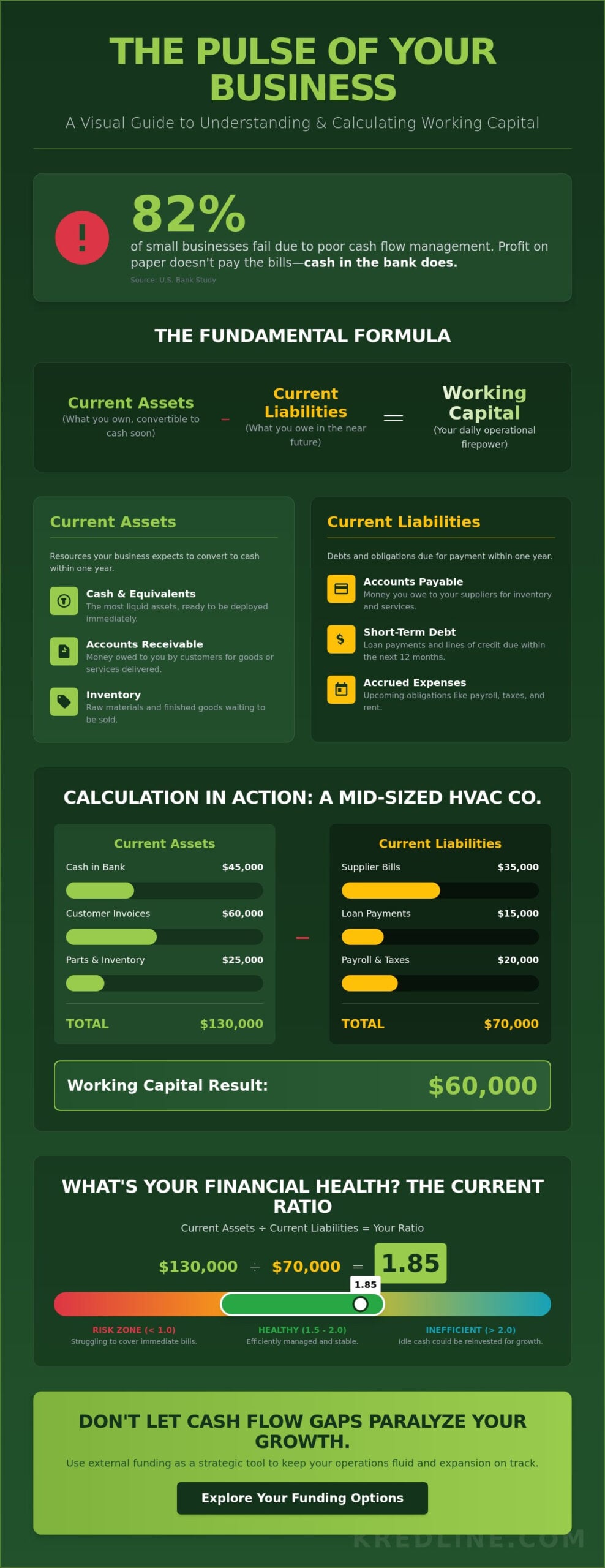

On a Tuesday morning in June 2026, a local wholesaler realizes they have $85,000 tied up in inventory while a $20,000 supplier invoice sits unpaid on their desk. It’s a classic squeeze that has nothing to do with profitability and everything to do with timing. You’ve likely felt that same knot in your stomach when a major customer’s payment window stretches from 30 to 60 days while your own bills stay due on the first. It’s a common reality; in fact, a study by U.S. Bank found that 82% of small businesses fail because of poor cash flow management. Managing your working capital shouldn’t feel like a constant balancing act on a high wire.

We’re here to help you regain control. You’ll learn exactly how to calculate your current liquidity and find actionable ways to speed up your cash cycle. We’ll also explore non-bank funding options that offer the modern flexibility your business needs to grow. By the end of this guide, you’ll have a clear roadmap to keep your operations fluid and your growth on track, even during seasonal dips. Let’s move past the stress of the gap and build a more resilient financial foundation together.

Key Takeaways

- Understand why daily liquidity is the true pulse of your business and how it differs from long-term profitability.

- Master the standard formula to calculate your working capital and determine if your current ratio indicates financial stability or potential risk.

- Identify the hidden bottlenecks in your cash-to-cash cycle that are trapping your money and preventing reinvestment.

- Learn practical internal strategies to optimize cash flow, such as renegotiating supplier terms to keep more cash available for operations.

- Discover how to use external funding as a strategic tool for business expansion rather than a temporary fix for management gaps.

