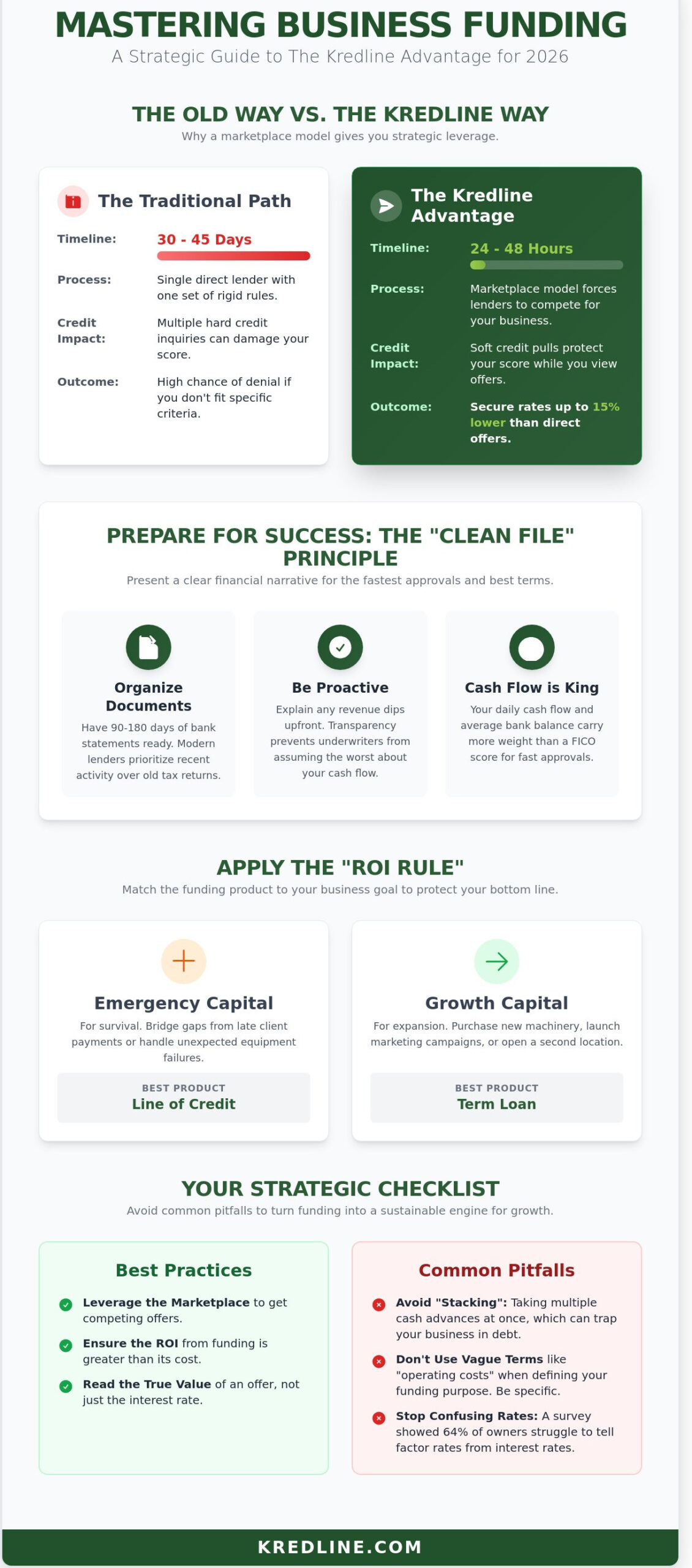

A 2025 survey of small business owners revealed that 64% of entrepreneurs still struggle to differentiate between factor rates and interest rates, often leading to unexpected hits to their daily cash flow. It’s frustrating when you need capital to bridge an invoice gap or hire a new team member, but the traditional banking system expects you to wait 30 days for a decision. You shouldn’t have to choose between immediate growth and long-term financial clarity. Understanding the best practices for Kredline allows you to move past these hurdles and treat funding as a strategic tool rather than a source of stress.

In this article, you’ll learn exactly how to secure capital in as little as 24 hours while keeping your repayment terms transparent. We’ll break down how to compare marketplace offers effectively, avoid common debt traps, and turn a quick line of credit into a sustainable engine for your company’s expansion throughout 2026.

Key Takeaways

- Understand why a marketplace model offers more leverage than a direct lender when navigating the modern funding landscape.

- Learn how to implement the “Clean File” principle and organize your bank statements for the fastest possible approval and better terms.

- Apply the “ROI Rule” to ensure the cost of capital remains lower than the profit it generates, protecting your bottom line.

- Master the best practices for Kredline by avoiding common pitfalls like “stacking” and learning to read the true value of a funding offer.

- Discover the roadmap for transitioning from temporary bridge funding to long-term expansion capital as your business scales.

