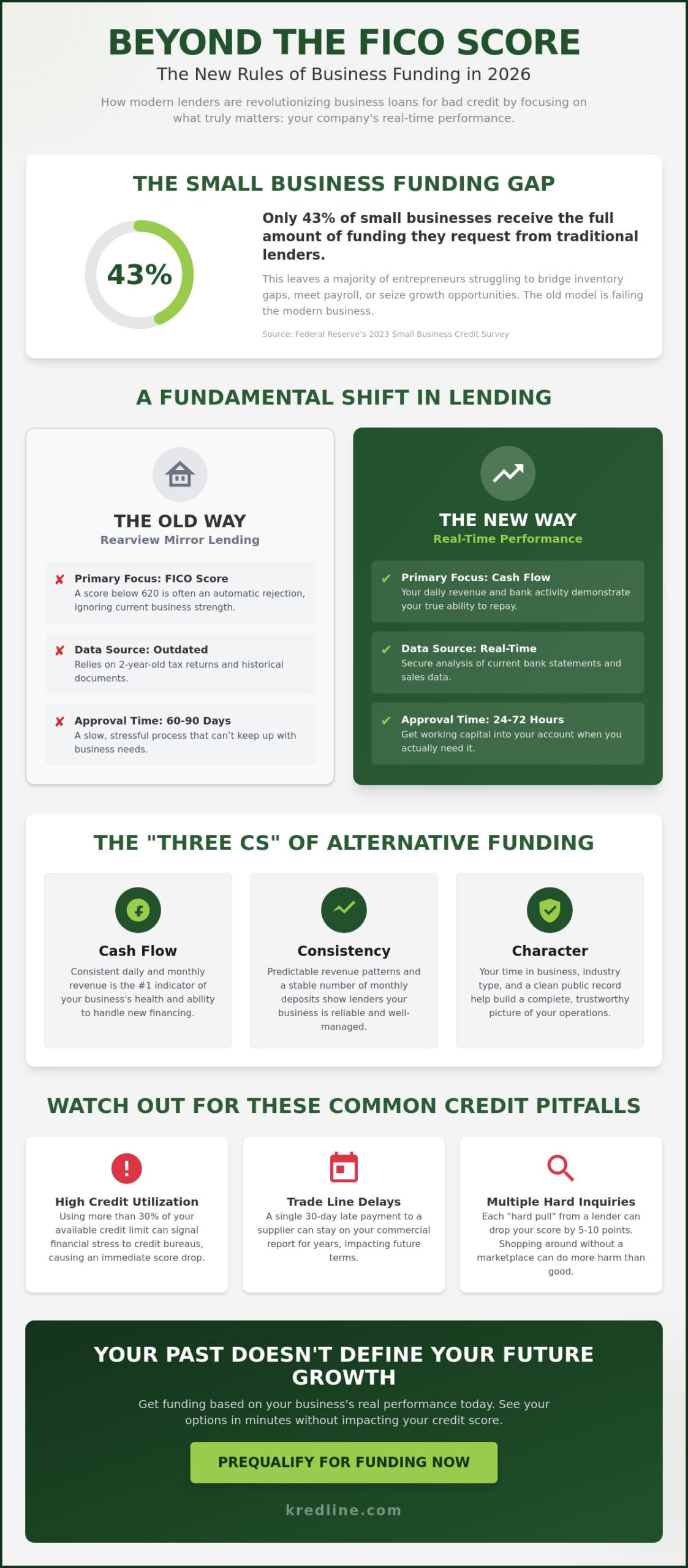

A low credit score isn’t a death sentence for your company; it’s often just a sign that your business has outpaced its traditional paperwork. According to the Federal Reserve’s 2023 Small Business Credit Survey, only 43% of firms received the full amount of funding they requested, leaving thousands of owners searching for alternative business loans for bad credit. You’ve likely felt the sting of an automated rejection letter or the frustration of a lender who treats you like a risk rather than a partner. It’s exhausting to face high-pressure sales tactics when you just need to bridge an inventory gap or meet a Friday payroll.

