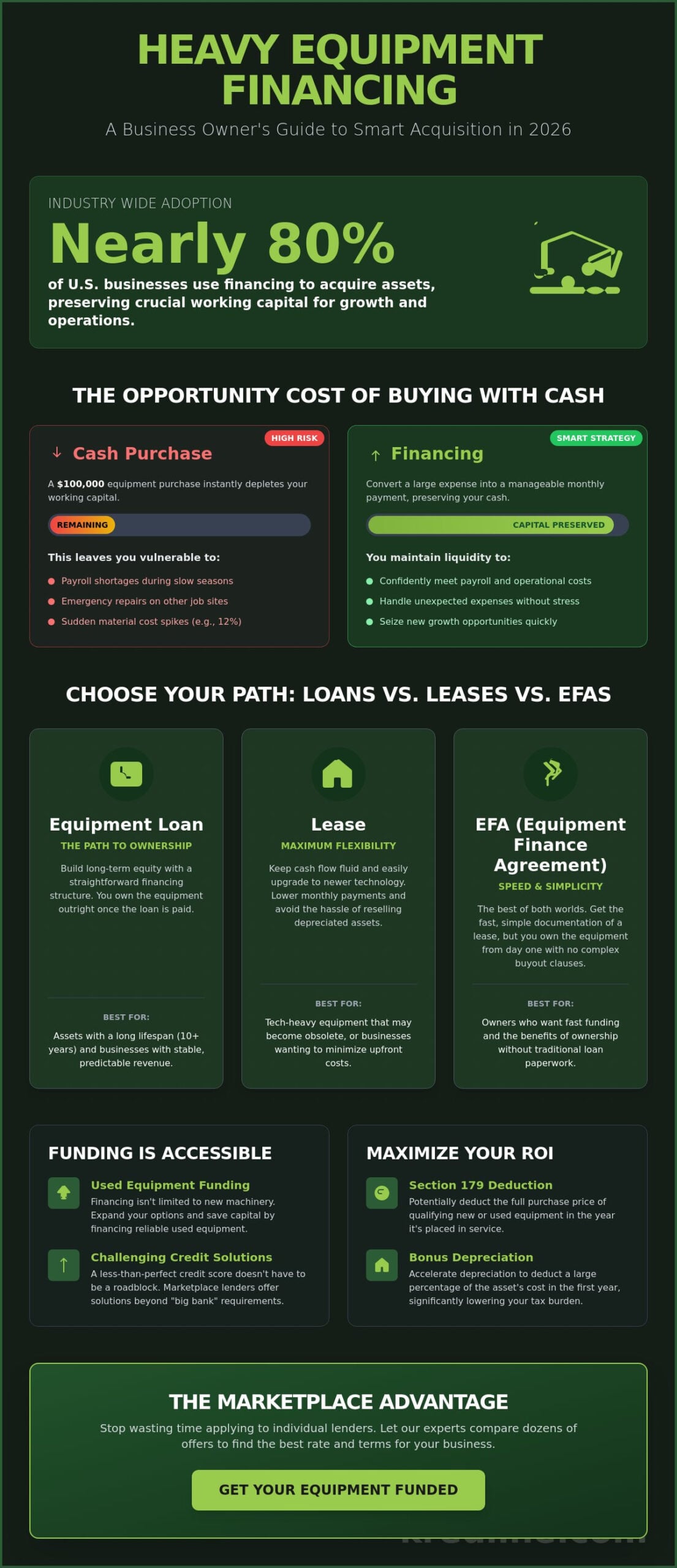

Imagine it’s April 2026. You just secured a project that could define your year, but your current fleet is already at capacity. You need a new backhoe, yet the upfront cost threatens to deplete the working capital you need for payroll. You aren’t alone in this dilemma, as nearly 80% of U.S. businesses now use heavy equipment financing to acquire assets according to recent industry reports. It’s a practical way to keep your operations moving without draining your cash reserves.

