If you have a fixed ACH daily withdrawal and hit a rough patch, you should contact the provider immediately to request a payment adjustment based on your current bank balances.

Can I have more than one merchant cash advance at a time?

You can technically have multiple advances, which the industry calls “stacking,” but it’s a risky financial move. Taking a second or third advance can quickly drain your daily operating cash and put your business’s survival at risk. If you’re feeling overwhelmed by multiple daily payments, Kredline can help you look into consolidation options that might offer a more sustainable monthly schedule.

Are merchant cash advances legal in all 50 states?

Merchant cash advances are legal across the United States, though transparency laws have changed significantly in certain regions. For example, California and New York passed regulations in 2022 and 2023 that require providers to provide clear disclosures about the total cost of capital. These laws help business owners better understand the merchant cash advance pros and cons by standardizing how pricing is presented during the offer stage.

How long does it take to get approved for an MCA?

The approval process is incredibly fast, often taking less than 24 hours from the moment you submit your bank statements. In many cases, you can receive an offer within 3 or 4 hours and see the funds in your business account by the next business day. This speed makes it a go-to solution for urgent needs like emergency roof repairs or taking advantage of a limited-time inventory discount.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.