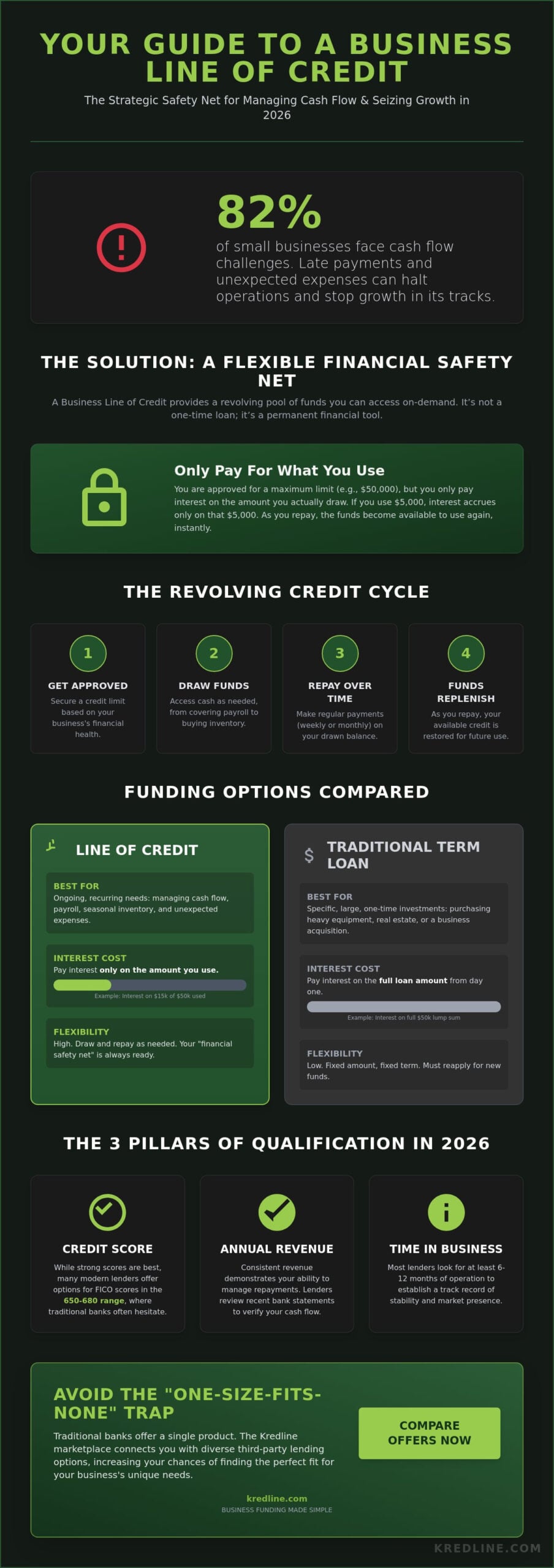

Imagine it’s a Tuesday morning in 2026 and you’re staring at a $20,000 invoice that’s twenty days overdue, while your lease payment is due in forty-eight hours. It’s a scenario that roughly 82% of small businesses face at some point, according to industry data on cash flow management. You know the work is done and the money is coming, but that timing gap feels like a weight on your shoulders. It’s exhausting to feel like you’re constantly chasing your own tail just to keep operations running smoothly.

We believe that managing your company’s finances shouldn’t feel like a high-stakes gamble. You deserve a reliable safety net that’s ready when you are, even if your FICO score sits in that 650 to 680 range where big banks often turn away. In this guide, you’ll learn exactly how a business line of credit works as a strategic tool to bridge revenue dips and seize growth opportunities the moment they appear. We’ll walk through the qualification process, explain the differences between various financing options, and show you how Kredline helps you compare multiple lender offers without the usual headache. By the end, you’ll have a clear roadmap to securing capital that works on your terms.

Key Takeaways

- Understand how a business line of credit provides a flexible safety net, allowing you to access funds on demand and only pay interest on what you actually use.

- Identify the three specific pillars lenders look for in 2026—credit score, revenue, and time in business—so you can prepare your application with confidence.

- Learn to navigate the practical differences between revolving credit and alternative funding options like merchant cash advances to find the right fit for your cash flow needs.

- Explore how a marketplace approach helps you avoid the “one size fits none” trap of traditional banks by connecting you with diverse third-party lending options.

- Gain insights into using flexible capital as a strategic tool to bridge seasonal gaps and fuel growth without the burden of a fixed term loan.

What is a Business Line of Credit and Why Does it Matter?

Cash flow rarely follows a perfect schedule. One month your accounts are full; the next, you are waiting on a $15,000 invoice while a $10,000 payroll deadline looms. A business line of credit solves this mismatch by providing a flexible pool of funds you can tap into whenever a need arises. It isn’t a one-time injection of cash. It’s a revolving resource that stays available as long as you manage it well.