You likely know that growth requires big tools, but the thought of a “no” from a traditional bank or high payments during a slow season is daunting. We’re here to help you navigate those concerns. This guide will show you how to secure necessary machinery while protecting your daily cash flow through strategic marketplace options. We’ll break down how to find flexible terms that adapt to your revenue cycles. By the end, you’ll have a clear roadmap to upgrade your fleet without the financial stress that usually comes with a six-figure purchase.

Key Takeaways

- Learn how using machinery as collateral can lower your borrowing costs and simplify the approval process.

- Compare the long-term equity benefits of loans against the cash-flow flexibility offered by equipment leases and EFAs.

- Find out how to secure funding for used equipment even if your credit score isn’t at a “big bank” level.

- Discover how to maximize your 2026 tax deductions using Section 179 and bonus depreciation through heavy equipment financing.

- Understand why a marketplace approach saves you time by letting experts compare multiple lenders on your behalf.

What is Heavy Equipment Financing and Why Does It Matter in 2026?

Running a business in 2026 requires more than just grit; it requires smart capital management. Heavy equipment financing is a specialized financial tool designed to help you acquire large-scale machinery without paying the full price upfront. Whether you need a bulldozer, a CNC machine, or a fleet of delivery trucks, this type of funding allows you to spread the cost over several years. The core mechanic here is that the machinery itself serves as the collateral. This setup reduces the risk for the lender, which often translates into more accessible terms and lower interest rates for you compared to unsecured business loans.

In the current 2026 economic landscape, liquidity is your most valuable asset. Operational costs have shifted, and having cash on hand is vital for navigating unexpected hurdles. When you use heavy equipment financing, you keep your cash reserves intact. You aren’t just acquiring a machine; you’re preserving your ability to stay flexible. If a new project requires a quick pivot or if material costs spike by 12% mid-year, you’ll be glad you didn’t lock all your working capital into a single piece of iron.

The Opportunity Cost of Buying with Cash

Think about the real-world impact of your spending. If you drop $100,000 on a new excavator today, that money is immediately removed from your operational budget. It can’t cover emergency repairs on another job site, and it can’t help you meet payroll during a rainy week. For many construction firms, the “burn rate” during the off-season can reach $20,000 or more per month just to keep the lights on. Having that $100,000 in the bank provides a safety net that a paid-off machine simply cannot offer. Asset-backed lending is a strategic tool that converts your equipment needs into a manageable monthly expense while protecting your total liquidity.

Understanding the 2026 Equipment Market

The machinery you’re looking at today is far more advanced than what was available ten years ago. In 2026, tech integration like telematics and AI-driven diagnostics is standard on most heavy gear. These features make equipment more efficient but also more expensive to purchase outright. Because technology cycles are moving faster, you need funding that matches that pace. You might find that a Finance lease offers the best balance of ownership and tax benefits for your specific situation. Currently, industries like renewable energy, infrastructure logistics, and specialized manufacturing are seeing the highest demand for these equipment funding options. They allow businesses to scale quickly to meet the demands of a high-tech market without the burden of massive initial outlays.

Breaking Down Your Options: Equipment Loans vs. Leases

Choosing between a loan and a lease isn’t just about the monthly payment. It’s about what you want your balance sheet to look like in five years. Heavy equipment financing requires a strategy that matches the lifespan of the machine. If you’re buying a backhoe that will last 15 years, ownership makes sense. If you’re looking at specialized tech that might be obsolete by 2028, a lease is usually the smarter move.

Equipment Loans: The Path to Ownership

Loans are built for stability. You get a fixed interest rate and a clear path to full ownership, which builds long-term equity. For businesses with steady revenue, this is often the most cost-effective route. Sometimes you don’t need a six-figure loan for a new tractor; you might just need a short-term business loan to grab a specialized attachment or handle an unexpected engine overhaul. Many owners also look into SBA financing options like the 504 loan program, which offers long-term, fixed-rate financing for major fixed assets that help a business expand.