Understanding Working Capital: The Pulse of Your Daily Operations

Think of your business like a high-performance engine. Profit is the horsepower you’re capable of reaching, but working capital is the oil that keeps the parts from seizing up. Technically, working capital represents the difference between your current assets, like cash and accounts receivable, and your current liabilities, such as utility bills and short-term debt. It’s what you have left to run the business day-to-day after accounting for what you owe in the near future.

Many owners confuse this with simple cash flow or long-term profitability. That’s a dangerous mistake. You can have a record-breaking sales month and still find yourself unable to meet payroll. A study by U.S. Bank found that 82% of small businesses fail because of poor cash flow management. This is the “Profit vs. Cash” paradox. Profit is an accounting theory; cash is a cold, hard reality. If your money is tied up in unpaid invoices for 60 days, your “profitable” business is effectively paralyzed.

Why Working Capital Matters for Your Survival

Survival isn’t just about avoiding bankruptcy. It’s about having the agility to handle the unexpected. When a walk-in freezer breaks or a primary supplier raises prices by 12% without notice, you need liquid funds immediately. Maintaining healthy working capital allows you to jump on bulk inventory discounts that save you money in the long run. It also keeps your reputation solid. Paying vendors on time builds the kind of trust that leads to better terms and priority service when supply chains get tight.

Positive vs. Negative Working Capital

Positive working capital means you have more than enough to cover your upcoming bills. It’s a sign of operational efficiency. However, having too much cash sitting idle can also mean you aren’t reinvesting enough. Negative working capital is often a red flag, but for some high-turnover businesses, like grocery stores or fast-food chains, it’s a standard model because they sell inventory before they have to pay the supplier.

For most, negative capital leads to the emotional exhaustion of “chasing cash.” This stress distracts you from growing your brand. If you’re constantly checking the bank balance before making a move, it might be time to look at funding options that can bridge those gaps. At Kredline, we help you find the right tools to keep your operations steady so you can focus on the work you actually love. We take the weight off your shoulders by navigating the complexities of the credit market for you.

How to Calculate Working Capital: A Step-by-Step Breakdown

Calculating your available cash isn’t just about looking at your bank balance. It requires a clear view of what you own and what you owe over the next twelve months. The standard formula is simple: Current Assets minus Current Liabilities. This figure represents the working capital available to fund your daily operations and handle unexpected costs.

Current assets are the economic resources a business expects to convert into cash or use up within one fiscal year, including cash, accounts receivable, and inventory. When you divide these assets by your liabilities, you get the “Current Ratio.” Most advisors look for a ratio between 1.5 and 2.0. If your ratio is 1.0 or lower, you’re likely struggling to cover immediate bills. If it’s above 2.0, you might be keeping too much cash idle instead of reinvesting it into growth. Mastering working capital management helps you find the balance between having enough liquidity and maximizing your profit potential.

Let’s look at a realistic example. Imagine a mid-sized HVAC service company. They have $45,000 in the bank and $60,000 in outstanding customer invoices. They also carry $25,000 in parts and equipment inventory. Their total current assets are $130,000. On the other side, they owe $35,000 to suppliers, have $15,000 in short-term loan payments due this year, and $20,000 set aside for upcoming payroll and taxes. Their total liabilities are $70,000. By subtracting the liabilities from the assets, the owner sees they have $60,000 in working capital with a healthy current ratio of 1.85.

Identifying Your Current Assets

Your assets aren’t just the money in your checking account. To get an accurate count, you must include three main categories:

- Cash and cash equivalents: This is your most liquid capital, including petty cash and short-term market funds.

- Accounts Receivable: This is money customers owe you. Be realistic here; if an invoice is 120 days past due, it might be bad debt rather than a reliable asset.

- Inventory: For a retail business, this includes products on shelves. For a service business, it includes raw materials or parts waiting to be used in a job.

Tallying Your Current Liabilities

Liabilities are the financial obligations you must settle within the next year. Keeping these organized prevents cash flow bottlenecks.

- Accounts Payable: These are the standard bills you owe to vendors and suppliers for goods or services already received.

- Short-term debt: Include any credit line balances or the portion of a long-term loan that’s due within the next 12 months.

- Accrued expenses: These are costs you’ve incurred but haven’t paid yet, such as employee wages, rent, and quarterly tax payments.

If your calculation shows a gap that’s making it hard to take on new contracts, you can always explore your funding options to see how a quick injection of capital could smooth out your seasonal dips.