Navigating the Kredline Marketplace: Why a Strategic Approach Matters

Securing capital in 2026 requires more than just a solid balance sheet; it demands a tactical mindset. Most business owners mistake a financial marketplace for a traditional direct lender. This is a critical distinction. A direct lender has one set of rules and one bucket of money. If you don’t fit their specific criteria, your application dies there. Kredline operates as a marketplace, which functions more like a high-tech broker. This model gives you significant leverage by forcing multiple third-party lenders to compete for your business.

Speed is the other major factor. Traditional bank cycles often stretch between 30 and 45 days. In a fast-moving economy, waiting six weeks for a decision can mean missing out on a bulk inventory discount or losing a key contract. One of the Best practices for Kredline is to use the platform’s speed to bypass these archaic timelines. Many users find they can move from application to funding in as little as 24 to 48 hours, provided they have their documentation ready.

Before you start the prequalify for business funding process, you need a clear roadmap. Entering a marketplace without a specific goal is like walking into a hardware store without a project in mind; you might walk out with something, but it probably won’t be what you actually need. Defining your objectives early keeps you in control of the conversation with potential lenders.

The Marketplace Advantage for Small Businesses

The primary benefit of a marketplace is efficiency. You fill out one application to access a network of providers, rather than spending 20 hours on individual submissions. This competition is your best friend. Since 2024, industry data has shown that businesses using marketplace models often secure rates up to 15% lower than those who settle for the first offer from their local bank. Additionally, Kredline helps protect your credit profile. By using a centralized system, you can often see potential offers through soft credit pulls, which don’t damage your score the way multiple hard inquiries would.

Defining Your Funding Purpose

Lenders in 2026 value precision over generalities. If you request $100,000 for “operating costs,” you’re a higher risk than someone requesting $100,000 for “purchasing a CNC machine with a 3-year ROI.” A fundamental understanding corporate finance will help you distinguish between two main categories:

- Emergency Capital: This is for survival. It bridges the gap when a major client is 60 days late on an invoice or an HVAC system fails in mid-July.

- Growth Capital: This is for expansion. It’s used for things like equipment funding or opening a second location.

One of the Best practices for Kredline is matching the urgency of your situation to the right financial product. Short-term gaps are best handled by lines of credit, while long-term investments deserve the stability of a term loan. Knowing your “why” ensures you don’t pay “emergency” interest rates for a “growth” project.

Preparing Your Business for Fast Approval and Better Terms

Speed is the currency of 2026. Lenders want a “Clean File,” which means your data should be ready for an algorithm or an underwriter to digest in minutes. One of the best practices for Kredline is presenting a narrative that makes sense at a glance. When your files are scattered or incomplete, it creates friction that leads to higher interest rates or flat denials. You want to show that you’re in control of your numbers from the first click.

Bank statements are the heartbeat of your application. While traditional SBA loan programs often require years of tax returns and personal financial statements, modern alternative lenders focus on the last 90 to 180 days of activity. They want to see how money moves through your business right now. If your revenue dropped by 25% last October because you were renovating your storefront, explain that upfront. Proactive transparency prevents an underwriter from assuming the worst about a temporary dip.

Don’t let a sub-680 credit score discourage you. In the current funding environment, your daily cash flow and average bank balance carry more weight than a FICO score. Lenders are more interested in your ability to manage a weekly payment than a mistake you made three years ago. Highlighting these strengths is a core part of the best practices for Kredline users who want to secure competitive terms despite a less-than-perfect credit history.

Organizing Your Financial Documentation

Keep the last 4 to 6 months of business bank statements in a single, organized digital folder. Your Profit and Loss (P&L) statement needs to reflect your current operational health, not just your status from the previous tax year. Digital, high-resolution records allow underwriting software to verify your data in seconds. This speed often results in a faster “yes” and lower administrative fees because the lender spends less time chasing paperwork.

Positioning Your Cash Flow

Lenders scrutinize your ending daily balance to ensure you have the capacity for repayment. If your balance frequently dips below $1,000, it signals a liquidity risk. You can offset this by identifying seasonal peaks, like a 35% revenue surge during the summer months. Highlighting “guaranteed” future income, such as signed purchase orders or recurring service contracts, provides the security lenders need to offer higher funding amounts. If you want to see what your business qualifies for today, you can prequalify for business funding to get a clear picture of your options.

Matching the Right Funding Product to Your Business Cycle

Every business follows a unique rhythm. A retail shop might see 40% of its annual revenue in December, while a construction firm waits 90 days for a single project payment. One of the best practices for Kredline clients is recognizing that the “cheapest” capital isn’t always the most effective. You have to weigh three factors: speed, cost, and flexibility. If you need $20,000 for a flash inventory sale that expires in 48 hours, a high-speed option is better than a slow, low-interest bank loan that takes six weeks to process.

The “ROI Rule” should guide every decision you make. Before signing any agreement, ensure the cost of the capital is significantly lower than the profit it will generate. For example, if borrowing $50,000 costs you $7,000 in fees but allows you to fulfill a contract worth $15,000 in net profit, you’ve gained $8,000. If the math doesn’t result in a clear surplus, it’s not the right time to borrow. To get these projections right, many owners refer to the SBA’s guide to writing a business plan, which helps map out the financial impact of new capital.