We believe that your past financial hurdles shouldn’t block your future growth. This guide shows you how to secure the capital you need to thrive, even when traditional bank requirements feel out of reach. You’ll learn how to distinguish transparent funding from predatory traps and find a path to better financial standing through successful repayment. We’ll examine the specific lending criteria for 2026, the real differences between loans and cash advances, and how to get working capital into your account without the stress of a typical bank application.

Key Takeaways

- Learn why modern lenders prioritize your business’s daily revenue and cash flow over traditional FICO scores in the 2026 landscape.

- Discover how to secure business loans for bad credit by matching the right financial tool to your specific growth or operational challenges.

- Understand the “Three Cs” of alternative funding to help you build a compelling revenue narrative that lenders actually trust.

- Compare short-term loans and lines of credit to identify which option best bridges your current capital gaps without adding unnecessary stress.

- Explore why a marketplace approach provides a stronger advocate for your business than applying to a single traditional bank.

Understanding the Reality of Business Loans for Bad Credit in 2026

In 2026, a credit score below 620 is often labeled as “bad” by traditional institutions. This three-digit number can feel like a heavy weight, especially when you’re trying to grow a company that has strong daily sales but a bumpy financial history. Traditional banks still rely on rigid FICO models that were built for a different era. These models often fail small businesses because they don’t account for the speed of modern commerce or the unique challenges of entrepreneurship. When a bank sees a low score, they see a risk. They don’t see the 15% year-over-year growth you’ve achieved or the loyal customer base you’ve built.

The lending landscape has changed significantly. The rise of data-driven underwriting means that your “score” is no longer the only thing that matters. Through Alternative Funding, lenders now use secure technology to analyze your real-time bank activity and revenue patterns. This shift allows for more flexibility. It means that business loans for bad credit are now based on what your business is doing today, rather than a mistake you made three years ago. At Kredline, we believe that a credit dip is often just a timing issue, not a reflection of your ability to run a successful company.

You aren’t alone in this struggle. Many owners find themselves with bruised credit because they prioritized their business over their personal finances. Maybe you used a personal card to cover a $10,000 equipment repair or delayed a payment to keep your team on the payroll during a slow month. These aren’t failures; they’re the tough decisions that keep a business alive. Understanding this reality is the first step toward finding the right partner to help you move forward.

The Difference Between Personal and Business Credit

Most lenders start by looking at your personal credit score. It’s their way of gauging how you handle debt personally. However, in the commercial world, the FICO SBSS score plays a massive role. This score ranges from 0 to 300 and is used to pre-screen many SBA loan applications. While your personal score gets you through the door, your business credit history is what determines your long-term borrowing power. Separating these two profiles is essential for scaling. If you’re ready to see what’s available for your specific situation, you can prequalify for business funding to get a clearer picture of your options.

Common Reasons for Credit Score Dips

Credit scores are sensitive to the daily rhythms of running a business. Common causes for a sudden drop include:

- High Utilization: Using more than 30% of your available credit limit during a seasonal slowdown can trigger an immediate drop in your score.

- Trade Line Delays: A single 30-day late payment to a major supplier can stay on your commercial report for years, affecting your terms with other vendors.

- Credit Pulls: A credit pull is a formal inquiry by a lender to review your credit report, which typically results in a temporary decrease of 5 to 10 points.

Managing these factors requires constant attention, but a temporary dip doesn’t have to stop your progress. Modern funding solutions are designed to bridge these gaps so you can focus on your next big move.

Beyond the FICO Score: How Alternative Funding Actually Works

Traditional banks often feel like they are looking through a rearview mirror. They focus on where your business was two years ago, obsessing over tax returns and personal credit scores. Alternative lenders take a different approach. They prioritize your current performance and real-time cash flow. By using secure API connections to your bank accounts and accounting software, these lenders see the actual health of your operations today. This data-driven model is the engine behind modern business loans for bad credit, allowing for approvals based on consistent revenue rather than just a three-digit score.

Speed is the most visible difference in this sector. While a standard bank application might take 60 to 90 days to process, alternative funding can land in your account within 24 to 72 hours. This isn’t because the lenders are reckless. It’s because their technology analyzes thousands of data points in seconds. While SBA-guaranteed loans provide excellent long-term rates for those who qualify, the rigorous documentation and credit requirements often leave growing businesses looking for faster, more accessible paths.