The Working Capital Cycle: Identifying Where Your Cash Gets Stuck

Think of your cash flow as a loop rather than a straight line. The “Cash-to-Cash” cycle measures the exact number of days between the moment you pay for raw materials and the moment your customer’s payment finally hits your bank account. If this loop is too wide, your business will feel a constant squeeze. A 2023 study by PwC revealed that the average cycle for global companies reached its longest point in five years, stretching to roughly 72 days. That’s over two months where your money is “out of office” and unavailable for growth.

The length of this cycle depends heavily on what you do. A local bakery might have a cycle of 24 hours because they sell what they bake immediately. A custom furniture manufacturer, however, might wait 120 days from buying timber to receiving a final check. If you’re in the SaaS world, you might even enjoy a negative cycle by collecting annual payments upfront. Understanding your specific industry benchmark is the first step to identifying where your working capital is actually hiding.

The Inventory Lag

Dead stock is more than just a warehouse headache; it’s frozen money. Every pallet of unsold goods represents capital you can’t use for payroll or new equipment. Industry data suggests that the “carrying cost” of inventory, which includes insurance, taxes, and storage fees, can range from 25% to 30% of the inventory’s total value annually. You can tighten this by adopting just-in-time (JIT) ordering. This strategy requires tight coordination with vendors but ensures you aren’t over-buying. If you’re currently sitting on slow-moving items, it’s often better to run a steep discount sale to liquefy that cash rather than letting it rot on a shelf.

The Accounts Receivable Bottleneck

A sale isn’t a sale until the money is in the bank. If you’re offering Net-60 terms to your clients, you’re effectively acting as their bank by providing an interest-free loan. This is a common trap. A 2024 survey of small business owners showed that 43% of firms struggle with late payments, which directly stalls their ability to reinvest. To speed up the cycle, try offering a “2/10 net 30” discount. This gives customers a 2% price break if they pay within 10 days. It’s a small trade-off to get your cash back weeks earlier. If you find that these gaps are still making it hard to cover daily costs, a business line of credit can serve as a flexible bridge while you wait for those invoices to settle.

Practical Strategies to Optimise Your Internal Cash Flow

Before you look at external financing, look closely at your internal operations. Many businesses sit on locked cash without realizing it. Efficiency isn’t just about cutting costs; it’s about making your working capital move faster through your business cycle. If you can shorten the time it takes to turn inventory into cash, you reduce your reliance on debt. This approach keeps your business lean and improves your bottom line without adding interest expenses.

Start with your inventory management. Overstocking is a common trap that drains liquidity. A 2023 report by the IHL Group found that inventory distortion, including overstocking and out-of-stocks, costs retailers nearly $1.77 trillion globally. Using data-driven ordering ensures you aren’t tying up thousands of dollars in products that sit on shelves for months. Aim for a higher turnover rate to keep your cash liquid and ready for immediate needs.

Mastering Your Receivables

Waiting for clients to pay is a major bottleneck. You can’t pay your own bills with an unpaid invoice. Automating follow-ups is an easy win. Software sends reminders automatically, saving you hours of manual work. Reducing friction helps too. Offering digital payment options often leads to faster settlements than traditional checks. For larger projects, always require a 25% deposit or milestone payments to keep cash moving throughout the job.

Managing Your Payables Strategically

Don’t pay your bills earlier than necessary. If a vendor gives you 30 days, pay on day 29. This keeps cash in your account longer for emergencies. Strong vendor relationships are vital. Most suppliers will extend terms to 45 days during slow months if you’ve been a consistent partner. Always identify which bills are critical, like payroll, and which have flexible windows that won’t result in late fees or credit damage.

Optimizing these internal levers creates a more resilient foundation. When you do decide to scale, you’ll be doing it from a position of strength rather than necessity. If you’ve tightened your processes and still see a gap for a major growth opportunity, you can prequalify for business funding to see what options fit your improved working capital profile.

Strategic Funding: Using External Capital to Fuel Business Growth

Internal optimization has its limits. Even if you’ve mastered your inventory and shortened your collection cycle, external factors can strain your cash flow. A 12% increase in raw material costs or a sudden opportunity to acquire a competitor can happen faster than your bank account can keep up. Strategic funding isn’t an emergency fix for poor management. It’s a growth tool. Using external capital allows you to keep your working capital liquid while you pursue high-ROI projects that would otherwise be out of reach.

Kredline functions as a comprehensive marketplace, removing the need to spend hours visiting different banks. You get to compare diverse products in one place, which saves time and stress. One of the biggest advantages is the ability to prequalify. This step allows you to see your actual options and estimated rates without any impact on your credit score. It’s about having information before you make a commitment, ensuring you choose the right partner for your specific situation.

