A daily withdrawal from your business account sounds like a cash flow nightmare, but for many high-velocity companies, it’s actually the most predictable way to manage debt. If your sales happen every day, a large lump-sum payment at the end of the month can feel like a massive hurdle that doesn’t reflect how you actually earn money. You’ve likely experienced the frustration of traditional lenders who don’t understand the rhythm of a retail or service business. This is where daily payment business loans come into play, offering a way to access capital without the rigid monthly structures of a standard bank.

We’ll show you how these structures work and how to tell if they’re a tool for growth or an unnecessary burden. You’ll learn the critical differences between fixed payments and variable remittances, especially since five states now require APR-equivalent disclosures as of May 2026. We’ll also cover how to determine if your sales velocity supports this high-frequency funding. Kredline is here to help you weigh these options so you can find a path that keeps your operations running smoothly without the stress of traditional bank delays.

Key Takeaways

- Learn how automated withdrawals align your repayment schedule with the daily rhythm of your sales to prevent large, end-of-month payment shocks.

- Understand the functional differences between daily payment business loans and merchant cash advances to choose the structure that best fits your revenue stability.

- Identify how “factor rates” work and learn to translate these figures into a clear picture of your total borrowing costs.

- Discover how to accurately calculate your daily free cash flow so you can secure funding without overextending your operating budget.

- Find out how comparing multiple transparent offers side-by-side helps you avoid the risks of debt stacking and high-interest cycles.

What Are Daily Payment Business Loans and Why Do They Exist?

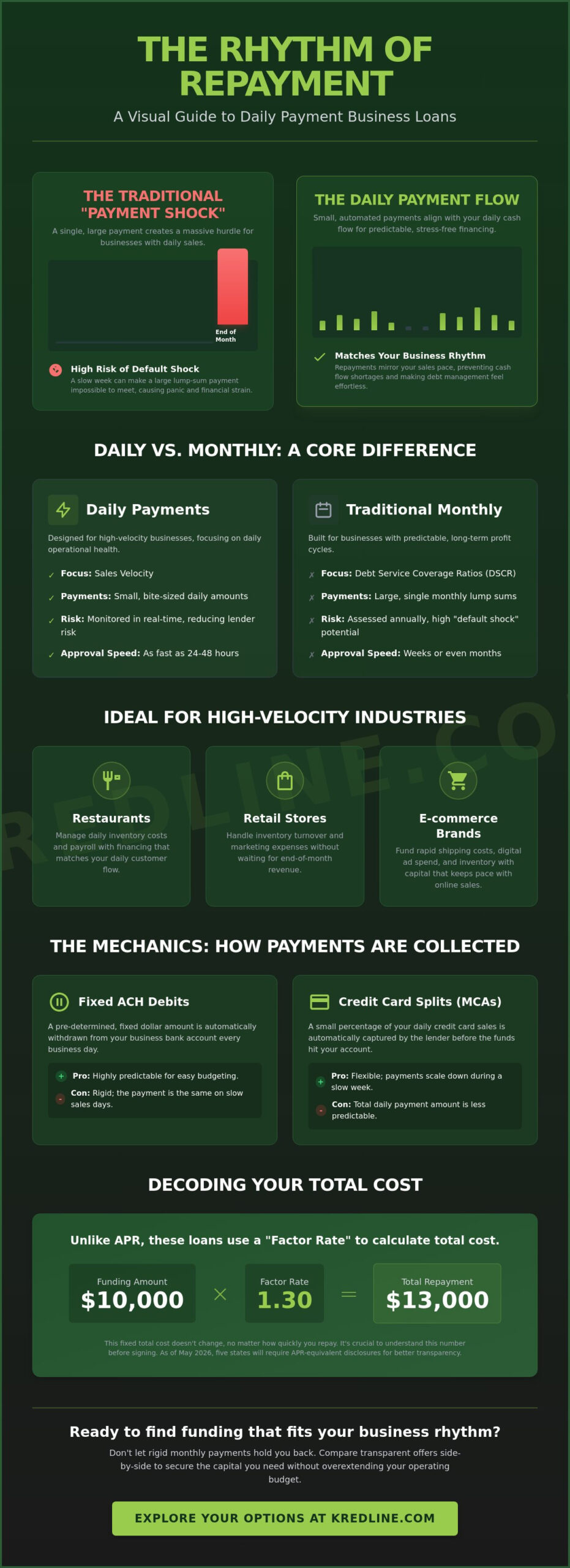

Most business owners are used to the monthly grind. You wait for the first of the month, write a big check, and hope your bank balance stays in the black. Daily payment business loans flip this script. These are financing products where a small amount is automatically withdrawn from your account every business day, typically Monday through Friday. It’s a high-frequency approach designed to mirror the actual pace of your sales. Instead of one massive hurdle at the end of the month, you handle small, bite-sized payments that keep your debt from piling up.

