What if your loan payment actually shrank during your slowest month of the year? Most business owners feel the pressure of rigid bank schedules, especially since 82% of small firms struggle with cash flow management at some point. You likely agree that a fixed monthly bill feels particularly heavy when your seasonal sales take a dip. It’s a stressful cycle that often makes revenue-based financing a more attractive, flexible alternative to traditional debt.

You’re about to learn how to secure capital that scales with your sales, allowing you to grow without giving up equity or risking your personal home as collateral. We’ll show you how to access fast funds that protect your ownership while providing a predictable cost of capital. This guide covers everything from qualification requirements to the specific ways this model supports business growth as we move into 2026.

Key Takeaways

- Discover how to access growth capital that adjusts to your monthly sales, allowing you to scale without giving up ownership or personal assets.

- Learn the mechanics of revenue-based financing, including how a factor rate differs from traditional interest and why it offers more predictability for cash-flow-heavy businesses.

- Compare the speed and flexibility of RBF against traditional bank loans and MCAs to identify the most cost-effective “middle ground” for your specific needs.

- Determine if your business is ready by reviewing the “Golden Rule” of gross margins and the specific revenue benchmarks required to secure funding.

- Find out how to navigate the lending marketplace safely to avoid common traps like debt stacking while using Kredline to explore your prequalification options.

What is Revenue-Based Financing and Why is it Trending in 2026?

