Last Tuesday, a landscaping firm owner realized that bringing on a silent investor through a limited partnership was the only way to fund three new crews without risking her family home if the market shifted. It’s a common crossroads for entrepreneurs who need capital but aren’t ready to hand over the keys to their entire operation.

You probably already know that the right legal structure can make or break your peace of mind. Balancing the tax benefits of a partnership against the fear of personal liability for a partner’s mistake is a heavy burden for any small business owner to carry. This guide will help you master the essentials of the structure, from legal liability and tax benefits to how it impacts your ability to secure business funding. We’ll break down the relationship between general and limited partners and provide a clear framework to help you decide if this is the right vehicle for your 2024 growth goals.

Key Takeaways

- Understand the critical distinction between general and limited partners to protect your personal assets while maintaining operational control.

- Learn why a formal partnership agreement and state registration are necessary to move beyond the risks of a basic general partnership.

- Discover how a limited partnership compares to an LLC and why it may be the more flexible choice for attracting passive investors.

- Identify how your business structure and personal credit impact your ability to secure capital, including options like short-term business loans.

- Evaluate the scalability of your business by weighing the benefits of rapid capital raising against the legal and tax complexities of the LP structure.

What is a Limited Partnership (LP) and How Does It Work?

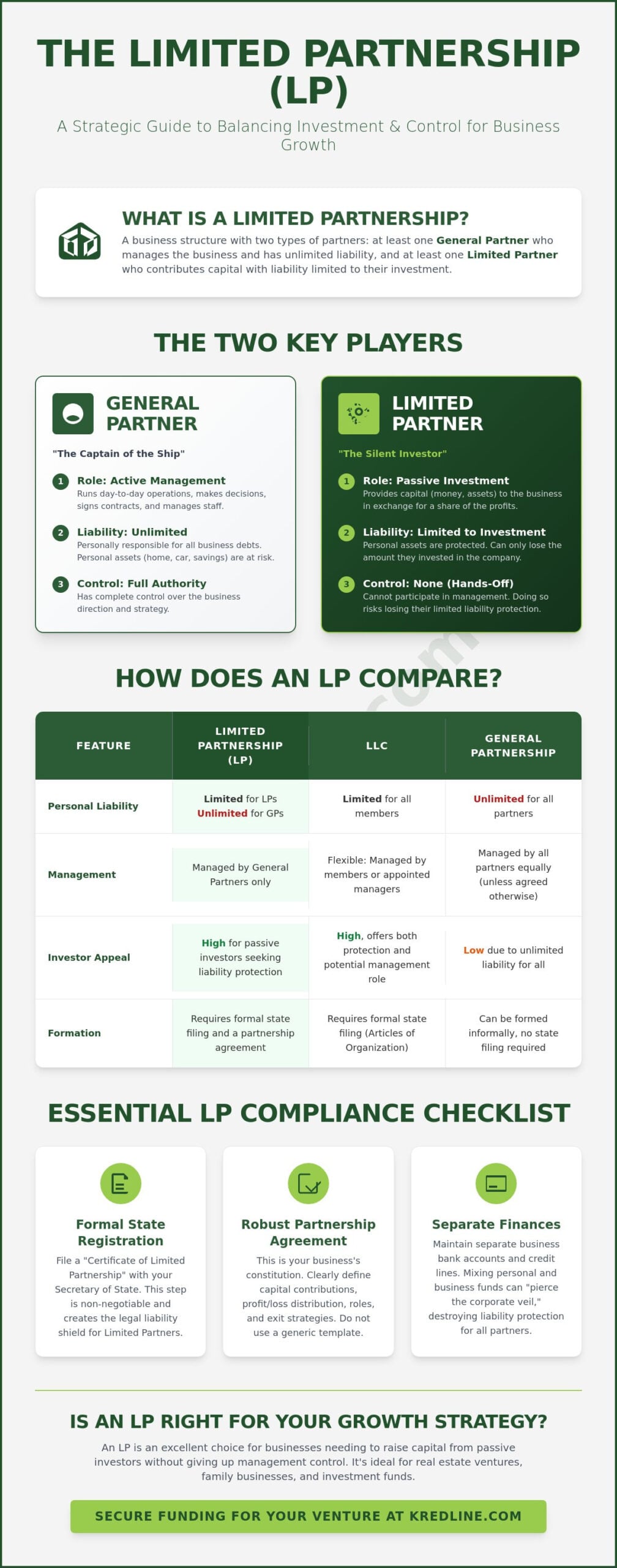

A limited partnership is a specific business structure that divides a company into two distinct camps: those who run the day-to-day operations and those who provide the capital. To form one, you must have at least one general partner and at least one limited partner. This setup is a staple in the business world because it allows for a clean split between management and investment. To get a better sense of the legal history and foundational rules, you can read more about What is a Limited Partnership and how it functions across different jurisdictions.