There is a common misconception that “alternative” means “unregulated.” In reality, reputable lenders in this space operate with high levels of transparency. Many adhere to strict state disclosure laws, such as those in New York and California, which require clear breakdowns of total funding costs. This shift toward transparency ensures you know exactly what you are paying before you sign anything.

Revenue-Based Financing: The Modern Solution

Revenue-based financing is built for businesses that have steady sales but lack heavy assets like real estate or expensive machinery. Instead of a fixed monthly payment that stays the same regardless of your performance, your payments fluctuate based on your sales volume. If you have a slow week, your payment decreases. If you have a record-breaking month, you pay back the capital faster. This flexibility is vital for industries with high transaction counts, such as e-commerce or seasonal retail, where cash flow can be unpredictable.

The Mechanics of a Merchant Cash Advance (MCA)

A merchant cash advance isn’t technically a loan. It’s the purchase of a portion of your future sales at a discount. Because it’s a commercial transaction rather than a traditional debt product, it is often the most accessible form of business loans for bad credit. Instead of an interest rate, you’ll see a “factor rate.” For example, a factor rate of 1.2 on a $10,000 advance means you will pay back $12,000 through a small percentage of your daily credit card receipts or bank deposits.

- Fast Access: Approvals often happen the same day you apply.

- No Fixed Term: The “term” lasts until the purchased sales amount is collected.

- Credit Flexibility: Lenders care more about your daily deposit consistency than a bankruptcy from five years ago.

If you’re tired of being judged solely by a credit report, you can see which funding options fit your current revenue without a hard credit pull. Understanding these mechanics helps you choose a partner that supports your growth rather than one that just checks a box.

Comparing Your Funding Options: Which One Fits Your Problem?

Choosing the right financial tool is about matching the solution to the specific hurdle your business faces. Not all business loans for bad credit are built the same way. Some are designed to be a quick patch for a leaking pipe, while others act as the foundation for a new warehouse. When your credit score is in a recovery phase, your priority shifts from finding the lowest possible rate to finding the highest possible return on investment.

Short-term loans and lines of credit are the two most common paths. A short-term loan gives you a lump sum upfront, which is perfect for a one-off purchase with a clear cost. A line of credit offers a revolving balance you can tap into as needed. For many owners, a short-term loan is easier to secure because lenders prioritize your recent bank statements and daily revenue over a credit report from three years ago. According to the 2023 Small Business Credit Survey, only 43% of firms received the full amount of financing they sought, often due to credit challenges. This makes selecting the right product vital for approval.

Transparency is the most important part of this conversation. We don’t hide the fact that capital costs more when your credit is sub-600. You’ll likely see higher factor rates or shorter repayment terms. The goal isn’t just to get “cheap” money; it’s to secure the capital that allows you to fulfill a contract or fix a machine that generates $5,000 in daily profit. If the loan costs $1,000 but enables $10,000 in new revenue, the math works in your favor.

Solving Immediate Cash Flow Gaps

Cash flow gaps can happen to the healthiest businesses. You might use a short-term business loan to handle emergency equipment repairs that would otherwise halt production. These loans are also effective for bridging the 30 or 60-day gap between sending an invoice and receiving payment. It ensures you can meet payroll during a seasonal dip without stress. At Kredline, we focus on how your business is performing today, helping you find business loans for bad credit that keep your momentum steady when timing is tight.

Investing in Growth and Infrastructure

Growth requires physical assets, and equipment funding is a strategic way to get them. Since the asset itself serves as collateral, lenders feel more secure, which often opens doors that traditional term loans might close. You can also research SBA-guaranteed loan programs to see if your business qualifies for government-backed support. These funds can help you expand to a second location or buy inventory in bulk to capture a 10% supplier discount. Using asset-based funding preserves your liquid cash for daily operations while your new equipment starts paying for itself.

How to Qualify for Financing When Your Credit is Less Than Perfect

Securing capital doesn’t always require a 750 FICO score. In 2026, alternative lenders have shifted their focus toward real-time performance rather than historical mistakes. They use the “Three Cs” to evaluate your file: Cash flow, Character, and Consistency. Cash flow is the most critical factor; it proves your business generates enough liquidity to handle repayments. Character is measured by your time in business and your history with previous creditors. Consistency ensures your revenue isn’t a series of wild swings, but a steady stream that can support a new debt obligation.

