A 1.3 factor rate sounds significantly cheaper than a 30% interest rate, but that decimal point often hides the true impact on your daily bank balance. It’s a common trap for business owners who are trying to move fast. You see a small number and assume the cost is low, only to realize later that the math doesn’t work quite like a traditional bank loan. You shouldn’t have to feel like you’re gambling with your margins just to get the working capital you need to bridge a seasonal gap or cover a sudden equipment repair.

In this guide, we’ll get merchant cash advance factor rates explained so you can stop guessing and start calculating your total repayment with total certainty. You’ll gain a clear framework to determine if the cost of funding aligns with your projected ROI, helping you make decisions that actually fuel growth. At Kredline, we believe that transparency is the only way to build a real partnership. We’ll walk through the simple formulas you need to compare offers side by side and identify the most efficient path for your business’s cash flow.

Key Takeaways

- Learn why factor rates are a fixed cost based on your total principal, giving you a clear picture of your total repayment from day one.

- Understand the critical difference between static factor rates and compounding interest to avoid overestimating the cost of your capital.

- Get merchant cash advance factor rates explained in the context of your daily sales, showing how your holdback rate influences your effective interest.

- Identify the specific “risk buckets” lenders use to determine your rate and learn what steps you can take to qualify for more favorable terms.

- Determine if a speed-focused factor-rate product or a specialized option like equipment funding is the best fit for your current business goals.