This structure remains the “old-school” favorite for real estate syndicates, law firms, and family-owned businesses. In fact, many private equity and venture capital firms use this model to manage billions in assets. It works well when one person has the expertise to run a business but needs outside cash to scale. It’s also a common choice for families who want to pass down assets while keeping control in the hands of a single, experienced family member. If you are looking for funding options to expand your role in such a venture, understanding these boundaries is the first step.

Limited partners enjoy a specific legal shield that ensures their personal assets remain protected from business debts beyond the exact dollar amount they have already invested in the company.

The General Partner: The Captain of the Ship

The general partner (GP) is the person in the driver’s seat. They have full authority to make decisions, sign contracts, and hire staff. They are the primary face of the business for lenders and vendors. If the business needs a line of credit or a lease, the GP is the one who negotiates the terms and signs the paperwork. This power comes with a significant trade-off. The GP has unlimited personal liability. If the business is sued or falls into debt it cannot pay, the GP’s personal bank accounts, vehicles, and real estate can be seized to cover the costs. It’s a high-stakes role that requires both confidence and a clear strategy for managing cash flow.

The Limited Partner: The Silent Investor

Limited partners are often called “silent partners” for a reason. Their primary job is to write a check and then step back. This “hands-off” rule is the cornerstone of their asset protection. As long as they stay out of the management side, their personal wealth is safe from the business’s creditors. They cannot negotiate deals, direct employees, or make executive decisions. If a limited partner crosses that line and starts acting like a manager, they risk losing their “limited” status. In a legal dispute, a court can strip away their liability protection if it’s proven they were actually running the show. For most investors, the goal is to provide the fuel without ever touching the steering wheel.

Operational Reality: Compliance, Taxes, and Agreements

Setting up a limited partnership isn’t a “handshake and go” situation. Unlike a general partnership, which can technically exist without formal paperwork, an LP requires a deliberate filing with the Secretary of State. You’ll typically file a Certificate of Limited Partnership and pay a state-specific fee, which ranges from $50 to over $500 depending on your jurisdiction. This formal registration is what creates the legal wall protecting your limited partners. If you skip this step, you risk the state treating the entity as a general partnership, where every partner carries full personal liability for the company’s debts.

Operational safety also relies on strict financial boundaries. You must maintain separate business bank accounts and credit lines. If a general partner pays personal bills from the business account, a process known as “piercing the corporate veil” can occur. In legal disputes, this allows creditors to argue that the business isn’t a separate entity, potentially exposing the personal assets of even the limited partners. Keeping your books clean ensures the liability protections you worked for actually hold up in court.

Drafting a Partnership Agreement That Actually Works

Your partnership agreement is the backbone of the business. Don’t rely on a generic $20 template found online for a venture involving significant capital. A robust agreement must clearly define capital contributions; for instance, if one partner brings $50,000 in cash and another brings $50,000 in equipment, the document should reflect those specific valuations. You also need a clear “exit strategy.” Data from the Bureau of Labor Statistics shows that about 20% of small businesses fail within their first year, and many of those failures are compounded by messy breakups. Your agreement should specify how a partner’s interest is valued and sold if they decide to leave or if a dispute arises that cannot be resolved through mediation.

Understanding the Pass-Through Tax Advantage

The primary fiscal draw of the limited partnership is avoiding the “double taxation” faced by C-corporations. The business itself doesn’t pay federal income tax. Instead, profits and losses “pass through” to the partners. Each year, the LP files Form 1065 with the IRS and issues a Schedule K-1 to every partner. This form breaks down each person’s share of the income, which they then report on their personal 1040 tax return.

One detail to watch is the self-employment tax. While limited partners usually enjoy passive income treatment, the general partner is typically subject to the 15.3% self-employment tax on their share of the profits because they are actively managing the business. Understanding these nuances helps you manage your cash flow more effectively. If you’re looking to scale or need to bridge a gap while waiting for these tax advantages to kick in, you can prequalify for business funding to see what options fit your current structure.

Limited Partnership vs. LLC vs. General Partnership

Choosing a business structure isn’t just about paperwork; it’s about building a wall between your personal savings and your business obligations. In a standard LLC, every member enjoys a shield against personal liability. A limited partnership functions differently by splitting the room. General partners manage the day-to-day work and carry full liability, while limited partners act as passive investors with protected personal assets. Filing fees vary significantly by state. For example, forming an LP in Delaware costs $200, while California charges a $70 filing fee plus a mandatory $800 annual franchise tax. Over time, LPs can become more expensive than LLCs because they often require more complex legal agreements to maintain the strict separation of partner roles.