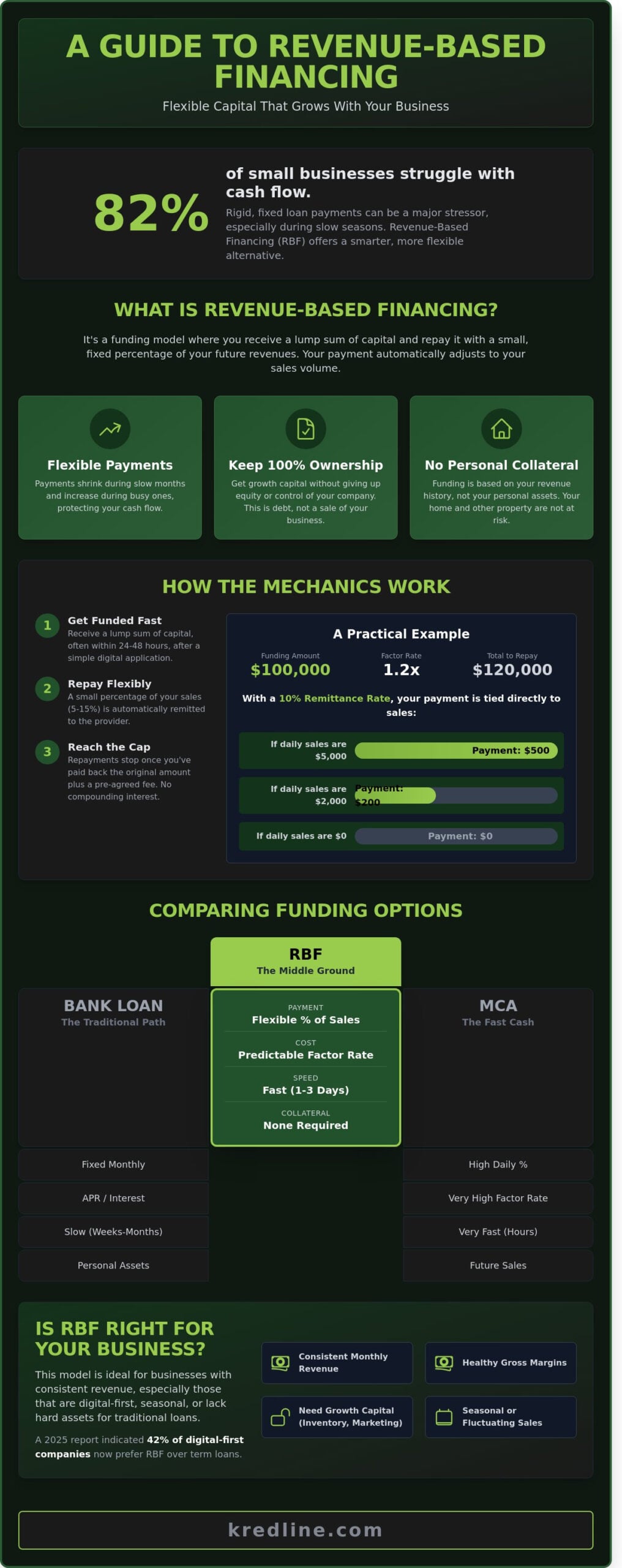

Revenue-based financing is a funding model where capital is repaid as a small percentage of your future gross revenues. It is a straightforward setup. You receive a lump sum upfront, and instead of a fixed monthly bill, you pay back a slice of what you actually earn. This model, often called revenue-based financing, has become a go-to for modern companies that do not fit the old-school bank mold. By 2026, the market has seen a massive shift away from debt-heavy capital. High interest rates and rigid bank terms in 2024 and 2025 forced many owners to look for more revenue-aligned options. A 2025 industry report indicated that 42% of digital-first companies—including those using fintech tools like Pallapay to manage digital assets—now prefer this model over traditional term loans.

If your sales drop during a quiet month, your payment shrinks automatically. This protects your operational runway when you need it most. It is especially popular for businesses that lack traditional collateral like real estate or heavy machinery. If your primary asset is your monthly recurring revenue or daily digital sales, this fits your reality better than a mortgage-style loan. Many service-based businesses or online retailers don’t have a warehouse to pledge to a bank. For them, RBF turns their consistent sales history into their most valuable leverage.

The Core Difference: Growth Capital vs. Traditional Debt

Fixed installments can be a death trap for seasonal businesses. A landscaping company or a retail boutique shouldn’t have to pay the same amount in a slow January as they do in a busy June. Traditional bank loans are transactional; the bank wants their check regardless of your cash flow. RBF feels more like a partnership. When you succeed, the repayment accelerates. When things slow down, the pressure eases. Revenue-based financing is a non-dilutive alternative to equity.

Non-Dilutive Funding: Keeping 100% of Your Business

Many owners are choosing RBF over venture capital or angel investors because they want to keep 100% of their business. Selling equity means giving up a piece of every future dollar you earn. It also means bringing in voices that might not share your long-term vision. With RBF, you get the cash to scale, but you maintain total control. It is an effective way to bridge the gap between early-stage growth and mid-market success. You can explore revenue-based financing options to see how this flexibility helps you reach the next level without bringing in outside board members. This approach allows you to focus on managing working capital and meeting payroll without the stress of diluting your ownership before a major exit or expansion phase.

The Mechanics: How Revenue-Based Financing Actually Works

Revenue-based financing doesn’t operate like a traditional bank loan with fixed monthly installments. It’s a structure where a funding provider purchases a specific percentage of your future sales. The process is streamlined and digital. Most providers use secure bank integrations, like Plaid or Wealthreader, or connect directly to your merchant account to verify your cash flow history. This real-time data allows them to skip the weeks of paperwork typically required by legacy banks. Once the data is analyzed, you receive a lump sum of capital, often within 24 to 48 hours.

The repayment happens automatically. Every day or week, a small percentage of your sales is diverted to the provider. This continues until you hit a predetermined total amount. If your sales slow down, the amount you pay back that week also drops. This flexibility is what makes revenue-based financing a popular choice for businesses with fluctuating seasonal demand.

Understanding the Repayment Cap and Percentage

Instead of an interest rate that compounds over time, this model uses a “factor rate” to determine the total cost of capital. For example, if you receive $100,000 with a 1.2x repayment cap, you’ll pay back exactly $120,000. There’s no guessing game. You know the total cost from day one. The speed at which you pay it back depends on your “remittance rate,” which usually ranges from 5% to 15% of your gross sales.

