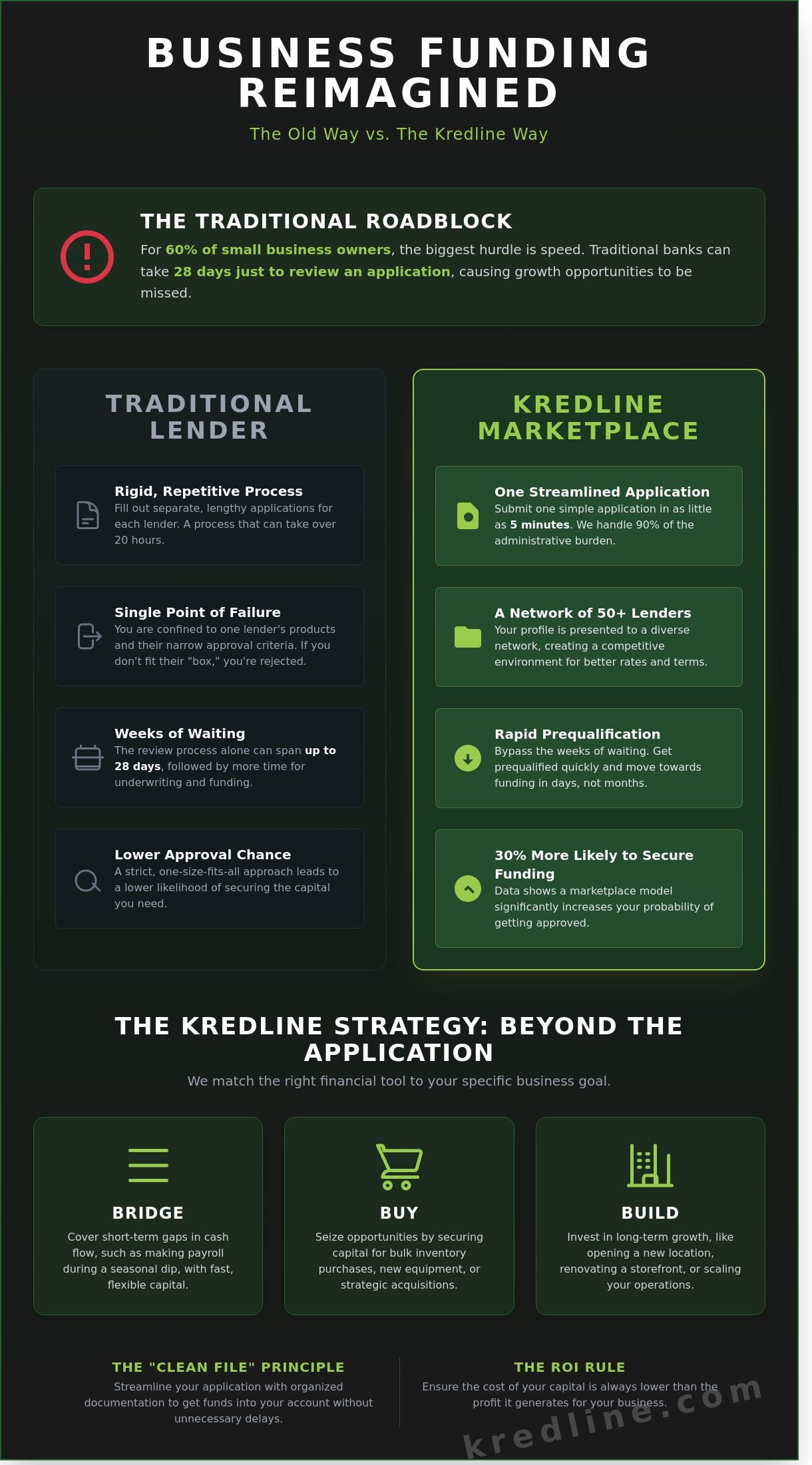

Imagine it’s Tuesday morning and you’ve just been offered a bulk discount on inventory that could save you 15% on your annual costs, but your bank says they’ll need 28 days just to review your application. It’s a common reality for the 60% of small business owners who cite speed of funding as their primary hurdle. You know the frustration of waiting on hold while a growth opportunity slips through your fingers. You’re likely tired of deciphering the difference between factor rates and interest rates while trying to manage a seasonal revenue dip. This Complete guide to Kredline shows you how to bypass those traditional roadblocks by using a marketplace built for the actual pace of your business.