When you apply for business loans for bad credit, your bank statements tell a story. Lenders look for a “revenue narrative” that shows you’re using your income to grow, not just to survive. If your statements show consistent monthly deposits from diverse sources, you’re a much stronger candidate. You’ll want to avoid the “stacking” trap at all costs. Stacking occurs when a business takes out multiple high-cost loans simultaneously. This practice creates a debt spiral that is a major red flag for underwriters, as it suggests your cash flow is already stretched to its breaking point.

The Application Checklist for Bad Credit

Preparation is the difference between an approval and a rejection. You don’t need a mountain of paperwork, but you do need the right documents ready to go. Most alternative lenders will require the following items to start the process:

- 3 to 6 months of business bank statements: These must be official PDF downloads, not screenshots or Excel exports.

- A valid business tax ID and legal structure: You must be registered as an LLC, S-Corp, or similar entity to move beyond personal lending products.

- Minimum time in business: Most lenders look for at least 6 months of active operations, though 12 months often unlocks better rates.

Improving Your Approval Odds

You can influence a lender’s decision by cleaning up your accounts before you hit submit. The most important metric is your “Non-Sufficient Funds” (NSF) count. Even one or two NSFs in a 90-day period can lead to an automatic decline because they signal a lack of cash management. Aim for zero NSFs to show you’re in total control of your overhead.

Maintaining a consistent daily balance threshold is another way to build trust. Lenders don’t like to see accounts that drop to near-zero every Friday after payroll. Your average daily balance acts as a primary indicator of your business’s financial health, determining the maximum daily or weekly payment a lender will offer you. By keeping a modest cushion in your account, you demonstrate that your business can absorb unexpected costs without failing to meet its loan obligations.

Ready to see what your business qualifies for based on your current revenue? Prequalify for funding today and get a clear picture of your options without a hard credit pull.

Navigating the Funding Marketplace: Why a Broker is Your Best Bet

Walking into a local bank with a sub-600 credit score often feels like a dead end. Traditional lenders usually rely on rigid, automated systems that trigger an immediate rejection the moment they see a low score. This is where a marketplace model changes the dynamic. Instead of gambling your time on a single institution, you leverage a network of providers who look beyond just the credit report. Kredline acts as your advocate in this space, ensuring you aren’t just another file in a stack, but a business owner with a viable plan.

Transparency is the most critical factor when you’re looking for business loans for bad credit. Some lenders might try to hide high origination fees or aggressive daily payment structures in the fine print. A broker’s job is to pull those details into the light. By comparing multiple offers side-by-side, you can see the true cost of capital and avoid “junk fees” that eat into your margins. This clarity allows you to treat the funding as a strategic tool rather than a desperate measure.

The long-term goal isn’t just to survive the current month; it’s to fix the underlying credit issue. Using current funding to bridge a gap or buy equipment is the first step. As you make consistent, on-time payments, you’re actively rebuilding your profile. Many business owners find that after 12 months of disciplined repayment on a short-term business loan, their credit score improves enough to qualify for even better rates in the future.

The Advantage of Multiple Underwriting Standards

One lender’s “no” is often another lender’s “yes.” This happens because every provider has a different “sweet spot” for risk. While one company might shy away from a restaurant with seasonal dips, another might specialize in restaurant working capital and understand those cycles perfectly. Kredline matches your specific industry and cash flow patterns to the right provider. You submit a single application, which saves hours of manual paperwork and protects your credit score from the damage of multiple hard inquiries.

Next Steps to Secure Your Funding

Getting started is designed to be low-impact and efficient. The prequalification process is fast, usually taking only a few minutes, and it won’t affect your credit score. This gives you a “ballpark” view of what you qualify for without any commitment. Once the offers come in, you don’t have to figure them out alone. You can review the terms with a knowledgeable advisor who explains the math in plain English.

- Review your cash flow: Ensure the daily or weekly payment fits comfortably within your typical revenue.

- Check the total payback: Know exactly what the loan costs from day one to the final payment.

- Plan your growth: Use the funds for high-ROI activities like inventory or marketing to maximize the impact.