- The $100,000 Example: If your remittance rate is 10% and you make $5,000 in sales on a Tuesday, $500 goes toward your balance.

- No Sales, No Stress: If you have a day with zero sales, you pay $0. There are no “late fees” in the traditional sense because the payment is tied to your actual performance.

- Margin-Based Rates: Providers set your percentage based on your profit margins to ensure the payments don’t choke your daily operations.

No Personal Collateral: A Lower-Risk Path to Growth?

One of the biggest reliefs for business owners is the lack of personal collateral. Unlike many short-term business loans that might require a personal guarantee or a lien on your home, these providers focus on the business’s health. They typically file a UCC-1 statement, which is a legal notice showing they have an interest in the business’s assets, but your personal property stays off the table.

Risk assessment is based on your sales history and consistency rather than just a personal credit score. This allows companies with strong revenue but less-than-perfect credit to access the capital they need. If you’re curious how these numbers look for your specific monthly volume, you can prequalify for business funding to see your options without a hard credit pull. It’s a straightforward way to see if your current sales volume supports the growth you’re planning.

Comparing Your Options: RBF vs. MCA vs. Traditional Term Loans

Choosing the right capital for your business depends on how fast you need the cash and what you’re willing to pay for that speed. Revenue-based financing often serves as the middle ground for growing companies. It offers more flexibility than a rigid bank loan but is generally more affordable and sustainable than a quick cash advance. Understanding how these models stack up helps you avoid overpaying for capital you don’t need or getting stuck with a payment you can’t afford.

- Traditional Term Loans: Best for long-term stability. They offer the lowest interest rates but require high credit scores and weeks of paperwork.

- Merchant Cash Advances (MCA): Best for emergencies. These are the fastest to fund, often within 24 hours, but they carry the highest costs and daily repayment schedules.

- Revenue-Based Financing: Best for growth. It scales with your sales, providing a balance of speed (3 to 7 days) and cost without requiring personal collateral.

Revenue-Based Financing vs. Merchant Cash Advances (MCA)

It’s easy to confuse these two because both use a “factor rate” instead of a traditional interest rate. However, the source of repayment is the big differentiator. A merchant cash advance (MCA) specifically targets your credit card sales. If you’re a B2B company that gets paid via wire transfer or ACH, an MCA might not even be an option for you. Revenue-based financing looks at your total gross revenue, including invoices and direct deposits. This makes it a much better fit for SaaS companies or service providers. RBF also tends to have longer repayment windows, whereas many MCAs demand full repayment within 3 to 9 months, which can squeeze your daily cash flow.

When a Traditional Loan Still Makes Sense

While RBF is great for marketing or hiring, it isn’t always the cheapest way to buy “hard” assets. If you’re looking to purchase a warehouse or heavy machinery, a bank or specialized equipment funding is usually the smarter move. These loans often come with 5 to 10 year terms and fixed interest rates that are lower than the cost of RBF over the same period. Many successful owners build a “funding stack” where they use a bank loan for their foundation and RBF to fuel their seasonal spikes or inventory needs.

The impact on your balance sheet is another factor to consider. Traditional loans are recorded as debt, which can affect your ability to get other financing. RBF is often structured as a purchase of future receivables. This can keep your debt-to-income ratio looking healthier. Since most RBF providers don’t report to personal credit bureaus unless there’s a default, it protects your personal credit score while you focus on scaling the business.

Is Your Business a Candidate for Revenue-Based Funding?

Revenue-based financing isn’t a one-size-fits-all solution. It’s a specialized tool designed for companies that already have a proven sales engine but need fuel to move faster. Unlike traditional bank loans that focus heavily on your personal credit score or collateral, this model prioritizes your monthly bank statements and the health of your cash flow.