Flexible Funding Tools for Working Capital

A flexible business line of credit acts as an on-demand safety net. You don’t pay for it until you use it; this makes it perfect for covering payroll during an unexpected slow week. If you’re looking at a specific, time-bound project like a 90-day inventory build-up for the holiday season, short-term business loans provide the necessary lump sum. For businesses with fluctuating monthly income, revenue-based financing is often the best fit. It adjusts your repayment amounts based on how much you actually earn, protecting your cash flow during leaner months.

Bridging Gaps with Merchant Cash Advances

A merchant cash advance (MCA) is designed for businesses with high daily credit card sales, such as cafes or retail shops. It’s a fast way to get capital because it’s based on your sales history rather than just a traditional credit score. This makes it accessible for owners who might have been turned away by traditional lenders due to less-than-perfect credit. It’s a practical way to manage working capital when speed is your top priority. You can prequalify for business funding online to see your specific rates and terms without the usual bank red tape.

Turning Your Cash Flow into a Competitive Edge in 2026

Managing your daily operations requires more than just keeping an eye on a bank balance. It’s about understanding how working capital keeps the lights on while you wait for invoices to clear. Most businesses face hurdles when cash gets trapped in inventory or unpaid bills. By tightening your collection processes and negotiating better terms with vendors, you can free up the liquidity needed to handle seasonal dips or sudden payroll demands. These small shifts in your cash cycle often create the breathing room necessary for long-term stability.

Sometimes internal adjustments aren’t enough to cover a major equipment purchase or a rapid expansion phase. You don’t have to navigate these financial hurdles alone or settle for rigid bank terms that don’t fit your reality. Whether you’re dealing with bad credit or lack traditional collateral, specialized solutions exist to keep your momentum going. You can access a network of 50+ third-party providers through a simple online application that avoids the typical personal loan pressure.

Explore your funding options and prequalify with Kredline today to see how a tailored approach can support your business goals. You’ve built the foundation; now it’s time to ensure you have the resources to grow.

Frequently Asked Questions

What is a good working capital ratio for a small business?

A healthy working capital ratio typically falls between 1.2 and 2.0. This range suggests your business has enough liquid assets to cover short-term liabilities without leaving too much cash sitting idle. If your ratio drops below 1.0, you might struggle to pay immediate bills. Conversely, a ratio above 2.0 often means you’re being too conservative and missing growth opportunities.

Is negative working capital always a sign of a failing business?

Negative figures aren’t always a death sentence for a company. High-turnover businesses like grocery stores or restaurants often operate this way because they collect cash from customers before paying their suppliers. However, for most service or manufacturing firms, it indicates a liquidity crunch. You should check if your specific business model naturally supports this before worrying about insolvency.

How is working capital different from monthly cash flow?

Working capital measures your financial health at a specific moment by subtracting current liabilities from current assets. Monthly cash flow tracks the actual movement of money in and out of your accounts over a 30 day period. Think of it this way; cash flow is the fuel moving through the engine, while the other figure is the total amount of fuel you have in the tank right now.

Can I get a working capital loan if I have bad credit?

You can still secure funding with a credit score below 600 through alternative lenders. These providers often prioritize your business’s monthly revenue and time in operation over your personal credit history. While interest rates might be higher, it’s a viable way to bridge gaps. Kredline can help you navigate these specialized options to find a fit that won’t strain your daily operations.

What are the main causes of a working capital shortage?

A working capital shortage often stems from a mismatch between when you pay expenses and when customers pay you. Late-paying clients on 60 or 90 day terms are a primary culprit for many small firms. Rapid expansion also eats up cash quickly because you’re spending on labor and materials before the new revenue arrives. Managing these gaps is essential to keeping the business stable.

How often should a business owner calculate their working capital?

You should calculate this figure at the end of every month when you close your books. Monitoring it monthly allows you to spot downward trends before they become emergencies. If your business is seasonal, you might even check it weekly during peak periods. Regular reviews help you decide when it’s time to seek outside funding or tighten up your collections process.

Will taking out a loan for working capital hurt my business in the long run?

Taking a loan won’t hurt your business if you use the funds to generate more revenue than the cost of the interest. It’s a strategic tool for managing timing gaps or buying inventory in bulk at a discount. Debt only becomes a problem when it’s used to cover permanent losses rather than temporary cash flow hurdles. Used correctly, it provides the breathing room needed for steady growth.

What is the difference between an SBA 7(a) loan and a merchant cash advance?

An SBA 7(a) loan is a government-backed bank loan with low interest rates and repayment terms up to 10 years. A merchant cash advance isn’t a loan but an advance on your future sales, usually repaid daily or weekly over 3 to 12 months. While SBA loans take weeks to process, advances can be funded in 24 hours. Each serves a different urgency and financial need.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.