Traditional banking is getting tighter. With the SBA now requiring 100% U.S. citizenship for loans as of March 1, 2026, many entrepreneurs are looking elsewhere for capital. When the prime rate sits around 6.75%, the speed and accessibility of alternative finance become more attractive than the slow, rigid requirements of a traditional bank. Alternative lenders prefer this daily structure because it reduces “default shock.” This is the panic that sets in when a business realizes they don’t have $5,000 ready for a single monthly payment. Taking $200 a day feels manageable and gives the lender real-time data on your business health.

This model works best for businesses with constant foot traffic or high transaction volumes. If you’re processing credit card sales daily, your cash flow is already “high-velocity,” making these loans a natural fit. Common industries that benefit include:

- Restaurants: Where daily cash flow is the lifeblood of the kitchen.

- Retail stores: Dealing with inventory turnover and daily customer visits.

- E-commerce brands: Managing rapid shipping costs and digital ad spend.

The Core Difference Between Daily and Monthly Payments

Monthly payments are built on Debt Service Coverage Ratios (DSCR). Banks look at your annual profit and decide if you can survive twelve big hits a year. Daily payments focus on velocity. It’s about daily bank balances rather than long-term projections. For many, these micro-payments feel less “heavy.” It’s easier to budget for a small daily deduction than to worry about a massive lump sum that might coincide with a slow week or an unexpected repair bill. If you’re unsure which path fits your current revenue, exploring a short-term business loan through Kredline can help you see how these structures impact your bottom line.

Why Lenders Require Daily Remittances

Lenders insist on daily access primarily for risk mitigation. When a lender has direct access via ACH or credit card processing, they don’t have to wait 30 days to see if you’re struggling. This structure is closely related to the Merchant Cash Advance (MCA) model, where the repayment is tied directly to your sales volume. Because the risk is monitored daily, these lenders can often approve funding in 24 to 48 hours. They aren’t waiting for a committee; they’re looking at your real-time ledger to provide the capital you need to keep moving.

The Mechanics: How Daily Payments Are Collected

Once you’ve secured one of these daily payment business loans, the manual work on your end effectively stops. The system is built on automation. Lenders don’t want you to remember to log in and pay; they want the process to be as friction-free as possible. They achieve this by linking directly to your business bank account or your credit card processor. This connection allows them to see your daily activity and ensure the agreed-upon amount is transferred without delay.

Timing is another detail to watch. Payments typically only happen on business days, which means your cash flow gets a breather on weekends and federal holidays. If Monday is a bank holiday, the next withdrawal usually happens on Tuesday. This predictable rhythm helps you plan for payroll or inventory orders without worrying about a surprise debit on a Saturday morning. The way the money leaves your business depends on the specific agreement you sign, generally falling into one of two categories.

ACH Debits vs. Credit Card Splits

ACH (Automated Clearing House) debits pull a fixed dollar amount from your bank account every morning. This is predictable but rigid; the payment stays the same regardless of your sales. Conversely, split funding takes a percentage of your daily credit card sales before they hit your account. This method offers more flexibility during a slow week, as the payment amount scales down with your revenue. This is a key feature of a Merchant Cash Advance (MCA).

Understanding Factor Rates and Terms

Factor rates, usually between 1.1 and 1.5, determine your total payback by multiplying the principal by the rate. A factor rate represents the fixed cost of the advance rather than an interest charge that grows the longer you hold the debt. Most daily payment business loans carry terms ranging from 3 to 18 months. Knowing the total cost upfront prevents the “interest creep” common in traditional credit lines. If you want to see how these numbers look for your specific situation, you can prequalify for business funding to get a clear breakdown of potential terms.

Understanding the total cost of capital is where many owners get tripped up. While the factor rate is fixed, the effective APR can be high because you’re paying the money back so quickly. As of May 2026, five states, including California and New York, require lenders to provide APR-equivalent disclosures. This is a win for transparency. It allows you to compare a daily payment loan to a traditional bank loan more accurately. Even if the daily amount feels small, knowing the annual cost helps you decide if the speed of funding is worth the price.

Daily Fixed Payments vs. Merchant Cash Advances (MCA)

It’s easy to assume all daily payment business loans are identical since the money leaves your account every morning. However, there’s a significant legal and practical divide between a fixed-payment loan and a Merchant Cash Advance (MCA). A loan is a debt you’re legally obligated to repay regardless of your performance. An advance is technically a purchase of a portion of your future sales. While both provide immediate liquidity, they handle a slow sales day very differently.