To qualify, your business typically needs at least 6 months of operating history. Most providers look for a minimum of $10,000 in consistent monthly revenue. If your sales are erratic or trending downward, you’ll likely face a rejection. Lenders view declining revenue as a sign of a struggling business model, which makes the risk too high for a percentage-based repayment structure.

The “Golden Rule” for this type of funding is maintaining high gross margins. Because you’re paying back the capital as a percentage of your top-line revenue, your margins must be thick enough to cover the repayment and your operating costs simultaneously. If your profit margins are razor-thin, the repayment could accidentally choke your daily operations.

The Ideal Profile: High Margins and Consistent Cash Flow

Service-based businesses and SaaS companies often find revenue-based financing easier to manage than traditional retail. This is because they don’t have the heavy overhead of physical goods, allowing them to absorb the factor rate without hurting their bottom line. Predictability is your best friend here. If you can show that your revenue stays steady or grows month-over-month, you’re in a much better position to negotiate favorable terms.

It’s best to use RBF specifically for revenue-generating activities that offer a clear path to growth. Healthcare practices and professional service firms use this to bridge the gap while waiting for insurance payouts or large contract settlements. They have the “predictability” lenders love, even if the cash isn’t in the bank account this exact second.

Common Use Cases: From Inventory to Digital Marketing

The most successful applications of this funding involve clear ROI. For instance, an e-commerce brand might face a massive spike in demand before the holiday season. If they know a $40,000 investment in inventory will generate $120,000 in sales within 60 days, the cost of the funding becomes a minor line item compared to the profit. It’s about using the capital to catch a wave you’re already riding.

- Digital Marketing: Funding a proven ad campaign where every dollar spent reliably returns three dollars in sales; to scale your efforts, check out CreativesConvert for automated ad design.

- Seasonal Hiring: Bringing on extra staff to handle a documented surge in contract work.

- Equipment Upgrades: Replacing a piece of machinery that directly increases your daily output.

You can review the specific requirements for revenue-based financing to see how your current numbers align with industry standards. If your ROI is expected to exceed the factor rate, it’s a logical move for scaling without debt traps.

Wondering if your monthly sales volume qualifies you for a growth injection? Prequalify for funding in minutes to see your options.

Navigating the Marketplace: Finding the Right Provider via Kredline

The alternative lending market often feels like a digital wild west. While 32 percent of small businesses turned to online lenders last year, many found themselves lost in a sea of fine print and aggressive sales tactics. Finding the right partner isn’t just about getting the money. It’s about ensuring the terms don’t strangle your daily operations. You need to watch out for “stacking,” which is the dangerous practice of taking out a second or third funding product before the first is repaid. This often leads to a debt spiral that consumes 50 percent or more of a company’s daily receipts, leaving little room for payroll or inventory.

When you review a contract, look past the initial offer. You should hunt for hidden origination fees or “administrative” charges that can quietly tack on thousands to your total cost. A transparent contract should also clearly outline prepayment discounts. Some providers offer a “buyout” option that reduces the total payback amount if you settle the balance early. If a lender isn’t willing to show you the total cost of capital upfront, it’s usually a sign to walk away.

Why Working with a Broker Beats Going Direct

Approaching lenders individually is time consuming and risky. Kredline acts as a protective filter, vetting third-party providers to weed out predatory actors who hide high costs in complex language. By using a broker, you create a competitive environment. When multiple lenders see your application, they often sharpen their pencils to offer better rates to win your business. This process helps you manage cash flow effectively without the stress of managing dozens of different conversations. It’s about having a partner who understands that your focus should be on your customers, not on chasing paperwork.

The Simple Path to Prequalification

Traditional bank loans often require three years of tax returns and months of waiting. Most revenue-based financing providers through Kredline only ask for recent bank statements to verify your sales history. This streamlined approach means you can move from a simple application to cash in your bank account in as little as 24 to 48 hours. It’s the speed your business needs when a growth opportunity or an unexpected expense arises.