A General Partnership is often the riskiest choice for a growing business because every partner shares unlimited personal liability for the actions and debts of the others. This means a single bad decision by one person can put every owner’s home or personal bank account at risk. If you are currently operating under a handshake deal, transitioning to a more formal structure is a vital step in protecting what you’ve built. If you’re ready to scale that new structure, you can prequalify for business funding to see which capital options fit your specific entity type.

When to Choose an LP Over an LLC

LPs are the gold standard for businesses that rely on “silent” investors. While LLCs often encourage a democratic management style, an LP creates a clear hierarchy. This prevents the “too many cooks in the kitchen” syndrome that often stalls decision-making in growing companies. Professional investment groups and real estate syndicates often prefer the limited partnership because it allows the experts to run the operations while providing investors with a clear, hands-off role. It’s a cleaner way to bring in capital without giving up control of the steering wheel.

The Dangers of a Standard General Partnership

Many small businesses start as general partnerships because they’re easy to form, often requiring nothing more than a verbal agreement. However, these “handshake deals” lead to joint and several liability nightmares where you’re 100% responsible for 100% of the business debt, regardless of your ownership percentage. Moving to an LP structure shields your investors and clarifies everyone’s financial exposure. If you’re moving away from a general partnership, follow this transition checklist:

- Draft a formal Partnership Agreement: Clearly define the roles of general and limited partners.

- File with the State: Submit a Certificate of Limited Partnership to your Secretary of State.

- Secure a new EIN: The IRS usually requires a new tax ID when changing business structures.

- Notify Creditors: Update your bank accounts, leases, and vendor contracts to reflect the new legal entity.

By formalizing your structure, you create a professional foundation that makes it much easier to secure business lines of credit or other growth capital down the road.

Financing a Limited Partnership: Challenges and Opportunities

Lenders view the limited partnership structure through two different lenses. They see the general partner (GP) as the captain of the ship and the limited partners as passive passengers. Because the GP has total control and unlimited liability, banks almost always base their lending decisions on the GP’s personal credit history and financial health. If you’re the general partner, your credit score is the key that opens or locks the door to capital.

The limited partnership model is particularly effective when you want to attract private equity or angel investors. These individuals often prefer the LP structure because they can inject capital into a promising venture without risking their personal assets beyond their initial investment. They get the tax benefits of a flow-through entity without the burden of daily management or legal exposure. This clear separation of roles makes it easier to pitch your business to high-net-worth individuals who want to be silent partners.

Securing Working Capital for Your Partnership

Managing cash flow can be tricky when you’re balancing the needs of multiple partners. If your business experiences seasonal fluctuations, short-term business loans provide a way to cover payroll or inventory costs during slow months. For partnerships that lack heavy collateral but have strong monthly sales, revenue-based financing offers a flexible alternative where repayments scale with your income.

If your partnership operates in the retail or service industry and processes a high volume of card payments, a merchant cash advance can provide speed when you need to fix equipment or handle an emergency. When you apply for these options, lenders will typically require:

- The formal partnership agreement.

- Schedule K-1 forms for all partners from the last two tax years.

- Updated profit and loss (P&L) statements.

- At least four to six months of recent business bank statements.

The General Partner’s Personal Guarantee

In a traditional lending environment, the general partner almost always bears the burden of a personal guarantee. This means you’re legally on the hook if the business can’t pay its debts. According to the 2023 Small Business Credit Survey, 53% of firms reported a financing shortfall, often because they couldn’t meet the rigid collateral requirements of traditional banks. This reality makes the GP’s role naturally more stressful.

To protect your personal assets while pursuing growth, you might look toward alternative financing marketplaces. These platforms often offer more flexibility than traditional banks and may have different requirements for personal guarantees depending on the business’s performance. Using these resources allows the GP to leverage the business’s actual revenue rather than just their personal net worth. It’s a way to keep the business moving forward without feeling like your personal future is constantly on the line.

Wondering which funding path fits your partnership’s current goals? Prequalify for business funding today to see your options without the typical bank hassle.

Is a Limited Partnership Right for Your Growth Strategy?

Deciding on a limited partnership isn’t just a legal formality; it’s a strategic move for your business’s future. This structure works best when you have the expertise to run the daily operations but lack the liquid capital to scale. You maintain total control as the general partner, while your investors provide the necessary funding without interfering in your management decisions. It’s a balance of power that keeps the vision clear while fueling growth.

The primary trade-off involves personal liability. As the general partner, you carry the legal and financial weight of the business. Limited partners only risk the capital they’ve contributed. This setup makes the limited partnership highly scalable. If you need to raise $250,000 for a specific project, you can bring on five limited partners at $50,000 each. You get the capital quickly, and they get a share of the profits without the burden of management duties.