An Equipment Finance Agreement (EFA) acts as a middle-ground option. It feels like a lease because the documentation is simple and fast, but you own the equipment from day one. There’s no “fair market value” buyout at the end. You just pay off the balance and keep the machine, making it a favorite for owners who want speed without the complexities of traditional bank structures.

Leasing: Flexibility and Technology Upgrades

Leasing keeps your cash flow fluid. A Fair Market Value (FMV) lease is great for equipment that loses value quickly. You use it for three years and hand it back, avoiding the headache of selling a depreciated asset. If you know you want to keep the machine, a $1 Buyout lease gives you the tax benefits of a lease while ensuring you own the asset for a single dollar at the end of the term. This helps growing firms keep their debt-to-income ratios healthy while still getting the gear they need to finish a job.

When Alternative Funding Fills the Gap

Traditional heavy equipment financing takes time. If a sudden contract win requires an extra excavator next week, Revenue-Based Financing can provide the capital to bridge that growth spurt without waiting for a bank’s committee. For emergency repairs on a job site, a Merchant Cash Advance provides the speed you need to get back to work immediately. These aren’t meant for 10-year asset purchases; they’re tools for speed and flexibility when timing is more critical than the lowest possible APR.

If you’re unsure which path fits your 2026 growth plan, you can prequalify for business funding to see what options are actually on the table for your specific situation.

Overcoming Barriers: Financing for Used Equipment and Challenging Credit

Roughly 45% of small business owners hesitate to apply for funding because they assume their credit score isn’t “bank-ready.” If your score sits in the 600 to 650 range, a traditional big bank will likely decline the application. These institutions often require a 720+ score and years of perfect tax returns. The reality of heavy equipment financing in 2026 is different. Specialized lenders prioritize the machine’s value and your company’s actual cash flow over a single three-digit number. They see the equipment as the primary collateral, which opens doors that remain closed at local branches.

The Strategic Case for Used Equipment

Buying used isn’t just about saving money; it’s a smart depreciation play. A new excavator can lose 20% of its market value the moment it leaves the dealer lot. Used machines have already taken that initial hit, meaning you’re financing an asset that holds its value more steadily. Securing heavy equipment financing for used assets requires a bit more documentation, such as a formal appraisal or a detailed spec sheet to prove the machine’s worth. Most used equipment can be financed for 3 to 5 years, provided the machine isn’t too old. Lenders typically follow a “15-year rule,” meaning the age of the equipment plus the loan term shouldn’t exceed 15 years. Using the Section 179 deduction allows you to write off the full purchase price of used gear in the first year, which significantly boosts your immediate ROI.

Financing with Less-Than-Perfect Credit

A lower credit score doesn’t end the conversation. It just changes the structure of the deal. If your score is below 640, expect to put more skin in the game. A down payment of 20% or 30% can often offset the perceived risk of a lower score. Lenders also look closely at your bank statements. They want to see consistent monthly revenue that proves you can handle the new payment without straining your daily operations. At Kredline, we don’t believe one rejection defines your business. We navigate a network of multiple lenders to find the specific profile that fits your credit history and equipment needs. You can explore your equipment funding options without the stress of a cold corporate rejection. We focus on the strength of your business today, not just a mistake from three years ago.

Maximizing Your ROI: Tax Incentives and Application Prep

Investing in a new excavator or a fleet of trucks is a major move. You aren’t just adding a tool to your yard; you’re adding a significant asset to your balance sheet. To get the best return on investment, you need to look at the tax code. Section 179 is your best friend here. It lets you deduct the full purchase price of qualifying equipment from your gross income in the year you buy it. This applies whether the gear is brand new or used. For 2026, the deduction limit is expected to be around $1.2 million, which covers the needs of most growing companies.