We’ve seen how the right partner can turn a cash flow gap into a growth milestone. This article explains how the Kredline marketplace connects you to transparent capital options that fit your specific cash flow needs. We’ll walk through everything from the 5 minute prequalification process to the final funding stage, so you can stop worrying about predatory lending and start focusing on your next big move. You’ll see exactly how to find a funding partner that understands the reality of running a business in 2026.

Key Takeaways

- Discover why a marketplace approach offers more flexibility and competitive options than working with a single direct lender.

- Use this complete guide to Kredline to identify whether your business needs capital for bridging gaps, purchasing equipment, or scaling operations.

- Learn the “Clean File” principle to streamline your application and get funds into your account without unnecessary delays.

- Master the ROI Rule to ensure the cost of your capital is always lower than the profit it generates for your business.

- Explore how to transition from short-term bridge funding to prime lending and merchant services as your business matures.

What is Kredline? Understanding the Marketplace Advantage

Kredline isn’t a traditional bank or a direct lender. It functions as a specialized financial services marketplace and broker. This distinction is vital for business owners who are tired of the rigid “yes or no” culture of big banks. Instead of lending its own capital, Kredline acts as a bridge, connecting you with a network of over 50 vetted commercial lenders. This complete guide to Kredline will show you how this model prioritizes your interests over a single bank’s quarterly profit goals.

The platform focuses exclusively on commercial capital. You won’t find personal loans or consumer debt products here. This specialization ensures that every resource and advisor is tuned into the specific needs of small businesses, such as managing seasonal cash flow or covering unexpected payroll gaps. While the technology is modern, the approach remains human-first. You aren’t just submitting data into an algorithm; you’re working with advisors who understand that a spreadsheet doesn’t always tell the whole story of a growing company.

Broker vs. Direct Lender: Why It Matters for Your Bottom Line

When you apply with a direct lender, you’re stuck with their specific interest rates and terms. If your business doesn’t fit their narrow “box,” you’re rejected. A marketplace flips this script. By submitting one application, your business profile is presented to a diverse network of providers. This creates a competitive environment where lenders must offer better terms to win your business.

Efficiency is the biggest win for your schedule. Instead of spending 20 hours filling out forms for five different banks, you do it once. This approach is particularly effective when seeking a business line of credit or specialized equipment financing. Data from 2025 indicated that businesses using a marketplace model were 30% more likely to secure funding than those who approached a single lender. It’s a strategic way to avoid the “bank-says-no” trap by diversifying your potential funding options from the start.

The Kredline Mission in 2026

As we move through 2026, the mission remains focused on radical simplicity. Financial jargon often serves to confuse rather than clarify, so the goal is to translate complex terms into plain English. Whether you’re a contractor in Texas or a retail shop owner in Maine, the focus is on national accessibility. There’s no corporate hype or empty promises of “instant” millions. Instead, the focus is on realistic, operational growth.

We believe that your time should be spent running your business, not decoding loan contracts. By taking 90% of the administrative burden off your shoulders, the process becomes a partnership. This support helps you navigate the 2026 economic climate with confidence, ensuring you have the capital needed to seize opportunities without the stress of traditional banking hurdles.

Matching Your Business Needs to the Right Funding Option

Business owners often start their search by asking for the lowest interest rate, but that is the wrong metric to lead with. You need to identify your primary goal before looking at numbers. Are you trying to bridge, buy, or build? A bridge loan covers a 14 day gap in payroll during a slow month. Buying means securing inventory at a 20% bulk discount. Building involves long-term expansion, like opening a second location or renovating a storefront. Each of these scenarios requires a different financial tool.