The regulatory landscape is also shifting. Because MCAs are commercial contracts rather than traditional loans, they haven’t always been subject to the same usury laws. This is why the 2026 disclosure requirements in states like California and New York are so vital. They force a level of transparency that helps you see the true cost of an advance compared to a fixed-term loan. Choosing the right one depends on whether your daily revenue is a steady stream or a fluctuating tide.

Merchant Cash Advances: The Revenue-Linked Option

An MCA is often the better fit for businesses with fluctuating daily revenue, like a seasonal boutique or a restaurant. Since the lender takes a percentage of your daily credit card sales, the payment naturally shrinks if you have a slow Tuesday. If the lender’s automated pull takes more than your agreed percentage during a slump, you can trigger a “reconciliation.” This process adjusts the withdrawal to match your actual sales volume, ensuring the funding doesn’t suffocate your operating cash. It’s a flexible safety net that fixed-payment structures simply don’t offer.

Daily Fixed-Payment Loans: Predictability Over Flexibility

If your business sees steady, predictable income, a short-term business loan with a fixed daily payment might be more attractive. This is common for B2B companies that have consistent daily bank balances from ongoing contracts. You know exactly what’s leaving your account at 9:00 AM every morning, which makes long-term budgeting simpler. The risk, of course, is that the payment stays the same even if you hit an unexpected slump. There is no reconciliation here; the debt must be serviced regardless of that day’s sales figures.

Deciding between these two requires an honest look at your ledger. A fixed daily payment business loan offers the peace of mind of a clear end date and a set cost. An MCA offers the flexibility to survive a volatile market. Kredline acts as a navigator in this process, helping you compare these structures side-by-side so you aren’t surprised by how the money leaves your account when things get quiet.

Is a Daily Payment Loan Right for Your Business?

Before you commit to daily payment business loans, you need to look at your “Daily Free Cash Flow.” This isn’t your total revenue; it’s the cash left over after you’ve paid your staff, your rent, and your suppliers. A safe rule of thumb is to ensure the daily withdrawal doesn’t exceed 10% to 15% of your average daily gross sales. If your shop brings in $2,000 on a typical Tuesday, a $250 payment might be manageable, but a $500 payment is likely to cause a crisis during a slow week.

You must also avoid the trap of “stacking.” This happens when a business owner takes out a second or third daily payment loan while the first is still active. It’s a quick way to suffocate your operations. Most reputable lenders will actually refuse to fund you if they see another daily debit already hitting your account because the risk of a cash flow collapse is too high. Funding only makes sense if it’s “ROI-positive.” If a supplier offers a 20% discount for buying $50,000 of inventory in bulk, the savings might far outweigh the cost of the financing. In that scenario, the loan is a tool for profit, not just a survival tactic.

If you aren’t sure if your margins can handle a daily debit, it’s worth taking a moment to prequalify for business funding to see what your actual daily numbers would look like. This helps you plan without any guesswork.

Ideal Use Cases: Bridging Gaps and Pursuing Growth

Daily payment structures excel when the money is used to solve an immediate, revenue-generating problem. If a bakery’s main oven breaks, every hour of downtime is lost profit. An emergency repair funded by a quick daily loan gets the business back to full capacity within 48 hours. Similarly, preparing for a peak season by hiring extra staff or stocking up on popular items can be a smart move, provided the increased sales volume will cover the debt quickly. The goal is to use the capital to create more value than the cost of the repayment.

Setting a Safety Buffer in Your Business Account

Maintaining a “cushion” in your bank account is non-negotiable with daily payments. If an automated pull hits and your balance is too low, you’ll face Non-Sufficient Funds (NSF) fees from your bank, which often cost $35 or more per occurrence. Over a week, those fees can add up faster than the loan interest itself. If a daily pull feels too aggressive for your rhythm, don’t be afraid to negotiate a weekly payment structure instead. This provides a bit more breathing room to accumulate cash while still keeping the lender happy with frequent remittances. Always evaluate your net profit margins to ensure they can absorb this daily “tax” without putting your payroll at risk.

Navigating Your Funding Options with Kredline

Finding the right capital shouldn’t feel like a high-stakes guessing game. When you’re considering daily payment business loans, the most effective way to protect your margins is to see multiple offers side-by-side. Going directly to a single lender limits your perspective. You only see their specific criteria and pricing. Kredline functions as a marketplace, which means you get a bird’s-eye view of the current market without having to fill out a dozen different applications. It’s about finding the structure that fits your sales velocity, not just the first one that says yes.