The mechanics are straightforward. You are approved for a maximum limit, but you only pay interest on the specific amount you draw. If you have a $50,000 limit and use $5,000 to cover a seasonal inventory boost, you only owe interest on that $5,000. As you pay it back, those funds become available to use again. According to the foundational definition of a line of credit, this arrangement establishes a maximum loan balance that a borrower can maintain, offering much higher utility than a standard loan for day-to-day operations.

Line of Credit vs. Traditional Term Loans

Traditional term loans deliver a lump sum of cash directly to your bank account. You start paying interest on the full amount immediately, regardless of how quickly you spend it. This structure works well for specific, one-time investments like purchasing a new delivery van or a specialized piece of equipment. If you have a single, large purchase in mind, short-term business loans are often the more logical choice.

A line of credit is different because it’s built for “on-demand” needs. It’s the better tool for recurring expenses like payroll or sudden utility spikes. You don’t have to reapply every time you need cash; you just draw what you need, when you need it. This agility is why many owners view it as a permanent part of their financial toolkit rather than a one-off fix.

The “Safety Net” Strategy for Small Businesses

Waiting until your bank account hits zero to look for funding is a dangerous gamble. In 2026, the most successful businesses use a business line of credit as a proactive safety net. Opening a line while your financials are strong ensures you aren’t forced into emergency borrowing when a crisis hits. High-interest, “last resort” loans can cripple a company’s margins; having an open line prevents that trap entirely.

There’s a significant psychological benefit to this strategy. When you know capital is available, you can focus on growth instead of staring at a calendar. The cost of inaction when a business lacks ready cash is often the lost revenue from a major project you simply couldn’t afford to start. Having that safety net in place means you can say “yes” to opportunities even when your clients are slow to pay their invoices.

How a Revolving Line of Credit Works in Practice

A business line of credit doesn’t function like a traditional loan where you receive a lump sum and start paying interest on the whole amount immediately. Instead, it works like a financial safety net. A lender approves a maximum credit limit based on your company’s health, typically looking at your annual revenue and credit history. If you’re approved for $100,000, that money sits ready for you. You don’t owe anything until you actually move funds into your bank account.

Accessing the money is usually as simple as using an online dashboard or a dedicated business card. You might draw $15,000 to cover a temporary gap in payroll or to snag a discount on bulk inventory. The moment you repay that $15,000, your available credit limit goes back up to the original $100,000. It’s a continuous cycle. Interest stops accruing on any portion of the balance you pay down, which makes this one of the most cost-effective ways to manage short-term needs.

Understanding Draw Periods and Repayment Terms

The lifecycle of a draw starts when you transfer funds and ends when the balance hits zero. Repayment schedules vary by lender; some require weekly payments while others stick to a monthly cycle. Weekly payments can actually help with cash flow management because they prevent large, intimidating bills from hitting your account all at once. Most agreements also feature a renewal period, often every 6 to 12 months. At this point, the lender reviews your recent bank statements. If your revenue has grown, they might even increase your limit to support further expansion.

Secured vs. Unsecured Lines of Credit

Deciding between a secured or unsecured line usually comes down to your business model and assets. Unsecured lines are common for service-based businesses like consulting firms or agencies. You don’t have to pledge specific collateral, but you might face higher interest rates. The lender takes on more risk, so they charge a bit more for the flexibility.

- Unsecured: Best for businesses with few physical assets; faster approval times.

- Secured: Backed by assets like inventory or accounts receivable; often comes with lower rates.

Product-based businesses often prefer secured lines. By using your existing inventory or unpaid invoices as collateral, you can often unlock much higher credit limits than an unsecured option would allow. It’s a practical way to use what you already have to get what you need for the next quarter. If you want to see how these structures could work for your specific situation, you can compare business line of credit details to find the right fit for your cash flow needs.

Qualifying for a Business Line of Credit in 2026

Getting approved for a business line of credit in 2026 requires more than just a decent pitch. Lenders now rely on three main pillars to assess risk: your credit score, your time in business, and your annual revenue. While the process has become more automated, the fundamentals remain the same. Banks want to see that you can repay what you borrow without straining your daily operations.

Typical FICO requirements for traditional bank lines currently range from 660 to 720. If your score sits below 650, you aren’t necessarily out of luck. Alternative lenders often provide more flexibility if your cash flow is strong. However, a lower score usually results in higher interest rates or lower credit limits. It’s a trade-off between accessibility and cost.

Revenue consistency is often more important than the total annual figure. A lender prefers to see $15,000 entering your account every month rather than a single $180,000 windfall followed by months of silence. This predictable flow proves you can handle the monthly interest payments. If you want to see where your current financials land, you can explore your business line of credit options to find a match for your specific profile.

