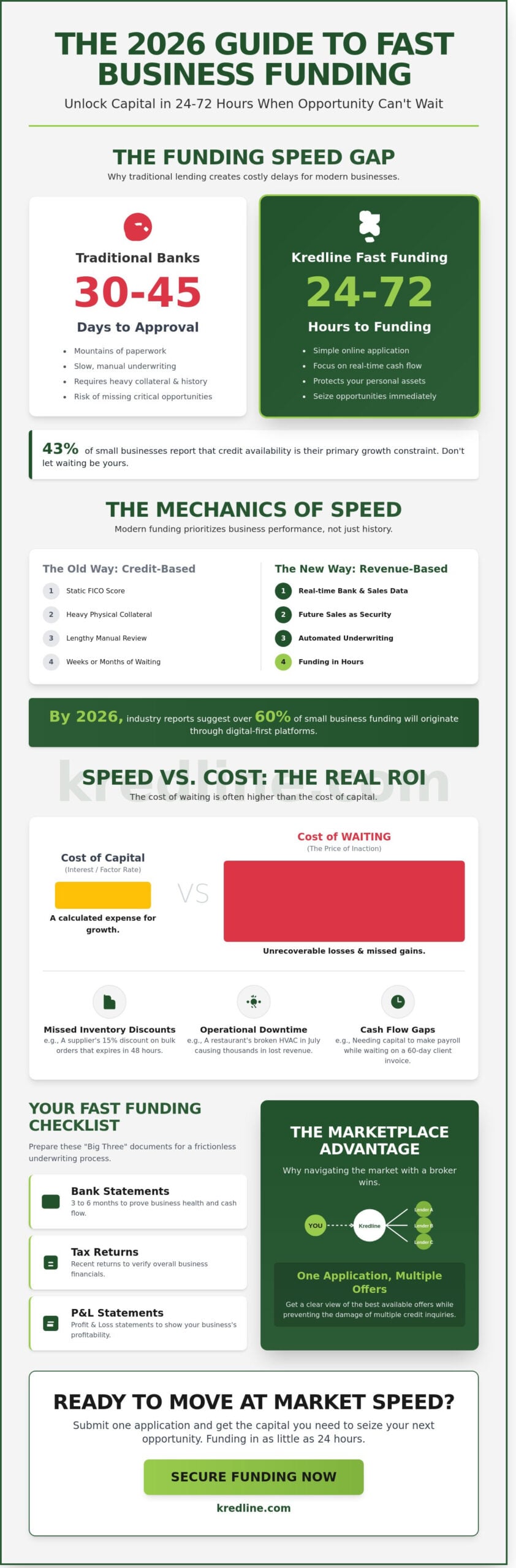

Last Tuesday, a bakery owner in Chicago found a liquidation sale on high-end ovens that would double her production, but she realized a traditional bank’s 30-day approval window meant the deal would be gone by Friday. It’s a common hurdle when 43% of small businesses, according to recent Federal Reserve surveys, report that credit availability remains their primary growth constraint. If you’ve ever watched a seasonal opportunity slip away while waiting for a loan officer to call you back, you’ll understand that timing is often more valuable than the interest rate itself. Securing fast lending loans isn’t about being desperate; it’s about being agile enough to move when the market does.

We agree that the old way of funding, with its mountain of paperwork and weeks of silence, doesn’t fit the pace of a modern company. You deserve a process that respects your schedule and understands that inventory needs don’t wait for committee meetings. This 2026 guide will show you how to access rapid capital without the typical bank delays, focusing on transparent terms and flexible repayment structures. We’re going to walk through the most reliable funding paths available right now and show you how Kredline helps you evaluate which option actually fits your specific business cycle.

Key Takeaways

- Learn how to access capital in as little as 24 to 72 hours by choosing funding models designed for business agility rather than traditional bank bureaucracy.

- Understand the mechanics of fast lending loans, including how revenue-based financing shifts the focus from your credit score to your actual business performance.

- Evaluate the real ROI of your funding by comparing the total cost of capital against the “cost of waiting” for a slow-moving traditional loan.

- Prepare your “Big Three” documents—bank statements, tax returns, and P&Ls—to ensure your application moves through underwriting without unnecessary friction.

- Discover why a marketplace approach prevents the damage of multiple credit inquiries while giving you a clear view of the best available offers.

What Are Fast Lending Loans for Businesses?

Fast lending loans for businesses are defined by their speed; they provide capital that reaches a bank account within 24 to 72 hours. In the 2026 economic environment, where supply chains and digital markets move faster than ever, waiting six weeks for a traditional bank approval can mean a lost opportunity. These products aren’t just emergency money anymore. They represent a specialized segment of the alternative finance market that prioritizes agility over the slow-motion processes of legacy institutions.