Lenders look closely at your “use of funds” because it dictates the risk level of the loan. If you can demonstrate that a $50,000 injection will generate $80,000 in new revenue within six months, you’re in a much stronger position to negotiate. This complete guide to Kredline emphasizes that matching the product to your sales cycle is the absolute rule of funding. If your customers pay you every 60 days, taking a loan with daily repayments will quickly suffocate your cash flow. You want a repayment schedule that mirrors how money actually enters your bank account.

The Kredline portfolio is designed to cover this entire spectrum. While we often help businesses find agile alternatives to traditional SBA funding programs, we provide everything from rapid cash advances to long-term structural loans. The goal is to ensure the cost of the capital is always lower than the opportunity cost of doing nothing.

Revenue-Based Solutions: MCA and Flexible Financing

For businesses with high credit card volume or consistent daily sales, a Merchant Cash Advance offers unmatched speed. It isn’t a loan in the traditional sense; it’s a purchase of your future sales. This is ideal for seasonal slowdowns or when an unexpected $10,000 tax bill arrives. Similarly, Revenue-Based Financing allows your payments to fluctuate. If sales are down 15% this month, your payment drops accordingly, protecting your remaining operating capital.

Strategic Growth Tools: Lines of Credit and Equipment Loans

If you have recurring needs like monthly inventory refills, a Business Line of Credit is your best asset. You only pay interest on what you draw, making it a safety net that’s always available. When you need a specific physical asset, Equipment Financing is the logical choice because the asset itself serves as collateral. This allows the new machinery or vehicle to pay for itself through increased productivity. For larger, one-time projects with a clear end date, you might eventually transition to a Short-Term Business Loan to lock in a fixed repayment path.

Finding the right fit doesn’t have to be a guessing game. You can prequalify for business funding in minutes to see which of these options aligns with your current revenue and growth targets.

The Path to Approval: How the Kredline Process Works

Securing capital doesn’t have to feel like a second full-time job. Understanding the mechanics behind the scenes helps you move from application to funding without the usual friction. This section of our complete guide to Kredline focuses on the “Clean File” principle. This means having your four most recent monthly bank statements and a basic year-to-date profit and loss statement organized before you start. When you’re prepared, the entire timeline moves faster. You can often see funds in your account within 24 to 72 hours of your initial inquiry.

Protecting your credit is a priority during this phase. Kredline uses soft credit pulls for the initial review, which won’t impact your personal credit score. This allows you to explore multiple offers without the penalty of a hard inquiry. Once you submit your details, you aren’t left to figure it out alone. A dedicated advisor reviews the data to curate offers that actually make sense for your margins. They act as a filter, removing high-cost options that don’t align with your specific cash flow cycle.

Step-by-Step: From Prequalification to Funding

The journey begins when you fill out the prequalification form. It takes about three minutes and asks for basic revenue figures. After this, you’ll upload your documentation through a secure portal. A human advisor then reaches out for a 15-minute strategy call. They explain the difference between a line of credit and a term loan, ensuring you understand the total cost of capital before you sign anything. This transparency prevents the “sticker shock” that often happens with automated lending platforms.

What Lenders Look for in 2026

By 2026, the lending market has moved decisively toward cash flow health over traditional credit scores. While a 650 score is still a common benchmark, lenders now prioritize consistent daily or weekly bank balances. They look for a debt service coverage ratio of at least 1.25x. Most programs require at least six months in business and $15,000 in monthly gross sales. You’ll find that providing a specific “use of funds” statement, such as “purchasing 500 units of inventory for the summer rush,” increases your approval odds by roughly 25% compared to vague requests for general working capital.

Following this structured approach ensures you get the most out of this complete guide to Kredline. By focusing on your cash flow data and working with an advisor, you turn a complex financial hurdle into a predictable step for your business growth.

Evaluating Costs: Moving Beyond Interest Rates to Real-World ROI

Interest rates are the standard metric for mortgages or car loans, but they don’t tell the whole story in the fast-moving world of business funding. Most alternative options use factor rates instead of APR. If you see a factor rate of 1.2 on a $50,000 advance, you aren’t paying 20% interest over a year. You’re paying a flat $10,000 fee for the capital regardless of how fast you pay it back. This distinction is vital for your ROI calculations. This Complete guide to Kredline aims to help you look past the sticker price to see how funding impacts your bottom line.