Bonus depreciation is another layer, though it looks different in 2026. Under the current phase-down schedule, bonus depreciation sits at 20% for the 2026 tax year. While this is lower than previous years, it still provides an immediate boost to your cash flow when combined with Section 179. Always sit down with your CPA before you sign the papers. They’ll help you time the purchase to ensure your heavy equipment financing aligns with your specific tax liabilities and revenue cycles.

Beyond taxes, your Profit & Loss (P&L) statement is the heartbeat of your application. Lenders look at this to see if your business is healthy enough to handle a new monthly payment. A clean, up-to-date P&L shows you have a handle on your margins. It proves that the new equipment will generate more income than it costs to finance. If your books are messy, it can lead to delays or higher interest rates. Taking the time to organize your records before applying is the fastest way to secure a competitive rate.

Leveraging Section 179 for Massive Savings

Section 179 isn’t a complex loophole; it’s a straightforward incentive for small businesses. Instead of depreciating a machine over several years, you can often take the entire deduction upfront. This can result in tens of thousands of dollars in tax savings during your first year of ownership. It’s a powerful way to offset the initial costs of heavy equipment financing and keep more cash in your operating account.

The Essential Document Checklist

Lenders move faster when you’re prepared. If you want an approval in 24 to 48 hours, you need your paperwork ready. Gather these items to speed up the process:

- Six months of recent business bank statements.

- A detailed equipment quote from the seller including the serial number and year.

- A valid government-issued ID.

- A clear “Use of Funds” summary explaining how the machine will increase your revenue.

A detailed quote is non-negotiable. Lenders need to know exactly what they’re backing to determine the asset’s value. When you have these documents ready, you show the lender you’re an organized, low-risk partner.

Ready to see what your business qualifies for? You can explore equipment funding options to get started today.

The Marketplace Advantage: How Kredline Simplifies the Search

Most small business owners spend roughly 26 hours searching for credit, according to data from the Federal Reserve. When you are managing a job site or a fleet of vehicles, you don’t have three workdays to waste on paperwork. The biggest hurdle is usually the “single-lender” trap. If you walk into a traditional bank, they can only offer you their specific products. If your credit score or industry doesn’t fit their narrow criteria, you get a rejection and have to start over from scratch.

Kredline operates as a multi-lender marketplace, which fundamentally changes your odds. Instead of you chasing lenders, we bring the options to you. We act as the advisor that does the heavy lifting of shopping rates and terms. This approach is built on the idea that your time is better spent growing your company than acting as your own loan officer. We handle the technical side of heavy equipment financing so you can focus on the actual equipment.

Our process is designed to be human-first. While we use modern technology to speed up approvals, we know that financial decisions are personal. You aren’t just a file number; you’re a business owner trying to meet payroll and expand. We provide the clarity needed to understand how a new monthly payment will impact your bottom line, ensuring the debt helps you grow rather than holding you back.

Why a Broker Beats a Traditional Bank

The main benefit of working with a broker is the “one application, many options” model. You submit your information once, and it reaches a network of lenders who specialize in different niches. This is vital because a lender that understands the HVAC industry might not have the same appetite for a paving company’s risk. Kredline understands these nuances and directs your application to the right desks.

- Industry Expertise: We know which lenders prefer specific types of machinery or specialized vehicles.

- Business Focus: Kredline doesn’t offer personal loans or consumer credit. Every resource we have is dedicated to business growth.

- Efficiency: You avoid the repetitive cycle of filling out identical forms for five different banks.

Getting Started Without the Stress

The path to new machinery shouldn’t feel like a high-stakes interrogation. You can prequalify for business funding to see exactly where your business stands before you make any hard commitments. This step is crucial because it often only requires a soft credit pull. This means you can see your potential rates without seeing a dip in your credit score, which is a common fear for many owners.