You’ll notice a clear trade-off here. Speed requires a different risk assessment model. Because lenders provide funds in days rather than months, interest rates or factor rates are typically higher than a standard 10-year term loan. It is a premium paid for the convenience of bypassing the red tape and extensive paperwork. For most owners, the cost of the capital is secondary to the cost of the missed opportunity if they don’t act quickly.

Business vs. Personal Fast Loans

Mixing personal and business finances is a common trap for new owners. Using a personal credit card or a consumer loan to cover a $30,000 business expense can damage your personal debt-to-income ratio. This makes it harder to buy a home or car later. Business-specific short-term business loans are designed to protect your personal assets. They focus on the company’s revenue and cash flow rather than just your personal FICO score. Documentation is usually minimal, often requiring only three to six months of recent bank statements to prove the business’s health.

When Speed Becomes a Strategic Advantage

Waiting is expensive. If a supplier offers a 15% discount on bulk inventory for an upfront payment, but that offer expires in 48 hours, the cost of fast lending loans is often lower than the savings you’d gain. Speed also protects operations. A restaurant with a broken HVAC system in July can’t wait three weeks for a loan committee to meet; they need a fix before the weekend rush to avoid thousands in lost revenue.

Another common use involves using a Merchant Cash Advance (MCA) to bridge gaps during slow-paying invoice cycles. When a client owes you $50,000 but won’t pay for 60 days, fast lending loans provide the liquidity to meet payroll on Friday. This isn’t about desperation; it’s about maintaining momentum. Kredline helps owners evaluate these options to ensure the funding fits the specific timeline of the business needs without adding unnecessary stress to the balance sheet.

The Mechanics of Speed: MCA and Revenue-Based Financing

Traditional bank underwriting often feels like a relic of the past. While a standard commercial loan can take 30 to 45 days to process, modern alternative lenders have cut that time down to 24 or 48 hours. They don’t just look at a static credit score from three years ago. Instead, they use secure technology and API integrations to analyze your real-time bank data and accounting software. This shift from credit-only models to revenue-based data is why fast lending loans are becoming the standard for businesses that need to move quickly. By 2026, industry reports suggest that over 60 percent of small business funding will originate through these digital-first platforms rather than traditional branches.

Speed happens because these lenders prioritize your current cash flow over heavy physical collateral. In most cases, your future sales act as the security for the capital. By linking directly to your business bank account, lenders can verify your daily or monthly income instantly. This allows for automated repayments that happen in small increments, which protects your cash flow from the shock of a large monthly bill. While SBA-backed loans remain a solid benchmark for long-term, low-interest debt, they rarely match the velocity required for an emergency repair or a flash inventory purchase that expires in 72 hours.

Merchant Cash Advances (MCA) Explained

A merchant cash advance isn’t technically a loan. It’s a purchase of your future credit card sales at a discount. If your restaurant has a busy Friday night, the repayment amount is slightly higher because it’s a fixed percentage of that day’s batch. If you have a slow Tuesday, the amount drops. This flexibility is a lifesaver for retail and hospitality businesses where transaction volume changes by the hour. Many owners turn to these fast lending loans because they don’t require the months of paperwork or personal real estate liens typical of a local credit union.

Revenue-Based Financing for Steady Growth

For service-based companies or tech firms that don’t rely on credit card swipes, revenue-based financing offers a similar level of agility. Unlike traditional debt that requires fixed monthly payments regardless of performance, this model uses a “remittance” based on your total gross monthly income. If your revenue dips by 15 percent, your payment typically scales down with it, ensuring you can still meet payroll. It’s a partnership approach that ensures the funding supports your growth rather than stifling it during a seasonal lull. If you’re wondering which structure fits your current numbers, you can prequalify for business funding to see your options without a hard credit pull.

Speed vs. Cost: Evaluating the Real ROI of Fast Funding

Small business owners often fixate on the interest rate. It’s a natural reaction. However, looking only at the Annual Percentage Rate (APR) doesn’t tell the whole story when you’re using fast lending loans to bridge a gap. Traditional bank loans or SBA products might offer lower rates, but they often take 60 to 90 days to fund. In a fast-moving market, three months of waiting can be the difference between winning a contract and watching a competitor take it. You have to weigh the premium you pay for speed against the revenue you lose by standing still.

Understanding Factor Rates

A factor rate is a decimal multiplier applied to the principal. Unlike traditional interest, it’s fixed from day one. You can calculate your total repayment by multiplying the loan amount by the factor. For example, a $10,000 loan with a 1.2 factor means you’ll pay back $12,000. It’s vital to remember that these rates don’t decrease if you pay early. You’re committing to the total cost of capital upfront, which provides clarity but lacks the flexibility of a declining balance loan. This structure is common in the world of fast lending loans because it allows lenders to take on higher risks while providing capital within 24 to 48 hours.