What is a Factor Rate? The “Fixed Cost” of Business Funding

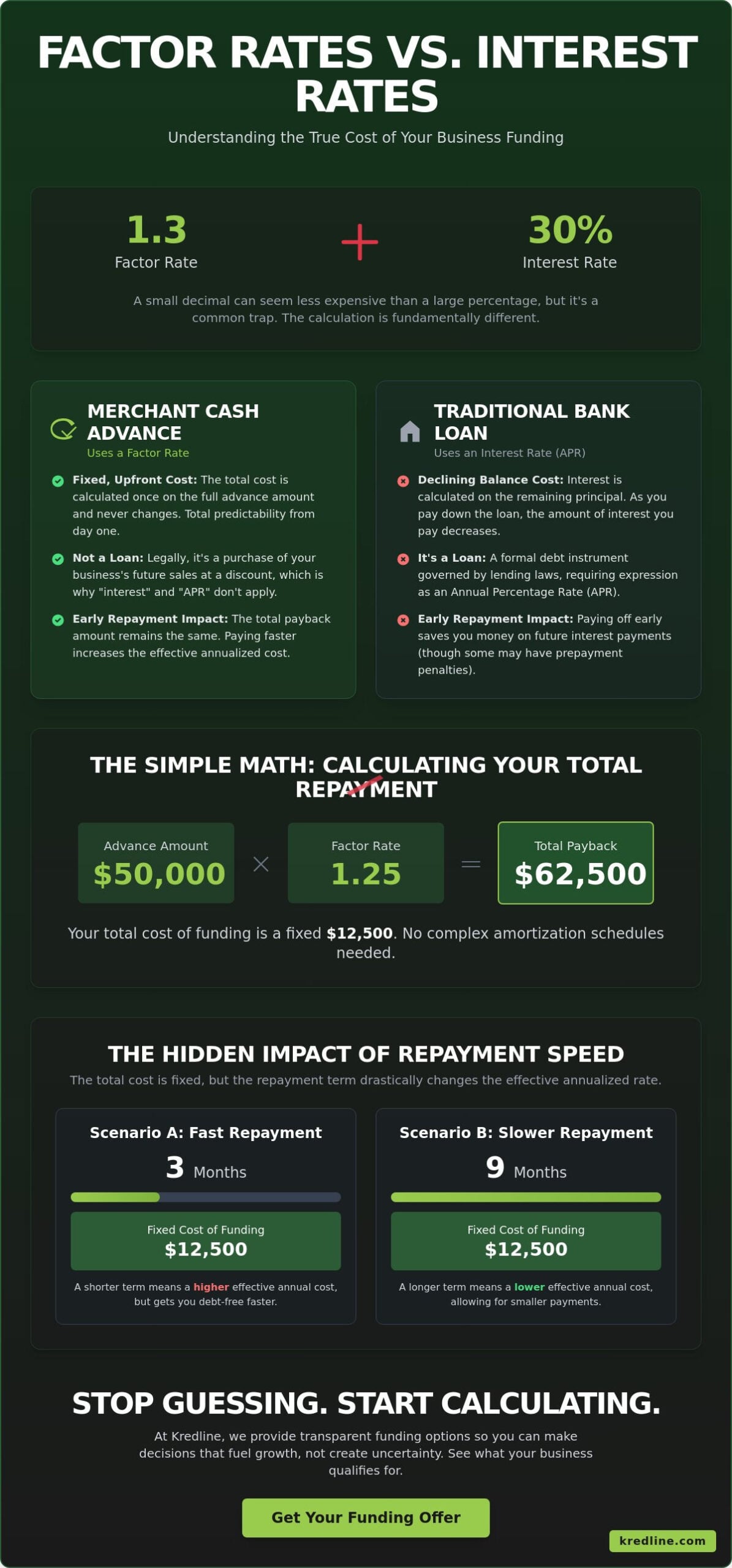

If you’ve spent years dealing with traditional banks, seeing a decimal instead of a percentage can be jarring. It’s a different language. A factor rate is a fixed multiplier used primarily in alternative finance to calculate the total cost of capital. Unlike an interest rate that fluctuates based on how much of the loan you’ve already paid back, a factor rate is static. It applies to the total principal from the moment the funds hit your account until the final dollar is returned. This model is the standard for products like a merchant cash advance or revenue-based funding. To get a better handle on the basics, you can read more about What is a Merchant Cash Advance? and how these structures operate outside the traditional banking system.

Most business owners feel a bit of “sticker shock” when they first see these numbers. A factor rate of 1.25 might look small, but it doesn’t represent 1.25% interest. It represents a 25% total cost on the money advanced. Because the cost is calculated on the original principal only, it never decreases as you pay down the balance. This is the core of having merchant cash advance factor rates explained: you’re paying for the convenience and speed of the capital with a fixed fee, not a variable interest charge.

The Simple Math: Calculating Your Total Repayment

One of the biggest advantages of this model is its predictability. You don’t need a complex calculator to figure out what you owe. The formula is: Advance Amount x Factor Rate = Total Payback. For example, if your business receives a $50,000 advance with a 1.25 factor rate, your total repayment amount is $62,500. You know this number before you sign any paperwork. There are no hidden amortization schedules or fluctuating monthly payments to track.

When reviewing your offer, you might hear the term “buy rate.” This is the base cost the funding source charges before any additional markups. The final factor rate offered to the merchant typically includes the buy rate plus any broker fees or administrative costs involved in securing the funding.

Why Lenders Use Decimals Instead of Percentages

The shift from percentages to decimals isn’t just a stylistic choice; it’s a legal one. A merchant cash advance isn’t technically a loan. It’s a purchase of your future business sales. Because it isn’t a loan, the terminology of “interest rates” and “APR” doesn’t apply in the same way. This distinction allows for more flexible repayment structures that align with your daily or weekly cash flow. It’s particularly common in revenue-based financing, where the lender’s return is tied directly to your sales volume.

The simplicity of the decimal system allows you to see the total cost upfront. You won’t have to worry about front-loaded interest or early payment penalties that can sometimes complicate traditional bank debt. For a busy owner managing payroll and inventory, knowing the exact “out the door” cost provides a level of clarity that helps in planning for the next quarter’s growth.

Factor Rates vs. Interest Rates: Why the Difference Matters

Most business owners think in terms of Annual Percentage Rate (APR) because that is how mortgages, car loans, and credit cards work. Merchant cash advances operate on a completely different logic. When merchant cash advance factor rates explained in simple terms, the biggest takeaway is that the cost is fixed. You aren’t paying interest on a balance that shrinks over time. Instead, you are selling a specific slice of your future sales for a set price.

Don’t assume a 1.2 factor rate is the same as a 20% interest rate. In a traditional loan, interest compounds or applies to whatever principal you still owe. If you pay a bank loan off early, you save money on interest. With an MCA, the factor rate is static. If you “buy” $50,000 of funding at a 1.3 factor rate, you owe $65,000. That $15,000 cost stays the same whether your sales allow you to pay it back in three months or nine months. Early repayment usually doesn’t offer the “interest savings” you might expect from a standard bank product.