Once you see your standing, you can explore equipment funding options that are tailored specifically to your industry’s standards for 2026. Whether you are looking for a lease or a loan, we provide the data you need to make an informed choice. Our goal is to make heavy equipment financing a transparent and manageable part of your business strategy, removing the friction that usually comes with commercial lending.

Build Your Fleet for a Strong 2026

Running a construction or landscaping business means your growth depends on the machines you have on-site. As we look toward 2026, the strategy for heavy equipment financing is about more than just getting a loan. It’s about balancing your immediate cash flow needs with long-term ROI. You’ve seen how Section 179 tax deductions can significantly lower your tax liability by allowing you to deduct the full purchase price of qualifying equipment in the year you buy it. Whether you’re opting for a lease to keep your tech current or a loan to build equity in used machinery, the right choice keeps your operations moving.

You don’t have to navigate these financial hurdles alone. Kredline provides access to a national network of third-party lenders who understand the specific demands of the landscaping and construction industries. This means you get access to specialized knowledge without the stress of traditional bank bureaucracy. You can check your options today through prequalification that won’t impact your personal credit score.

Explore your equipment financing options and prequalify in minutes with Kredline.

Your next project is waiting, and the right tools will help you finish it ahead of schedule.

Frequently Asked Questions

How much of a down payment is required for heavy equipment?

Most lenders require a down payment between 10% and 20% of the total purchase price. If your business has a strong credit history and solid cash flow, you might qualify for 0% down programs. For a $100,000 backhoe, plan to have $10,000 to $20,000 ready. This upfront cost reduces your monthly payments and shows the lender you’re committed to the investment.

Can I finance heavy equipment with a credit score below 650?

You can absolutely get heavy equipment financing with a credit score below 650. Since the machinery acts as collateral, lenders feel more secure than they would with an unsecured loan. You’ll likely see higher interest rates or need a larger down payment to offset the risk. Many specialized lenders focus on your business’s recent revenue rather than just a single credit number.

What is the difference between an equipment loan and an equipment lease?

The main difference is ownership; a loan results in you owning the machine, while a lease is more like a long-term rental. With a loan, you pay the full price plus interest over a set term. Leases often have lower monthly costs and give you the choice to return the gear or buy it for a small fee, like $1, at the end of the term.

Does equipment financing cover used machinery from private sellers?

Financing is available for used machinery from private sellers, though it involves a few extra steps like an independent inspection. Lenders want to ensure the equipment’s value matches the loan amount. Most programs require the machine to be less than 15 years old. Using a platform like Kredline helps you navigate the paperwork needed to verify the seller’s title and the machine’s condition.

How long does it take to get approved for equipment funding?

You’ll typically receive an approval decision for heavy equipment financing within 24 to 48 hours of submitting your application. If you have your last six months of bank statements and equipment quotes ready, some lenders move even faster. After you sign the documents, the funds are usually transferred to the seller within three business days. Speed is vital when you’re trying to bid on a new project.

Are there tax benefits to financing my construction equipment?

Yes, Section 179 of the IRS tax code lets you deduct the full cost of equipment in the first year you use it. For the 2024 tax year, the deduction limit is $1.22 million. This means you don’t have to wait years to write off the depreciation. It’s a powerful way to keep more cash in your business while upgrading your fleet and reducing your overall tax liability.

What happens to the equipment if I can’t make my payments?

If you miss payments, the lender can repossess the equipment because it serves as the collateral for the loan. Usually, lenders reach out to find a solution before taking such drastic steps, often after 90 days of delinquency. If the machine is seized and sold for less than what you owe, you might still be responsible for the balance. It’s always best to talk to your advisor if cash flow gets tight.

Can I finance equipment if I am a startup business?

Startups can finance equipment, but they usually need at least six months of operating history or a down payment of at least 20%. Lenders look at your personal credit score and your industry experience to gauge risk. If you’ve got a signed contract for a new job, that future revenue can help you secure the funding you need to get your operations off the ground.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.