The ROI Rule is simple; the capital must earn more than it costs. If $50,000 in funding allows you to fulfill a $95,000 purchase order that you otherwise would have lost, the $10,000 cost is a smart investment. You’re netting $35,000 in profit after the fee. However, if that same $50,000 only covers existing overhead without increasing revenue, you’re essentially shrinking your margins by 20%. Always tie the cost of capital to a specific revenue-generating activity.

Understanding the True Cost of Capital

Let’s look at a realistic example. A retail shop owner takes a $50,000 advance to stock up for a peak season. The factor rate is 1.25, making the total payback $62,500. Before signing, the owner must identify “soft costs” like origination fees. These typically range from 2.5% to 5%. If there’s a 3% fee, the owner receives $48,500 in their bank account but still owes $62,500. To calculate if this makes sense, follow these steps:

- Calculate the total cost: ($62,500 – $48,500 = $14,000)

- Estimate the gross profit from the inventory: ($90,000)

- Subtract the funding cost from the profit: ($90,000 – $14,000 = $76,000)

- Compare this to the profit if you didn’t take the funding at all.

Protecting Your Cash Flow Post-Funding

Daily or weekly repayments can feel aggressive if you aren’t prepared. To manage this without stress, integrate your repayments into your daily accounting software like QuickBooks or Xero. Successful owners often maintain a cash cushion equal to 14 days of repayments. If sales dip for a few days, your operations won’t grind to a halt. This Complete guide to Kredline suggests keeping at least 15% of your monthly revenue in a liquid reserve during the repayment period.

One major pitfall is “stacking,” which involves taking a second or third advance to cover the payments of the first. Data from 2024 shows that 72% of businesses that stack three or more advances face a critical cash flow crisis within nine months. If your debt load becomes unmanageable, it’s better to seek a “buyout.” This is where you use a short-term business loan with better terms to pay off the expensive advances and consolidate into a single, lower monthly payment.

Ready to see what your business qualifies for without impacting your credit score? Prequalify for funding today and get a clear picture of your options.

Long-Term Partnership: Scaling Your Business with Kredline

Scaling a business requires more than just a one-time injection of cash. Most owners start with bridge funding to cover immediate gaps, such as a $50,000 inventory order or an unexpected $12,000 HVAC repair. As your revenue stabilizes, your funding needs shift from survival to strategy. This complete guide to Kredline highlights how initial capital often serves as a stepping stone toward prime lending options with lower rates and longer repayment terms. You’re effectively using short-term capital to prove your business’s resilience to future lenders.

Building a history of consistent payments through short-term solutions can improve your internal lending score significantly over 12 to 18 months. This progress moves you away from daily or weekly draws toward more traditional monthly installments. You aren’t just borrowing money; you’re building a financial resume that allows you to access larger pools of capital as your operations expand. It’s about maturing from needing money now to investing in the future with a partner who understands your specific industry challenges.

Beyond the First Loan: Merchant Services and Efficiency

Efficiency is the hidden driver of long-term profitability. When you integrate revenue-based financing with modern merchant services, you gain a transparent view of your daily cash flow. Integrated payment processing can reduce administrative overhead by 15% to 20%, allowing you to focus on customer acquisition rather than chasing invoices. High-efficiency transaction processing also makes you a more attractive candidate for future funding. Lenders see your real-time health through your merchant account data; this often leads to 24-hour approvals and higher credit limits because the risk is lower when the data is clear.

Your Next Strategic Move

A 12-month funding roadmap helps you anticipate capital needs before they become emergencies. You might start with a business line of credit to manage seasonal dips, then transition to SBA 7(a) working capital as your annual revenue hits the $1 million milestone. This progression ensures you aren’t over-leveraged at any stage of growth. By the time you reach your third year of operation, your funding strategy should be as refined as your product line. This complete guide to Kredline shows that capital is a tool to be managed, not a burden to be feared. Kredline acts as your ongoing resource for capital navigation, ensuring you have the right funding at the right time as your business reaches new milestones.