The Declining Balance Trap

Traditional bank loans get cheaper as you pay them down. If you have a $100,000 term loan over five years, your monthly interest is calculated only on what you haven’t paid back yet. MCAs don’t follow this path. Because an MCA is a purchase of future receivables, the “fee” is baked into the total amount from the start. A retail shop taking a 6-month cash advance will pay the same total cost even if they have a record-breaking month and clear the obligation early. You should view this as a fixed cost of doing business rather than a fluctuating interest expense.

Converting Factor Rates to APR (And Why It Is Often Misleading)

If you try to annualize a factor rate, the numbers can look intimidating. For example, a 1.2 factor rate paid back over six months translates to an APR of roughly 40%. If your sales are fast and you pay it back in three months, that effective APR doubles. However, APR is often a poor tool for measuring short-term capital. If a business owner uses $20,000 to buy discounted inventory that generates $15,000 in clear profit within 90 days, the speed of the capital matters more than the annualized rate.

Instead of obsessing over APR, focus on the “Total Cost of Capital.” Ask yourself if the flat fee for the advance is lower than the profit you’ll generate using that money. This practical approach helps you decide if a merchant cash advance is the right tool for a specific growth opportunity or a temporary cash flow gap. Understanding merchant cash advance factor rates explained through the lens of total cost ensures you don’t pass up a profitable deal just because the math looks different than a mortgage.

The Hidden Impact of Repayment Speed on Your Bottom Line

When you look at a funding offer, the factor rate tells you the total cost, but it doesn’t tell you how fast that money leaves your bank account. That is determined by the holdback rate. This is a fixed percentage of your daily sales, usually ranging from 10% to 25%, that the funding company collects until the total balance is paid. Understanding this mechanism is vital to having merchant cash advance factor rates explained in a way that actually helps your business survive the repayment period.

There is a direct relationship between your sales volume and the “effective” cost of your capital. If your business has a record-breaking month, you’ll pay back the advance much faster. While clearing debt quickly sounds like a win, it technically increases your annualized interest rate because you’ve had the use of the funds for a shorter period. The trade-off is simple: high-velocity repayment gets you out of debt sooner, but it puts more pressure on your daily operating cash. You have to decide if your daily margins can handle a 15% or 20% “haircut” on every dollar that comes through the door.

The most common question owners ask is whether the cost is worth the speed. The answer isn’t found in the factor rate itself, but in the opportunity the money creates. If the funds allow you to buy inventory that will double your revenue in 60 days, a 1.25 factor rate is a minor hurdle. If the funds are just covering up a permanent leak in your business model, the speed of repayment will only make that leak harder to manage.

ROI vs. Cost of Capital

Imagine a restaurant owner who finds a high-end commercial oven at a liquidation sale for $10,000, normally priced at $18,000. Even with a factor rate of 1.30, the total cost of $13,000 is still significantly lower than the market value of the equipment. Using revenue-based financing to bridge this gap makes sense because the immediate ROI is 80% higher than the cost of the capital. You should only move forward with factor-rate funding when the projected profit margin from the investment clearly exceeds the total factor cost.

Managing Daily Cash Flow with ACH Debits

Most repayments happen via automated clearing house (ACH) withdrawals, which pull funds directly from your business checking account daily or weekly. To avoid the stress of an overdrawn account, it’s smart to maintain a cash buffer equal to at least three days of repayments. You should also monitor your seasonal trends closely; a holdback rate that feels easy in July might feel suffocating during a slow October. Kredline works with owners to explore short-term business loans and other structures that provide more predictable, manageable repayment schedules that won’t cripple your daily operations.

How Lenders Determine Your Factor Rate (And How to Get a Lower One)

Lenders don’t pull factor rates out of thin air. They use a specific set of “risk buckets” to categorize your business. When merchant cash advance factor rates explained in simple terms, it comes down to how likely the lender thinks they are to get their money back on schedule. The higher the perceived risk, the higher the rate you’ll pay for the capital.