Ready to see your options? Prequalify for business funding today and find out how much your business can access to fuel its 2026 growth goals.

Secure Your Future Beyond the Credit Score

Navigating the landscape of business loans for bad credit in 2026 requires looking past traditional bank rejections. You’ve seen that modern funding focuses on your actual performance, specifically your daily revenue, rather than just a historical FICO number. By prioritizing cash flow and leveraging alternative options like revenue-based financing, you can bridge gaps or fund growth without the typical red tape. It’s about finding the right fit for your specific operational needs, whether that’s inventory for a busy season or new equipment to scale.

Success often comes down to who you have in your corner. Instead of applying blindly, you can lean on a partner who offers a human-first advisory approach and a network of 3rd-party providers. Kredline specializes in navigating these complex markets, focusing on Revenue-Based Financing and MCAs to find terms that actually work for your business. You don’t have to handle the stress of the funding marketplace alone. Our team works to simplify the process so you can stay focused on your daily operations.

Explore your funding options and prequalify with Kredline today. Your business has potential that a credit report can’t capture, and we’re here to help you unlock it.

Frequently Asked Questions

Can I really get a business loan with a 500 credit score?

Yes, you can secure funding even with a 500 credit score by looking toward alternative lenders who prioritize your business performance over personal history. While traditional banks typically require a score of 680 or higher, 2026 data shows that 35% of non-bank lenders now use real-time bank data to approve applications. You’ll generally need to show at least $10,000 in monthly revenue to qualify for these specific programs.

How long does it take to get funded with bad credit?

You can typically receive funds within 24 to 48 hours after your application is approved. Speed is the primary advantage of alternative financing because these lenders use automated underwriting systems to assess risk quickly. In 2026, roughly 60% of fintech platforms offer same-day funding if you submit your digital bank statements before noon. This makes it a reliable way to cover immediate payroll or urgent equipment repairs without the long wait.

Will applying for a bad credit business loan hurt my score further?

Most preliminary applications won’t affect your credit score because lenders perform a soft credit pull to check your eligibility. A hard inquiry, which can lower your score by 5 points according to FICO data, usually only happens once you accept a formal offer. Kredline helps you compare options without triggering multiple hard hits, keeping your credit profile protected while you shop for business loans for bad credit.

What is the difference between an MCA and a business loan?

A Merchant Cash Advance (MCA) is a purchase of your future sales, while a business loan is a fixed amount of capital you repay with interest. MCAs don’t have a fixed term and instead take a percentage of daily sales, which helps during slow weeks. Recent industry reports indicate that 42% of small businesses choose MCAs for their flexibility, even though the total cost can be higher than a standard term loan.

Do I need to provide collateral if I have poor credit?

You don’t always need physical collateral like real estate or equipment, as many bad credit options are unsecured. Instead, lenders often require a personal guarantee or a general lien on business assets to mitigate their risk. Statistics from 2025 show that 70% of alternative small business loans are secured by cash flow rather than physical property. This allows business owners who rent their space to still access necessary growth capital.

How much can I borrow if my business has strong revenue but bad credit?

Most lenders will offer between 10% and 15% of your annual gross revenue, regardless of your personal credit score. If your business generates $500,000 a year, you could qualify for $50,000 to $75,000 in funding. Lenders focus on your consistent deposits and average daily balances to ensure you can handle the daily or weekly repayments without straining your operations or cash flow.

Are there specific industries that find it easier to get bad credit funding?

High-volume, cash-heavy industries like restaurants, retail stores, and construction companies often find it easier to secure business loans for bad credit. These sectors provide the consistent daily revenue that alternative lenders look for when assessing repayment ability. According to a 2026 small business funding survey, service-based businesses saw a 12% higher approval rate compared to manufacturing firms when applying with credit scores below 600.

What are the typical interest rates for alternative business financing in 2026?

Rates for alternative financing in 2026 typically range from 15% to 45% APR, depending on your specific risk profile and business age. Factor rates, which are common in this space, usually fall between 1.15 and 1.45. While these are higher than bank rates, they reflect the increased risk the lender takes on. Kredline can help you calculate the total cost of capital to ensure the return on your investment justifies the expense.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.