Financial Benchmarks You Need to Meet

Lenders have specific “floor” requirements you must hit before they even look at your tax returns. For a traditional business line of credit, you usually need at least 2 years of operational history. Newer businesses can look toward alternative lenders who often accept 6 months of history if the growth trajectory is steep.

Monthly revenue thresholds typically start at $10,000 for standard lines. Your debt-to-income ratio also plays a massive role. If 45% or more of your monthly income already goes toward existing debt payments, lenders will likely view you as overleveraged. They want to ensure there is a “cushion” left over for unexpected expenses or seasonal dips.

Preparing Your Documentation for a Smooth Application

Speed is essential when you’re trying to bridge a cash flow gap. You should have the last 6 months of business bank statements ready in PDF format. Many modern platforms now allow you to link your accounting software directly. This step often cuts approval times from three days down to just a few hours because it gives the lender a real-time view of your P&L statement.

- Gather your last two years of federal business tax returns.

- Ensure your Profit and Loss statement is updated within the last 30 days.

- Keep a current list of outstanding accounts receivable to show future incoming cash.

Before you hit the submit button, check your business credit report for errors. A single misreported late payment from 2024 can drop your score by 30 points and cost you thousands in unnecessary interest charges over the life of your credit line. If you’re ready to start the process, you can prequalify for business funding to see what rates your current documentation supports.

Line of Credit vs. Alternative Funding Options

A business line of credit is often the most flexible tool in your financial toolkit, but it isn’t a universal solution for every scenario. Choosing the wrong type of capital can lead to unnecessary costs or restricted cash flow when you need it most. You should match the funding source to your specific business goal to ensure your profit margins stay healthy. While a line of credit works best for short-term gaps, other options provide better structures for specific needs like rapid emergencies or large asset purchases.

When an MCA Makes More Sense Than a LOC

If your credit score has dipped below 600 or you lack traditional collateral, a Merchant Cash Advance (MCA) might be the faster path. While a line of credit requires a standard approval process that can take days, an MCA focuses on your daily credit card receipts. This is ideal for retail or hospitality businesses with high sales volume but fluctuating daily revenue. If a walk-in freezer breaks on a Friday night, the 24-hour funding speed of an MCA outweighs the lower cost of a line. You’ll pay a “factor rate,” such as 1.2, rather than an APR. This means you pay back a fixed total amount, which is simpler to calculate for a one-off emergency repair during a busy season.

Choosing Between a LOC and Revenue-Based Financing

A Revenue-Based Financing model offers a unique advantage for high-growth companies. Unlike the fixed monthly payments of a business line of credit, these repayments scale with your monthly income. If you have a slow month, your payment drops; if you have a record-breaking quarter, you pay back faster. This protects your balance sheet during seasonal dips. It’s a partner-style arrangement that doesn’t require giving up equity, making it a favorite for service providers or e-commerce brands with 25% month-over-month growth targets.

For specific asset purchases, equipment funding is usually the smarter play. Using your business line of credit to buy a $45,000 delivery van ties up your operating capital. By using equipment-specific loans, the vehicle itself serves as collateral; this leaves your line open for payroll or inventory. Conversely, don’t use a line of credit for long-term real estate investments. A 10-year property project needs the stability of a mortgage, not a revolving credit facility that could see rate adjustments or annual renewals. In the last 12 months, we’ve seen more owners successfully use a mix of these tools rather than relying on just one.

Not sure which path fits your current goals? You can prequalify for business funding in minutes to see your personalized options.

How to Secure a Business Line of Credit Through a Marketplace

Applying to a single bank often feels like a gamble. Traditional lenders have rigid criteria that don’t always account for the nuances of your specific industry. If you don’t fit their exact mold, you’re out. This “one size fits none” approach leads to a high volume of rejections. In fact, data from recent small business lending indexes shows that large banks still reject roughly 86% of small business loan applications. A marketplace changes this dynamic by connecting you with a network of third-party lenders through a single point of entry.

Instead of pitching your business to one person behind a desk, you’re opening the door to multiple lenders who are actively looking for businesses like yours. This competition works in your favor. When lenders compete, you gain the leverage to compare terms and find the lowest cost of capital. It’s about moving from a position of asking for a favor to choosing the best partner for your growth.

The Advantage of a Marketplace Approach

Speed is the biggest win here. You fill out one application instead of ten. Kredline acts as your navigator in this space, filtering through various alternative lenders to find those that actually want to work with your specific business model. This saves you dozens of hours that would otherwise be spent on repetitive paperwork.