Analyzing the Opportunity Cost

The “cost of waiting” is a real line item on your balance sheet. Imagine a retailer gets a one-time offer to buy $100,000 of inventory for $50,000. This inventory will sell for full price within 30 days, netting a $50,000 profit. A traditional bank might offer a 7% interest rate, but the approval takes six weeks. By then, the inventory is gone. If you use fast capital with a higher cost but 24-hour funding, the premium you pay is simply a business expense to secure that $50,000 gain. This is where speed becomes a strategic tool rather than just a convenience. Using these short-term wins responsibly also helps build the credit profile needed to eventually qualify for a more flexible business line of credit.

Before signing any agreement, look for these specific red flags that indicate predatory lending:

- Confusing Fee Structures: If a lender can’t give you a clear total repayment amount in writing, walk away.

- Double Dipping: Some lenders charge additional fees to “renew” a loan before the first one is paid off.

- Aggressive Daily Payments: While daily or weekly draws are common, ensure they won’t choke your daily operating cash flow.

Reliable partners like Kredline focus on making these numbers clear from the start. The goal isn’t just to get cash in your account, but to ensure the funding actually helps your business grow without creating a debt trap. When the return on the investment exceeds the cost of the capital, the loan has done its job.

How to Secure Fast Business Funding: A 2026 Preparation Checklist

Speed isn’t just about the lender’s technology; it’s about your readiness. If you want a decision in hours rather than weeks, you need your financial house in order before hitting submit. When applying for fast lending loans, the goal is to move through automated underwriting without triggering a manual “red flag” that requires a human loan officer to step in and slow things down.

The core of your application relies on the “Big Three” documents. You’ll need your last 4 to 6 months of business bank statements, your most recent two years of federal tax returns, and a current year-to-date Profit and Loss (P&L) statement. In 2026, lenders use sophisticated algorithms to scan these files for cash flow consistency. If your P&L is more than 30 days old, it’s often considered outdated by modern standards. You should also check for existing Uniform Commercial Code (UCC) filings. These are public notices lenders file to announce their interest in your assets. If a previous lender didn’t clear a lien after you paid off a loan, it can stall your new application for several days while you scramble to provide proof of payoff.

Documentation You Need Ready Right Now

Lenders expect the last 4 to 6 months of bank statements in digital PDF format. Don’t use screenshots or cell phone photos; these usually trigger manual reviews, adding 24 to 48 hours to the process. You’ll also need a valid government ID and a voided business check to verify your identity. Most modern lenders use digital document portals that allow you to link your bank account directly. This is the fastest way to verify your revenue and can often lead to a same-day approval because it eliminates the need for manual data entry.

Optimizing Your Profile for Instant Approval

Your bank account history is the primary factor in determining speed. Avoid Non-Sufficient Funds (NSF) flags at all costs. Data shows that even one or two NSF instances in a 90-day period can lead to an automatic decline or a significant reduction in the offer amount. Your industry also impacts the speed of fast lending loans. For example, a retail shop with daily transactions often sees faster approvals than a heavy construction firm because the revenue is easier to predict. Taking a prequalification check is the best first step to see where you stand without a hard credit pull.

Having a clear “use of funds” statement is equally vital. Instead of asking for general capital, specify that you’re “purchasing $25,000 in seasonal inventory” or “covering payroll during a 14-day gap between contracts.” This transparency builds trust and helps the lender’s risk model categorize your request correctly. When the lender understands exactly where the money is going, they can move much faster on the final sign-off.

If you’re ready to see what your business qualifies for, you can explore your funding options today.

The Broker Advantage: Why Navigating the Marketplace Wins

Many business owners believe that applying to as many lenders as possible increases their chances of success. This strategy, often called “shotgunning,” usually does more harm than good. Each time a lender performs a hard credit pull, your credit score can drop by 5 to 10 points. If you apply to five lenders in a week, you’ve potentially damaged your credit before you’ve even seen an offer. Underwriters at major institutions often view multiple recent inquiries as a sign of financial distress. This can lead to higher interest rates or outright rejections.

A marketplace approach eliminates this risk. Instead of multiple hits to your credit, you provide information once. We then match your profile against a curated network of lenders who actually want to work with businesses in your specific situation. It’s a process built on precision rather than volume. Kredline prioritizes transparency, ensuring you understand the logic behind every offer. We focus on human-first financial guidance because we know that a spreadsheet doesn’t tell your whole story. Our advisors act as navigators, matching your industry’s unique risks and rewards to the right capital source.

