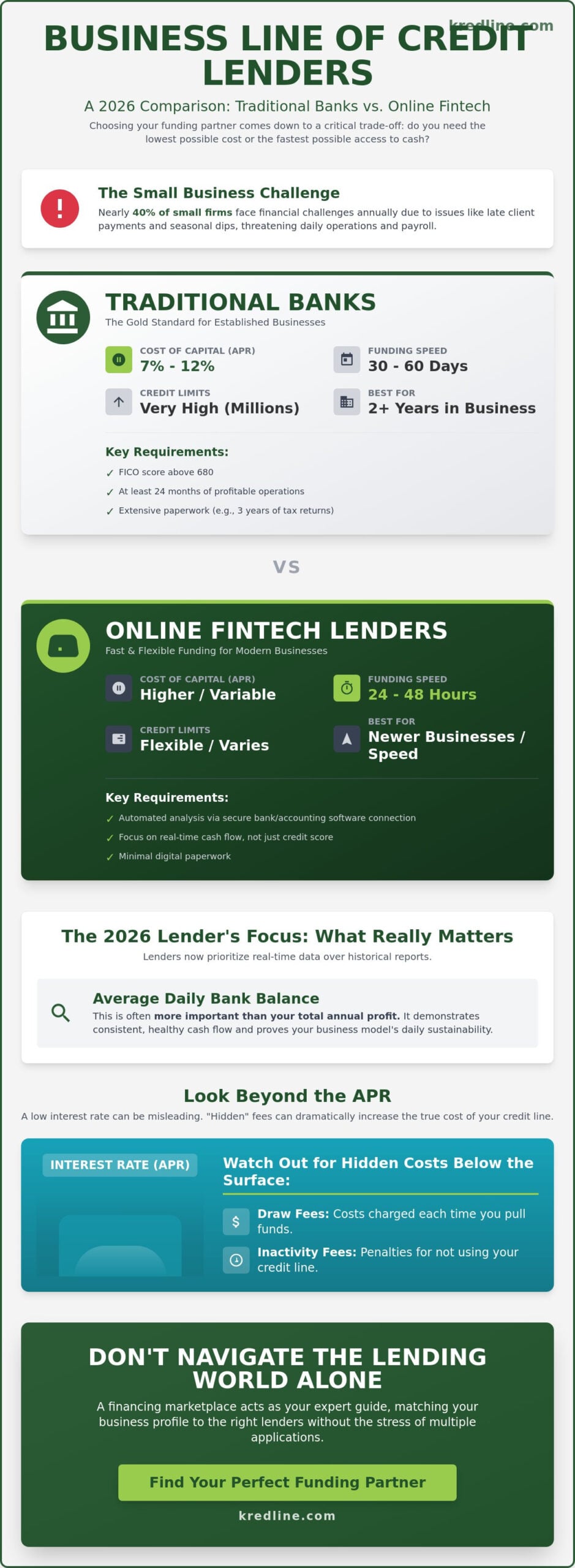

Last Tuesday, a landscaping business owner sat at her desk at 9:00 PM, staring at a $12,000 payroll gap because a major client’s payment was three weeks late. According to recent Federal Reserve data, nearly 40% of small firms face similar financial challenges every year. You’ve likely felt that same knot in your stomach when seasonal dips or delayed invoices threaten your daily operations. It’s exhausting to deal with rigid bank requirements that don’t account for the reality of running a modern company. You deserve a financial cushion that doesn’t come with a mountain of paperwork or confusing fee structures that eat into your hard-earned margins.

Finding the right business line of credit lenders shouldn’t feel like a second full-time job. This guide helps you secure a revolving line with fair rates and fast access to funds so you can focus on growth instead of survival. We’ll examine how to compare different lending models in 2026 and highlight how Kredline simplifies the search for a funding partner that actually understands your business. You’ll learn exactly what to look for to ensure your capital stays flexible and your costs stay low while you build for the future.

Key Takeaways

- Learn why treating a line of credit as a revolving resource provides the ongoing flexibility your business needs to handle unexpected shifts.

- Balance the lower costs of traditional banks with the rapid access of fintech lenders to find the right funding speed for your goals.

- Understand why your average daily bank balance is often more important to business line of credit lenders than your total annual profit.

- Identify the “hidden” fees, like draw and inactivity costs, that can make a low-interest offer much more expensive than it appears.

- Discover how a financing marketplace can act as your navigator, matching your profile to providers without the stress of multiple individual applications.