Because revenue-based financing is tied to your sales, the process is built for speed rather than bureaucratic hurdles. You don’t need to spend weeks preparing balance sheets or collateral appraisals. You can prequalify for business funding today to see which options fit your current revenue model and growth goals.

Ready to Scale on Your Own Terms?

Running a business in 2026 requires a level of agility that traditional bank loans simply can’t match. You’ve seen how revenue-based financing aligns your repayment schedule with your actual sales volume, ensuring your cash flow stays healthy even during slower months. Unlike rigid term loans or high-risk personal debt, this model protects your personal assets while giving you the capital needed to bridge invoice gaps or stock up for seasonal peaks.

Kredline helps you navigate this landscape by providing access to a network of top-tier third-party providers. We focus 100% on business funding, so you don’t have to worry about the complexities of personal loans. You get flexible capital with no fixed monthly payments, letting you focus on operations instead of looming debt deadlines. Whether you’re upgrading equipment or expanding your team, finding the right fit shouldn’t be a source of stress. Our goal is to make the process as straightforward as possible.

Explore your funding options and prequalify in minutes to see what’s possible for your company’s next chapter. You’ve built something great; now it’s time to give it the room it needs to grow.

Frequently Asked Questions

Is revenue-based financing a loan?

Technically, it isn’t a traditional loan. It’s a purchase of a fixed percentage of your future gross revenue. Unlike a bank loan that requires a set monthly payment regardless of your performance, this structure adjusts to your cash flow. It doesn’t typically appear as debt on your balance sheet, which helps keep your financial ratios healthy for future needs.

How does revenue-based financing differ from a Merchant Cash Advance?

The main difference lies in the repayment source and timeframe. A Merchant Cash Advance usually takes a daily cut of your credit card sales, while revenue-based financing looks at your total monthly gross revenue. Most revenue-based agreements span 12 to 36 months, offering a more sustainable pace than the 3 to 9 month windows common with cash advances.

Will revenue-based financing affect my personal credit score?

It won’t usually impact your personal credit because the funding is tied to your business’s performance. Providers focus on your monthly bank statements and consistent revenue history rather than your personal FICO score. You can use Kredline to explore these options without the stress of a hard credit pull affecting your personal standing.

Can I pay off a revenue-based financing agreement early?

You can settle the balance at any time, but it doesn’t always reduce the total cost. Since you agree to pay back a fixed multiple of the original amount, the total price is set from day one. Some agreements include a 10% or 15% discount if you pay the full amount within the first 6 months, so it’s always smart to check your specific terms.

What happens if my business has a month with zero revenue?

If your revenue drops to zero, your payment for that month is also zero. This flexibility is built into the contract to protect your cash flow during seasonal dips or unexpected pauses. You aren’t penalized for a slow month; the repayment period simply extends until the total agreed-upon amount is fully paid back through future sales.

Do I need to provide collateral for revenue-based financing?

No, you don’t need to put up your house, equipment, or inventory as security. The funding is unsecured because the provider is buying a share of your future sales. This makes revenue-based financing a great fit for service-based businesses or software companies that lack the physical assets traditional banks usually demand for a secured line of credit.

How much does revenue-based financing typically cost?

The cost is calculated as a total repayment multiple, which typically ranges from 1.1x to 1.3x of the funded amount. If you take $50,000, you might pay back $60,000 over time. Industry data from 2023 shows these costs are often higher than a standard bank loan but significantly cheaper than selling 10% or 20% of your company’s equity to an investor.

What industries are best suited for revenue-based funding?

SaaS companies and subscription-based businesses are the strongest candidates because they have predictable, recurring income. E-commerce brands with at least 6 months of steady sales history also use this to fund inventory. It’s less effective for businesses with very low profit margins, such as some grocery retail, or companies that rely on infrequent, large project payments.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.