One Application, Multiple Solutions

Kredline connects you to a diverse network of third-party providers through a single point of contact. We don’t just look for any loan; we filter for terms that align with your cash flow patterns. If your business sees heavy seasonal swings, we find lenders who offer flexible repayment structures. For businesses needing to upgrade machinery or vehicles, specialized equipment funding is often a smarter path. These targeted options can be processed 30% faster than general loans because the equipment serves as collateral, simplifying the underwriting process for fast lending loans.

Your Partner in Growth

We view funding as a long-term strategy rather than a one-time transaction. A single loan might solve a problem today, but a partnership helps you plan for next year. Fast funding often serves as a vital bridge. For example, if you’re waiting 60 to 90 days for a larger SBA 7(a) working capital loan to fund, a shorter-term option can cover immediate payroll or inventory needs. This prevents your momentum from stalling while you wait on government-backed paperwork. Our goal is to help you move from urgent needs to sustainable growth. Take the next step in your business journey and consult with a Kredline advisor today to explore your fast lending loans and long-term options.

Take the Next Step Toward Your Business Goals

Finding the right capital doesn’t have to be a source of stress. By 2026, the speed of your response to market shifts will likely define your success. You’ve seen how revenue-based financing and MCAs offer immediate relief for payroll or inventory gaps, even if that capital costs more than a traditional bank loan. Success comes down to your preparation. Following a clear checklist ensures you’re ready when an opportunity appears.

Navigating the marketplace for fast lending loans is easier when you aren’t doing it alone. You need a partner who looks past the algorithms to find terms that actually fit your cash flow. We provide access to a diverse network of top-tier third-party lenders and offer expert guidance from real people who understand your daily operations. There’s no hype here; we focus on transparent terms designed to help you move forward. You’ve worked hard to build your business, and having a reliable navigator makes all the difference.

See your funding options and prequalify in minutes

Your next growth phase is within reach.

Frequently Asked Questions

How fast can I actually receive funds after applying?

You’ll typically see funds in your bank account within 24 to 72 hours after your application is approved. Many online lenders now process digital applications in under 15 minutes and can wire the capital on the same business day if you finish the paperwork before their 10:00 AM cutoff. This speed is designed to help you handle immediate needs like an emergency repair or a limited-time inventory discount.

Do fast lending loans require a hard credit pull?

Most providers of fast lending loans use a soft credit pull to give you an initial offer, which won’t impact your credit score at all. A hard pull usually only happens once you’ve reviewed the terms and decided to move forward with the final funding contract. Recent industry data shows that 85% of alternative lenders prioritize your recent bank statements and cash flow over your historical FICO score during the initial review phase.

What is the minimum credit score for fast business funding?

You generally need a minimum credit score of 500 to 600 to qualify for most fast funding options. While traditional banks often require a 680 or higher, modern lenders focus more on whether your company generates at least $10,000 in monthly revenue. If your business is healthy but your personal score is lower, you can use Kredline to explore options that weigh your daily sales more heavily than your credit history.

Can I get fast funding if I already have an existing business loan?

Yes, you can often secure additional capital even if you’re currently paying off another loan. Lenders call this a “second position” or an “add-on” loan, and they’ll look at your remaining debt-to-income ratio to ensure your cash flow can handle another payment. If your revenue has increased by at least 20% since you took out your first loan, you’re in a strong position to qualify for more growth capital.

Are there any restrictions on how I use the fast loan capital?

There are almost no restrictions on how you use the capital from fast lending loans. Whether you need to cover payroll for 12 employees during a seasonal dip or buy $8,000 worth of raw materials for a new contract, the choice is yours. Unlike specific equipment financing or real estate mortgages, this type of funding provides the flexibility to address whatever bottleneck is currently slowing your business down.

How do repayments work for merchant cash advances?

Repayments for a merchant cash advance happen automatically through a fixed percentage of your daily credit card sales or a set daily draw from your bank account. This means if you have a slow Tuesday with zero sales, you don’t pay anything for that day, or the amount is significantly lower. It’s a dynamic system that ensures your debt payments stay in sync with your actual business performance each week.

Is fast lending available for startups with less than 6 months of history?

Most lenders require at least 3 to 6 months of active business history and consistent bank deposits to approve an application. If your startup is less than 90 days old, you’ll likely need a high personal credit score or significant collateral to secure a loan. Once you hit that 180-day mark, your options expand significantly because you’ve proven your business model can generate steady revenue.

What is the difference between a factor rate and an interest rate?

A factor rate is a fixed multiplier applied to your total loan amount, while an interest rate accrues over time on the remaining balance. For example, a 1.2 factor rate on a $10,000 loan means you’ll owe exactly $12,000, no matter how quickly you pay it back. It’s a very transparent way to see the total cost of fast lending loans upfront without worrying about compounding interest or hidden monthly fees.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.