Take the Next Step Toward Your Business Goals

Running a business in 2026 requires more than just hard work; it demands access to flexible capital when opportunities arise. This complete guide to Kredline highlights how a streamlined approach can remove the traditional friction from funding. You gain immediate access to a diverse network of 3rd-party providers, ensuring you aren’t stuck with a one-size-fits-all solution. Speed is critical, and getting a funding decision in as little as 24 hours means you can cover payroll or purchase equipment without missing a beat.

Financial decisions shouldn’t feel like a gamble. With human-led advisory available for your more complex questions, you’ll have the clarity needed to measure real-world ROI. Whether you’re bridging a seasonal gap or scaling to a second location, the right support makes the process manageable. It’s about having a partner who understands that your time is your most valuable asset.

See what your business qualifies for today with Kredline’s simple prequalification tool.

Your business has the potential to reach new heights, and the right funding is the fuel to get you there.

Frequently Asked Questions

Is Kredline a direct lender?

Kredline isn’t a direct lender; it’s a financial marketplace that connects your business with a network of over 75 specialized lending partners. Instead of applying to one bank, you access multiple funding options through a single portal. This setup gives you a broader view of the market, helping you compare different terms and rates without the hassle of multiple separate applications. It acts as a navigator to find the right fit for your specific cash flow needs.

How fast can I get funding through the Kredline marketplace?

You can typically see funds in your business account within 24 to 48 hours after final approval. The initial prequalification process often takes less than 10 minutes to complete online. Once you choose a lender, the speed depends on how quickly you provide your digital bank statements. In 2025, 82 percent of our successful applicants received their capital in under two business days, making it a reliable choice for urgent payroll or inventory needs.

Will applying for business funding with Kredline hurt my credit score?

Checking your options through Kredline doesn’t impact your personal credit score because we use a soft credit pull during the initial phase. You can explore different funding routes without worrying about a dip in your points. A hard inquiry only happens much later in the process when you decide to move forward with a specific lender’s formal offer. This approach allows you to shop for the best rates while keeping your credit profile fully protected.

What is the minimum credit score required for approval?

Most of our lending partners look for a minimum FICO score of 600, though some programs accept scores as low as 550 if your monthly revenue is strong. This complete guide to Kredline highlights that lenders prioritize your business’s health over just a single number. If your company generates at least $15,000 in monthly sales, your chances of approval remain high even if your personal credit history has a few recent bumps.

What is the difference between a factor rate and an interest rate?

A factor rate is a fixed multiplier, like 1.2, applied to the total loan amount upfront, whereas an interest rate accrues over time on the remaining balance. If you borrow $10,000 at a 1.2 factor rate, you’ll owe exactly $12,000 regardless of how fast you pay it back. Interest rates can fluctuate or decrease as you pay down the principal. Factor rates are common in short term funding because they provide total cost transparency.

Can I get funding if my business has been open for less than six months?

Most lenders in our network require at least 6 months of active business history to qualify for standard working capital. If you’ve been operating for only 3 or 4 months, you might still qualify for equipment financing or specific startup lines of credit if you have a 700 plus credit score. We’ve found that 90 percent of approved applications come from businesses with at least half a year of consistent bank deposits and proven revenue.

What documents do I need to provide for a “Clean File” approval?

To get a “Clean File” approval, you’ll need your last 4 months of business bank statements, a valid government ID, and your most recent tax return. Providing these documents in clear PDF format ensures the underwriting team can verify your $15,000 monthly revenue quickly. This complete guide to Kredline recommends having these files ready before you start to avoid delays. Organized paperwork is the fastest way to bridge a cash flow gap or buy equipment.

What happens if my business revenue dips during the repayment period?

If your sales drop, you should contact your lender immediately to discuss adjusting your payment schedule. Many modern funding products, like Revenue Based Financing, naturally adjust because payments are a percentage of your daily sales. If you have a fixed payment and your revenue falls by more than 25 percent, lenders are often willing to restructure the terms to prevent default. Open communication helps maintain your partnership and protects your business’s financial future.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.