Understanding the Landscape of Business Line of Credit Lenders

Running a business in 2026 requires more than just a steady bank balance. It requires a safety net that expands and contracts with your needs. A line of credit isn’t a one-time injection of cash that sits in your account gathering interest. Instead, it’s a revolving resource that stays available in the background until you actually need it. Think of it as the Swiss Army Knife of business finance. You might use it to cover a $20,000 payroll during a slow month, or to snag a bulk discount on raw materials that just hit the market.

The primary goal for most owners is bridging the gap between accounts receivable and accounts payable. If your clients operate on 60-day payment terms but your vendors expect payment in 15, that 45-day gap can stall your growth. Most business line of credit lenders offer two paths to solve this:

- Secured Lines: These require collateral, such as real estate or inventory, but usually come with lower interest rates.

- Unsecured Lines: These rely on your credit score and cash flow. They don’t require physical assets as backing, making them faster to access for service-based companies.

Revolving Credit vs. Term Loans

The biggest difference between these models is how you handle the interest. With a term loan, you receive a lump sum and pay interest on the total amount from day one. With a business line of credit, you only pay interest on the specific dollar amount you draw. Revolving credit is a flexible funding arrangement where your available limit resets as you pay back what you’ve borrowed, giving you a reusable source of capital. It’s a game-changer for cash flow because you aren’t paying for “idle” money.

The 2026 Shift in Lending Standards

Lending has changed significantly over the last few years. By 2026, the days of mailing stacks of paper tax returns are largely over. Modern business line of credit lenders now use automated underwriting that connects directly to your business bank account via secure APIs. This allows for real-time data analysis and funding decisions in as little as 24 hours. While the process is faster, “time in business” remains a major hurdle. Most national lenders still look for a minimum of 12 to 24 months of operational history to prove your business model is sustainable. If you’re looking to see where you stand, you can prequalify for business funding to understand your options without a hard credit pull.

Traditional Banks vs. Online Fintech Lenders

Choosing between a local bank and a digital platform often comes down to a simple trade-off: do you need the lowest possible cost or the fastest possible cash? Most business line of credit lenders fall into one of these two camps. Each has a specific appetite for risk and a different way of evaluating your company’s health. Understanding where you fit can save you weeks of wasted paperwork.

The Case for Traditional Bank Lenders

Traditional banks remain the gold standard for established companies with a clean paper trail. If your business has been profitable for at least 24 months and you maintain a personal FICO score above 680, a bank is likely your best path. The primary benefit is the cost of capital. You’ll typically find APRs ranging from 7% to 12%, which is significantly lower than alternative options. Banks also offer much higher credit limits, often scaling into the millions for qualified borrowers.

Beyond the numbers, banks offer a dedicated relationship manager. This person acts as a long-term partner who understands your local market. They can help you transition from a simple line of credit to more complex financing as you grow. However, the process is slow. Expect to provide three years of tax returns and wait 30 to 60 days for a final decision. This is why SBA guidance on business lines of credit often suggests starting the application process long before you actually need the funds.

The Rise of Fintech and Alternative Platforms

Online fintech lenders have filled the gap for businesses that don’t meet strict bank criteria or simply can’t wait two months for an answer. These platforms prioritize data and speed. By linking your accounting software or business bank account, these lenders can analyze your real-time cash flow and provide an approval in minutes. Funding often hits your account within 24 to 48 hours.

One major advantage of fintechs is the “soft pull” credit check. Unlike banks that perform a hard inquiry immediately, many online platforms let you see your potential terms without affecting your credit score. This allows you to compare multiple Kredline funding options without the risk of lowering your FICO during the search. While the interest rates are higher than traditional banks, the agility they provide is vital for covering unexpected payroll gaps or jumping on a limited-time inventory discount.

Most business line of credit lenders require a personal guarantee, meaning you’re personally responsible if the business defaults. However, as your revenue grows, some alternative lenders offer unsecured lines that don’t require specific collateral. If you’re unsure which route matches your current revenue, you can prequalify for business funding to see what’s available for your specific situation.

What Lenders Look for in a 2026 Application

When you approach business line of credit lenders, the evaluation process goes deeper than a simple glance at your tax returns. Modern lenders focus on the three pillars of a successful application: credit, cash flow, and character. Credit shows your past behavior, cash flow proves your current ability to repay, and character reflects your professional experience and the resilience of your business model. Most lenders want to see that you’ve been in operation for at least six to twelve months before they’ll consider a revolving line.

Many business owners assume a high annual profit is the most important metric. In reality, your average daily bank balance often carries more weight. Lenders look for a “cushion” that suggests you can handle unexpected expenses without draining your account to zero. A business that maintains a steady $8,000 daily balance is frequently viewed as more stable than one that nets $200,000 a year but frequently sees its balance drop into the low hundreds. They also scrutinize your debt-to-income ratio. In a commercial context, lenders generally prefer that your total monthly debt obligations don’t exceed 30% to 40% of your average monthly revenue.