The process also protects your credit score. Most marketplaces use a “soft pull” for the initial matching phase. This means you can explore your options without seeing your score drop by 5 or 10 points before you’ve even seen a formal offer. You get a clear view of the landscape first; you only commit to a hard credit inquiry when you’ve found a match that makes sense for your bottom line.

Next Steps: Prequalifying Without the Stress

Starting the process is straightforward. You’ll need basic business information like your annual revenue, time in business, and recent bank statements. Once the offers start coming in, you need to look past just the interest rate. Transparency is vital. Look for maintenance fees, which can range from $20 to $100 monthly, and draw fees that typically sit between 1% and 3% of the amount you take out.

A marketplace approach simplifies the search for a business line of credit by putting the power back in your hands. You can see the total cost of borrowing upfront, including any origination fees or late payment penalties. When you’re ready to see what’s possible for your cash flow and bridge those seasonal gaps, you can prequalify for business funding today to see your available options. It’s a simple step that provides the clarity you need to plan for 2026 with confidence.

Taking Control of Your Business Capital

Navigating the financial landscape of 2026 requires more than just hard work; it demands the right tools to bridge the gaps between invoices and expenses. A business line of credit serves as a flexible resource that grows with your needs, allowing you to handle seasonal slowdowns or sudden equipment repairs without losing momentum. Data from the Federal Reserve’s 2023 Small Business Credit Survey indicates that nearly 43% of small businesses use financing to cover operating costs, proving that access to capital is a standard part of successful operations.

You shouldn’t have to struggle through mountains of paperwork or confusing corporate jargon to find the right fit. Kredline simplifies this journey by connecting you to a broad network of both traditional and alternative lenders. Our team provides specialized support to help you manage working capital effectively, ensuring you’re never alone in your financial decisions. We prioritize transparency and speed so you can get back to what matters most: running your company.

Explore your business line of credit options and prequalify with Kredline

Your business has a bright future, and the right partner makes getting there much easier.

Frequently Asked Questions

How is a business line of credit different from a business credit card?

A business line of credit provides direct access to cash that you can transfer into your checking account, while a credit card is designed for point-of-sale purchases. You can use the cash from a line of credit for expenses like rent or payroll without paying the high fees associated with credit card cash advances. These lines also typically offer much higher borrowing limits than standard cards, often exceeding $100,000.

Can I get a business line of credit with a credit score below 600?

You can still secure funding with a score below 600, but you’ll likely work with alternative lenders instead of traditional banks. These lenders prioritize your business’s health, often requiring at least $15,000 in monthly revenue to qualify. While your interest rates might be higher, consistent cash flow acts as a powerful offset to a lower personal credit score during the evaluation process.

What are the typical interest rates for an unsecured business line of credit in 2026?

Typical interest rates for an unsecured business line of credit in 2026 range from 8% to 25% APR based on your risk profile. These rates are usually variable and tied to the prime rate, which means they can shift as market conditions change. Businesses with at least two years of operating history and strong annual returns generally qualify for rates on the lower end of this spectrum.

How long does it take to get approved for a business line of credit?

Approval for a business line of credit usually takes between 24 hours and 30 days depending on the lender you choose. Online providers often give you an answer within 48 hours, while traditional banks frequently take 20 to 30 days to review financial statements. If you’re in a hurry, Kredline can help you identify lenders that specialize in fast processing to ensure you don’t miss a growth opportunity.

Are there any hidden fees associated with a business line of credit?

Common fees include origination charges, draw fees, and annual maintenance costs that you should review before signing. Some lenders charge a 1% to 2% fee every time you pull funds from the line. It’s also common to see inactivity fees if you don’t use the credit for six months. Always check your agreement for these specific costs to avoid surprises during your repayment period.

Can I use a business line of credit to pay off other business debts?

You can use the funds to consolidate high-interest debt or clear short-term balances from other lenders. This is a smart way to manage cash flow if you find a line of credit with a lower interest rate than your current loans. It simplifies your monthly payments and can reduce your total interest expense, giving your business more breathing room to invest in new equipment or growth.

What happens if I don’t use the funds in my line of credit?

If you don’t draw any money, you won’t pay any interest on the balance. The funds simply sit there as a safety net for when you actually need them. However, you might still be responsible for an annual fee, which typically ranges from $100 to $500. This small cost ensures the capital stays available for emergencies, seasonal inventory needs, or unexpected repairs without requiring a new application.

Is a personal guarantee required for a small business line of credit?

Most lenders require a personal guarantee for a small business line of credit, especially if the loan is unsecured. This means you’re personally responsible for the debt if the business can’t pay it back. Data shows that 90% of small business lenders include this requirement to manage their risk. It’s a standard part of the process for most modern financing options available to growing companies today.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.