Industry type is one of the first things a lender looks at. If you run a construction company, you might see higher factor rates than a retail shop. This isn’t personal; it’s based on data. Construction often involves long payment cycles, such as Net-60 or Net-90 terms, which creates gaps in cash flow. Lenders prefer businesses with high-frequency, smaller transactions because they provide a steadier stream for daily or weekly remittances. Your credit score and time in business also weigh heavily. According to data from the Bureau of Labor Statistics, approximately 20% of small businesses fail within their first year. If you’ve crossed the two-year mark, you’ve already moved into a more favorable risk bucket.

Your bank statements tell the real story. Lenders analyze your average monthly deposits to ensure you have enough “cushion” to handle the advance. They also look for existing UCC filings. A Uniform Commercial Code (UCC) filing means another lender already has a legal claim to your business assets. If you have multiple filings, it signals that your revenue is already stretched thin, which almost always results in a higher factor rate.

The 3 Pillars of a Low Factor Rate

Securing a competitive rate requires proving your business is a safe bet. Pillar 1 is consistent revenue. Lenders want to see steady deposits rather than “lumpy” cash flow where one month is great and the next is empty. Pillar 2 is maintaining clean bank statements. Even a single Non-Sufficient Funds (NSF) flag in a 90-day period can disqualify you from the best rates. Pillar 3 is your operational history. Businesses with five or more years of continuous operation typically access the lowest tiers of funding.

Preparing Your Business for a Funding Application

Preparation is the difference between a 1.15 and a 1.45 factor rate. Before you apply, gather your last four to six months of business bank statements and your most recent tax return. If you accept credit cards, have your processing statements ready to show your monthly volume.

Timing is also vital. You should apply when your sales are trending upward, not when you’re in the middle of a cash crunch. Lenders view a business with growing month-over-month revenue as a much lower risk. To get a clear picture of where you stand, you can prequalify for business funding to see potential rates without a hard pull on your credit report. This allows you to compare options without damaging your score.

Ready to see what rates your business qualifies for? Check your funding options today and get a decision in as little as 24 hours.

Choosing the Right Funding Path for Your Growth

Factor rate products aren’t a one-size-fits-all solution, but they fill a vital gap for many small businesses. If you need capital within 24 to 48 hours to grab a bulk inventory discount or repair a delivery truck, the speed of a Merchant Cash Advance (MCA) often outweighs the higher cost. These products work effectively if your credit score is below 600 or if you lack physical assets like real estate to pledge as collateral. You’re essentially trading a portion of your future sales for immediate liquidity today.

However, an MCA isn’t always the most efficient choice for every scenario. If you’re looking to buy a specific piece of machinery or a vehicle, equipment funding usually provides better terms because the asset itself secures the deal. This lowers the risk for the lender and typically results in a lower overall cost than a product based on factor rates. Matching the right tool to the right job is the key to maintaining healthy margins.

Finding the best deal shouldn’t feel like a guessing game or a high-pressure sales pitch. As we’ve seen in this guide where merchant cash advance factor rates explained the total cost of capital, the difference between a 1.2 and a 1.4 factor can mean thousands of dollars in extra costs. We act as your navigator at Kredline, comparing multiple offers simultaneously to find the lowest factor rate your business qualifies for. Our goal is to simplify the process so you can focus on operations rather than paperwork.

Think of short-term capital as a bridge. Using a well-timed injection of cash to fulfill a large contract can boost your revenue and bank balances. Over time, this improved cash flow helps you qualify for lower-cost traditional loans. It’s a strategic stepping stone toward a stronger financial profile and long-term creditworthiness.

When to Walk Away from an Offer

A factor rate above 1.5 is a major red flag for most industries unless your profit margins are exceptionally high and the ROI is guaranteed. If a lender refuses to show you the total payback amount in plain English, stop the conversation immediately. Transparency is non-negotiable. If you receive an offer that feels steep, don’t be afraid to use it as a counter-offer. We often help clients use a standing offer to negotiate a lower factor or more manageable repayment terms with another lender in our marketplace.