To keep the process moving, you’ll need your documentation ready. This typically includes:

- Your last four to six months of business bank statements.

- A year-to-date profit and loss (P&L) statement.

- Your most recent business tax return.

- Basic details about your business ownership and legal structure.

While some fintech platforms use automated algorithms to scan these documents, others may look for how your business aligns with broader SBA loan programs or traditional banking standards to determine your risk level.

The Credit Score Factor

Lenders look at two different scores during the process. Your personal FICO score remains a major factor, especially for small businesses, but your business credit score (like a Paydex score) is equally vital. Paydex scores range from 1 to 100, and a score above 80 tells lenders you pay your bills on time or even early. Before you apply, check your reports with bureaus like Dun & Bradstreet. Errors are common; a 20% inaccuracy rate in business credit files can lead to higher interest rates or unnecessary rejections. A credit score is the cover of your book, but lenders read the whole story before they sign the check.

Cash Flow and Revenue Consistency

Lenders love boring, predictable numbers. They prefer to see 15 small, steady deposits throughout the month rather than one massive windfall that leaves your account stagnant for weeks. If you run a seasonal business, don’t worry. You can still qualify by providing 24 months of bank statements to show that your “slow” months are a predictable pattern rather than a sign of failure. For businesses with high transaction volumes but fluctuating margins, revenue-based financing can serve as a practical alternative if traditional business line of credit lenders require more rigid consistency than your industry allows.

How to Compare Offers Beyond the Interest Rate

Focusing purely on the interest rate is a trap many owners fall into. While a low rate looks great on paper, the operational costs of working with different business line of credit lenders can quickly change the math. You need to look at the “hidden” fees that drain your available capital before you even spend a cent. Draw fees are common; these usually range from 1% to 3% every time you pull funds. If you’re making small, frequent draws to cover payroll, these costs add up fast.

Maintenance and inactivity fees are also worth watching. Some lenders charge a monthly fee just to keep the line open, while others penalize you if the account sits idle for more than 90 days. You should also consider the repayment rhythm. Weekly payments might work for a high-volume restaurant, but they can stifle a B2B company waiting 30 days for an invoice to clear. The replenishment process is another critical factor. A true revolving line resets your limit as you pay back the principal, giving you a continuous safety net without needing to reapply.

The True Cost of a Line of Credit

Don’t confuse a factor rate with an interest rate. A factor rate is a fixed multiplier applied to the total amount you borrow. This means you pay the same cost regardless of how quickly you pay it back. To find the real impact on your bottom line, calculate the effective APR. This includes the interest plus all origination and processing fees. Ask your lender if they offer incentives for early repayment. Some lenders actually charge a prepayment fee to recoup lost interest, while others give you a discount for clearing the balance early.

Flexibility and Scalability

A good credit line should grow with your business. Choosing between different business line of credit lenders requires a deep dive into their growth policies. Ask if the lender allows for limit increases after six months of consistent, on-time payments. You also want to know if the funds are restricted. While most lines are for general working capital, some owners use them as a bridge for equipment funding when an urgent replacement is needed. The ease of use matters too. A modern digital portal that allows for instant draws is far more valuable than a traditional bank process that takes three days to move money.

Finding the Right Fit Through a Financing Marketplace

Running a business takes every bit of focus you’ve got. You don’t have time to fill out twelve different forms for twelve different business line of credit lenders. Research shows that small business owners can spend over 24 hours on paperwork for a single traditional bank loan application. Applying to one lender at a time is slow, and it’s often inefficient. Each rejection feels like a setback, and each new application starts the clock over again while your cash flow needs remain urgent.

Kredline acts as your navigator in this crowded market. We don’t just throw your data at a wall to see what sticks. We match your specific business profile to a curated network of providers. Instead of a “one-size-fits-all” approach, you get a single application that reaches banks, credit unions, and alternative lenders simultaneously. This transparency ensures you see the full picture of what’s available without the usual guesswork or hidden agendas.

The Broker Advantage

The biggest risk in searching for capital is the “hard pull” on your credit. Every time a lender checks your credit officially, your score can take a hit, sometimes dropping by 5 to 10 points. Kredline helps by pre-screening your business first. We look at your health and performance to see which business line of credit lenders are actually looking for a profile like yours before any formal inquiry happens.

Our role is to be your advocate. We understand which lenders have an appetite for certain industries, whether you’re running a seasonal retail shop or a high-growth construction firm. We handle the heavy lifting by comparing terms for you. This includes:

- Identifying lenders with the fastest funding times, often within 24 to 48 hours.