Determining Your Capital Needs

Growth requires a clear understanding of your cash flow requirements. Some projects need a large upfront investment, while others benefit from a flexible business line of credit to manage seasonal gaps. In 2023, industry data showed that nearly 70% of real estate investment syndications used this structure because it allows for passive investment in capital-intensive assets. If you’re ready to see how much capital your business can access, prequalifying for business funding through Kredline provides a clear starting point without the rigid pressure of a traditional bank.

Consulting the Professionals

Don’t attempt to formalize this structure alone. You need a CPA to handle the pass-through tax complexities and an attorney to draft a partnership agreement that protects everyone. These professionals ensure your foundation is solid. Kredline fits into this team as your financial navigator. We help you explore funding options that align with your partnership’s goals, focusing on speed and transparency rather than red tape.

To maintain a healthy partnership over the long term, prioritize communication. Provide your limited partners with regular updates on financial performance and project milestones. This transparency builds trust, making it much easier to raise capital for your next venture. When your partners feel informed, they’re more likely to remain long-term allies in your business journey.

Moving Your Business Strategy Forward

Choosing a limited partnership is a strategic move for owners who want to scale without giving up daily operational control. It bridges the gap between needing fresh capital and maintaining a clear management hierarchy. By now, you understand that success hinges on a solid agreement and a clear grasp of tax obligations. According to the IRS, this structure allows for pass-through taxation, which can simplify your filing process compared to a corporation. Whether you’re comparing this to an LLC or using it as a growth vehicle, the focus remains on sustainable cash flow. Managing payroll or bridging gaps between invoices shouldn’t slow your momentum.

Kredline functions as a dedicated partner in this process, helping you navigate the complexities of business capital. You can explore flexible funding options for your partnership at Kredline and access a broad network of 3rd party providers. It takes only minutes to prequalify without a hard credit pull affecting your score. They specialize in tailored solutions like revenue-based financing and MCAs, which align with your actual business performance. Getting the right support means you can focus on running your company while the financial logistics are handled. You’ve built a strong foundation; now it’s time to put your growth plan into motion.

Frequently Asked Questions

Is a general partner personally liable for the debts of a limited partnership?

Yes, a general partner is personally liable for all the debts and legal obligations of a limited partnership. This means if the business can’t pay its bills, creditors can go after your personal assets, like your home or car. It’s a high-risk role compared to the limited partner, who only risks what they’ve invested. This is why many owners structure the general partner as a business entity instead of an individual.

Can a limited partner be fired from the business?

You can’t fire a limited partner like a regular employee because they’re an owner, not just a worker. However, the partnership agreement usually outlines specific conditions under which a partner can be removed or bought out. If a partner violates their duties or the business needs to restructure, the legal terms set at the start will dictate how the separation happens. Clear contracts prevent messy disputes during these transitions.

What is the main difference between a limited partnership (LP) and a limited liability partnership (LLP)?

The main difference is that a limited partnership requires at least one general partner with unlimited liability, while a limited liability partnership (LLP) protects all partners from the firm’s debts. In an LP, the limited partners stay out of daily management to keep their liability protection. Small business owners often choose an LLP to ensure no single person is on the hook for the entire company’s financial mistakes.

How are profits distributed in a limited partnership?

Profits in a limited partnership are typically distributed based on the percentages outlined in the formal partnership agreement. Most businesses choose to divvy up earnings based on how much capital each person contributed. For example, if you provided 30 percent of the initial funding, you’d likely receive 30 percent of the profits. These payments are passed through to the partners’ personal tax returns, avoiding double taxation.

Can a corporation be a general partner in an LP?

A corporation can absolutely serve as the general partner in a limited partnership. This is a common strategy used to shield individuals from personal liability. By having a Corporation or an LLC act as the general partner, the business gains the structure of an LP while ensuring that no single human being has their personal bank account exposed to business lawsuits or debts.

What happens if a limited partnership goes bankrupt?

If a limited partnership goes bankrupt, the general partner is responsible for paying off the remaining debts using their personal assets. Limited partners generally only lose the money they already invested in the company. Their personal property remains safe unless they overstepped their role and participated in daily management. It’s a stark reminder of why clear roles and financial planning are vital for long term stability.

Do I need a lawyer to form a limited partnership?

You aren’t legally required to hire a lawyer to form a limited partnership, but skipping professional advice is risky. While you can file the basic paperwork yourself, a lawyer ensures your agreement covers critical what-if scenarios. Roughly 70 percent of business partnerships eventually face internal conflict. If you’re looking to secure the capital for these legal and setup fees, Kredline can help you explore your funding options.

How much does it cost to start a limited partnership in 2026?

Starting a limited partnership in 2026 involves state filing fees that typically range from $50 to $500 depending on your location. For instance, California has historically charged a $70 filing fee plus an annual $800 franchise tax. You’ll also need to budget for legal drafting and potential publication requirements in certain states. Managing these startup costs effectively helps keep your cash flow healthy as you move toward your first growth milestone.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.