Next Steps: Evaluating Your Options

Take a moment to run your own numbers using the formulas we provided earlier. Match the funding type to your specific hurdle; don’t use a high-cost MCA for a long-term project that won’t see a return for years. You can explore our full range of funding options to see what aligns best with your current cash flow. When you’re ready to see what’s available for your business, you can prequalify online without any obligation or impact on your credit score.

Take Control of Your Business Funding Strategy

Understanding how factor rates work is the first step toward making a smart financial move for your company. Unlike traditional loans where interest builds over time, a factor rate gives you a clear view of the total cost from day one. You’ll know exactly what you owe. This makes planning for payroll or equipment purchases much simpler. This merchant cash advance factor rates explained guide shows that while these rates are fixed, the speed of your sales directly impacts your daily cash flow. Choosing the right partner means looking beyond just the number on the page.

You don’t have to navigate these numbers alone. Kredline provides access to a national network of 50+ specialized lenders to ensure you find a fit for your specific industry. You can see what rates your business qualifies for today with Kredline through a no-obligation prequalification that requires no hard credit pull. Our expert advisors are ready to explain the fine print before you sign anything. Your business deserves a path to growth that feels manageable and clear.

Frequently Asked Questions

What is a typical factor rate for a merchant cash advance in 2026?

Most business owners encounter factor rates between 1.15 and 1.45 in the current 2026 market. If you receive an advance of $50,000 at a 1.2 factor rate, your total repayment amount is $60,000. These rates fluctuate based on your industry’s risk level and your average monthly credit card volume. Lower rates are usually reserved for businesses with at least 24 months of stable operating history.

Can I negotiate a factor rate after receiving an offer?

You can definitely negotiate your factor rate before you sign the final agreement. Lenders are often willing to lower the multiplier if you provide 6 months of strong bank statements or agree to a shorter repayment window. It’s smart to show consistent daily balances to prove you’re a low-risk partner. Kredline experts suggest comparing at least two different offers to use as leverage during your conversation with a funder.

Does a factor rate ever change during the life of the advance?

No, your factor rate is locked in when you sign the contract and stays the same until the balance is cleared. This is a primary benefit for those seeking merchant cash advance factor rates explained simply; the total cost is fixed. Unlike a traditional bank loan where interest might compound or fluctuate with market shifts, your total payback amount won’t grow. You’ll know exactly what you owe from the first day.

Is a factor rate the same as a flat interest rate?

A factor rate isn’t the same as an interest rate because it’s calculated only once on the original advance amount. Interest rates apply to a declining principal balance, which means the dollar amount of interest drops as you pay. With a 1.3 factor rate, you pay the same $3,000 fee on a $10,000 advance regardless of how long it takes to pay back. This distinction is vital for calculating your true ROI.

What happens to my factor rate if my sales slow down?

Your factor rate remains unchanged if sales slow down, but your daily payment amount will likely decrease. Since payments are usually a fixed percentage of your daily sales, a dip in revenue means you pay less that day. This structure protects your cash flow during seasonal slumps, such as a restaurant seeing fewer customers in January. The only catch is that it will take more time to reach your total payback goal.

Are there other fees besides the factor rate I should look for?

You should watch for origination fees and administrative costs that typically range from 1% to 5% of the total funding. Some providers also charge a one-time “documentation fee” of $200 to $500 or monthly maintenance fees. Always ask for a closing statement that lists every charge. This ensures you understand the total cost of capital beyond the base factor rate before committing your business to the deal.

Can I pay off a factor-rate advance early to save money?

Paying off an advance early doesn’t usually reduce your costs because the fee is a fixed multiplier of the original amount. If your contract says you owe $13,000, that’s the amount due whether you pay in two months or ten. However, some lenders offer a “prepayment discount” or “early payoff addendum” that can shave 5% to 15% off the remaining balance. Always check your contract for these specific clauses before sending a lump sum.

How does my credit score impact the factor rate I am offered?

Your credit score influences the rate, but lenders prioritize your 12 months of revenue and daily bank balances over a single number. A score above 620 often helps you secure rates near 1.18, while scores below 580 might lead to rates of 1.40 or higher. Lenders use your score to gauge personal financial responsibility, but they care more about whether your business generates enough daily cash to support the repayment schedule.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.