Transparency is the foundation of a healthy lending relationship. With the 2026 shifts in disclosure laws across states like California, New York, and Utah, borrowers now have more power to see the true cost of their capital. We help you cut through the marketing noise to understand the actual impact on your daily bank balance. To get started, the process is straightforward. You typically only need to provide three to six months of recent business bank statements. This allows for a clear assessment of your cash flow and ensures the daily payment amount is sustainable for your specific operation.

The Role of a Navigator in Securing Favorable Terms

Think of Kredline as a navigator in a complex market. We filter out predatory lenders to focus on sustainable daily structures that won’t cripple your business. Sometimes, the best way to handle a daily debit is to customize the term length. By extending a term from six months to twelve months, you can significantly lower the “daily hit” to your account. This flexibility is often lost when dealing with a single direct lender who has rigid, pre-set products. We work to ensure the funding supports your growth rather than just filling a temporary gap.

How to Prequalify Without Impacting Your Credit

One of the biggest concerns for business owners is the fear of a credit score drop. Exploring your options with Kredline involves a soft credit pull, which means you can see your potential offers without hurting your score. The process is built for speed; you can often move from a simple application to a firm offer in less than 24 hours. This allows you to make decisions based on real numbers rather than estimates. If you’re ready to see what’s available for your business, you can prequalify for business funding today and take the first step toward more predictable cash flow.

Aligning Your Funding with Your Business Rhythm

Managing cash flow isn’t about avoiding debt; it’s about finding the right structure for your specific revenue cycle. By now, you understand that daily payment business loans work best when they mirror your high-velocity sales. Whether you choose a fixed ACH debit or a flexible merchant cash advance, the goal is to keep your operations moving without the “default shock” of a massive monthly bill. With new transparency laws in five states as of May 2026, you’re better equipped than ever to compare the true cost of capital and protect your margins.

Kredline simplifies this search by connecting you to a network of 50+ third-party lenders. You can access funding in as little as 24 hours, and most advances don’t require personal collateral. This speed allows you to act on bulk inventory discounts or urgent repairs before they impact your bottom line. Explore your daily payment funding options with Kredline and find a solution that matches the pace of your success. Your business moves fast, and your financing should be able to keep up.

Frequently Asked Questions

Will a daily payment loan affect my personal credit score?

Most prequalifications through Kredline use a soft credit pull, which doesn’t lower your score. A hard pull typically only occurs once you’ve reviewed your offers and decided to move forward with a specific lender. This allows you to explore daily payment business loans without worrying about a sudden drop in your personal credit rating during the research phase.

Can I pay off a daily payment business loan early to save on costs?

Paying off a factor-rate loan early doesn’t always save you money because the cost is fixed from the start. Unlike a traditional interest-bearing loan where interest accrues over time, a factor rate is a set fee. Some lenders might offer a small discount for early repayment, but you should check your contract for “prepayment penalties” before assuming you’ll save on total costs.

What happens if my business has a slow day and I can’t make the daily payment?

If you have a Merchant Cash Advance, you can request a reconciliation to lower your payment during a slump. If you have a fixed-payment loan, the withdrawal happens regardless of your sales. Missing a payment can trigger NSF fees of $35 or more from your bank; it’s vital to maintain a cash buffer in your account to avoid these extra charges.

Are daily payment loans more expensive than traditional bank loans?

Yes, these loans are generally more expensive, with APRs often ranging from 15% to 50% compared to bank rates of 7% to 13% in 2026. You’re paying for speed and accessibility. These products are designed for short-term needs where the return on investment happens quickly, rather than long-term debt that you carry for several years.

What is the difference between a daily payment and a weekly payment?

The main difference is how the debt affects your daily operating cash. A daily payment is pulled every business day, while a weekly payment happens once every seven days. Weekly structures are often better for businesses that don’t have high daily transaction volumes, such as wholesalers or B2B contractors who wait for larger invoices to be settled.

Do daily payment loans require collateral like my home or equipment?

Most of these funding options are unsecured, meaning you don’t have to pledge your home or specific equipment as collateral. However, lenders will almost always file a UCC-1 lien against your business assets. This gives them a legal claim to your business property if the debt isn’t repaid, but it avoids the risk of losing personal real estate.

How do I calculate the daily payment amount from a factor rate?

Multiply your principal by the factor rate and divide that total by the number of business days in the term. For example, a $10,000 advance with a 1.2 factor rate over 6 months (roughly 126 business days) results in a total payback of $12,000. Dividing $12,000 by 126 days gives you a daily payment of approximately $95.24.

Is a Merchant Cash Advance considered a daily payment loan?

Technically no, a Merchant Cash Advance is a purchase of future receivables rather than a loan. While it’s often categorized under daily payment business loans because of how the money is collected, the legal distinction is important. This difference is why MCAs can offer flexible “split funding” that adjusts to your sales volume, whereas a true loan has a rigid schedule.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.