- Comparing draw fees and maintenance costs that aren’t always obvious.

- Matching you with providers that offer flexible repayment structures tailored to your revenue cycles.

Next Steps: Prequalifying Without Risk

Getting started doesn’t have to be a hurdle. You can prequalify for business funding in just a few minutes through our streamlined platform. The process is designed to be low-impact and high-value, giving you a clear view of your borrowing power without the stress of a traditional bank interview.

Having your last 3 to 6 months of bank statements ready will speed things up significantly. This data gives lenders a clear view of your real-time cash flow, which is often more important than a simple credit score in 2026. Once you upload these documents, our team works to find the most competitive offers in our network.

Finding capital should be a tool for your growth, not a source of constant stress. When you have the right partner, you stop worrying about the logistics of the search and start focusing on how that capital will move your business forward. It’s about making the financial side of your business as efficient as the operational side.

Take the Next Step Toward Smarter Business Funding

Choosing the right financing in 2026 comes down to matching specific terms with your daily operational needs. You now understand that while interest rates matter, the true value lies in how a partner handles draw periods and repayment flexibility. It’s about having capital ready before you actually need it, whether that’s for an unexpected equipment repair or a bulk inventory purchase that’s too good to pass up. This proactive approach keeps your cash flow steady and your mind focused on the bigger picture.

We’ve built a platform that removes the stress of the traditional application process. By connecting you with a network of 50+ third-party lenders, we help you compare real offers side by side. You won’t face a hard credit pull just to see your initial options, which keeps your financial profile protected while you shop. In many cases, you can secure funding in as little as 24 hours. This speed ensures you don’t miss out on growth opportunities because of slow bank approvals.

See which business line of credit lenders you qualify for today with Kredline

You’ve done the hard work of building your business; now let’s find the capital that helps it thrive.

Frequently Asked Questions

How long does it take to get approved for a business line of credit?

You can often get approved within 24 to 48 hours through online lenders, while traditional banks typically take 3 to 5 weeks to process your application. If you have your 2025 tax returns and recent bank statements ready, the process moves much faster. Kredline helps you compare these timelines so you can secure funding before your next payroll or inventory deadline arrives.

Can I get a business line of credit with a 600 credit score?

Yes, you can qualify with a 600 credit score, but you’ll likely need to work with alternative business line of credit lenders instead of traditional banks. These lenders often prioritize your monthly revenue, usually looking for at least $10,000 in consistent deposits, rather than just your credit score. It’s a realistic option for business owners who are rebuilding their credit while managing a profitable company.

What is the difference between a secured and unsecured business line of credit?

A secured line requires you to pledge assets like real estate or equipment as collateral, while an unsecured line relies solely on your business’s financial health. Most small businesses prefer unsecured lines because they don’t risk specific assets; however, these often come with slightly higher interest rates. If you don’t own a warehouse or heavy machinery, an unsecured option is usually the most accessible path for your cash flow needs.

Do business line of credit lenders require a personal guarantee?

Most business line of credit lenders require a personal guarantee, which means you’re personally responsible for the debt if the business cannot pay. Industry data shows that approximately 90% of small business financing agreements for companies with under $5 million in revenue include this requirement. It’s a standard practice that helps lenders offer more flexible terms to growing companies that might not have decades of credit history.

How much can I typically borrow with a business credit line?

Most small businesses qualify for limits between $5,000 and $250,000, depending on their annual gross sales and time in business. Lenders typically set your limit at 10% to 20% of your total yearly revenue. For example, if your company generates $1 million in annual sales, you might see offers for a $100,000 line to help bridge the gap between client invoices and your monthly expenses.

Can a new startup qualify for a business line of credit?

You generally need at least 6 months of operating history to qualify, though some modern lenders will consider startups with only 3 months of revenue. You’ll need to show consistent growth and a minimum of $100,000 in projected annual sales to be a strong candidate. Kredline can help you identify which specialized lenders are currently active in the startup space so you don’t get stuck with rigid bank requirements.

Are there fees if I don’t use my business line of credit?

Some lenders charge an annual maintenance fee or an inactivity fee, which typically ranges from $100 to $500 depending on the size of the line. Many online providers have moved away from these costs, only charging interest on the funds you actually draw. You should always review your contract for “draw fees” or “origination fees” to ensure the line stays affordable even when it’s sitting idle as an emergency fund.

How does a business line of credit affect my credit score?

The initial application usually triggers a hard credit pull, which can temporarily lower your score by about 5 to 10 points. In the long run, maintaining a line and making on-time payments can significantly improve your business credit profile over 12 months. It’s a strategic way to demonstrate financial responsibility, making it easier to qualify for larger loans or better rates when you’re ready to expand your operations.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.