When to Choose Revenue-Based Options

If your sales fluctuate, revenue-based financing offers a safety net. Instead of a fixed monthly payment that might crush you during a slow July, your payments adjust based on your actual sales volume. A merchant cash advance works similarly for businesses with high credit card volume, like restaurants or boutiques. These products use a “factor rate” rather than a traditional APR. A factor rate of 1.2 on a $10,000 advance means you pay back $12,000. It’s straightforward, fast, and doesn’t require the same collateral as a bank loan.

Leveraging Lines of Credit and Term Loans

A business line of credit is the ultimate tool for recurring gaps. Think of it as a safety net for payroll or utility spikes. You only pay interest on what you actually draw, making it a flexible part of the best practices for Kredline management. If you have a specific, one-time project with a clear end date, a short-term business loan provides the lump sum you need with a predictable repayment schedule.

When you need new hardware or vehicles, don’t drain your cash reserves. Using equipment funding allows the machinery to pay for itself over time. This preserves your liquid working capital for emergencies or unexpected opportunities, ensuring your daily operations never skip a beat while you upgrade your capabilities.

Evaluating Offers and Integrating Repayments into Operations

Receiving a funding offer is an exciting milestone, but the numbers require a careful look before you sign. A common mistake is focusing only on the total amount deposited into your account. You need to look at the daily or weekly impact on your bank balance. One of the best practices for Kredline clients is to treat the funding offer as a math problem rather than a windfall. Your Kredline advisor is there to help you walk through these figures, so don’t hesitate to ask for a breakdown of the total payback amount versus the net funding you receive.

Avoid the temptation of “stacking,” which happens when a business owner takes out multiple advances from different providers at the same time. In late 2024, data indicated that businesses with three or more active advances were 45% more likely to face a cash flow crisis. Stacking creates a scenario where too much of your daily revenue is diverted to debt service, leaving you short on funds for essential costs like rent or payroll. It’s almost always better to finish one repayment cycle or seek an increase on an existing line than to layer multiple high-frequency payments.

- Review the Factor Rate: This tells you exactly how much you’ll pay back in total.

- Check the Disbursement: Confirm if fees are deducted upfront so you know the exact amount hitting your account.

- Schedule a Call: Use 15 minutes to talk to your advisor about how the repayment fits your specific sales cycle.

Decoding the True Cost of Capital

Understanding “cents on the dollar” is the clearest way to judge an offer. If you receive $50,000 and the total payback is $59,000, your cost is 18 cents for every dollar borrowed. You should also watch for origination fees, which typically range from 1% to 4% of the total amount. A 3% fee on $100,000 means you start with $97,000. When choosing between daily or weekly repayments, look at your revenue patterns. If your sales fluctuate wildly day-to-day, a weekly structure often provides more breathing room. Following these best practices for Kredline ensures you don’t overextend your liquid cash.

Managing Cash Flow Post-Funding

Once the capital is in your account, speed is your ally. Capital that sits idle still costs money, so you should use it for its intended purpose immediately. If you bought $30,000 in inventory to prepare for a seasonal surge, track the turnover rate of those specific goods. Set up automated ACH repayments to avoid the administrative burden of manual transfers. This automation also protects your reputation with lenders. By 2026, 82% of successful small businesses used automated tools to sync their repayments with their accounting software, reducing the risk of accidental overdrafts during slow weeks.

Ready to see what your business qualifies for without the guesswork? Prequalify for business funding today and speak with an advisor about your options.

Long-Term Growth: Scaling Your Business with Kredline

Growth isn’t a single event; it’s a sequence of well-timed financial moves. Many business owners start their journey using bridge funding to solve immediate needs, such as covering a $20,000 inventory gap or fixing a delivery truck. By 2026, the goal often shifts toward expansion capital. This involves larger sums, perhaps $250,000 or more, used to open a second location or launch a new product line. One of the best practices for Kredline users is to view every early repayment as a deposit into their future borrowing power.

Lenders in the Kredline marketplace reward consistency. When you maintain a clean repayment history over a six-month or twelve-month period, your internal risk profile improves. This data-driven trust often translates into 15% to 20% higher funding limits on your next round. You might also see factor rates drop or interest rates decrease by 2% to 3% as you prove your business is a reliable partner. Beyond direct funding, you should look at your merchant services. Optimizing how you process payments can save a high-volume retailer $500 to $1,000 in monthly fees, which directly boosts the cash flow lenders look for during underwriting.

Building a Funding Relationship

Working with a marketplace partner like Kredline offers a distinct advantage over one-off lenders. Because Kredline tracks your business growth and revenue trends over time, they can advocate for better terms on your behalf. This relationship becomes vital when you’re ready to transition from short-term debt to long-term stability. For instance, a strong history of revenue-based financing can serve as the primary evidence needed to qualify for SBA 7(a) working capital loans. These loans offer some of the most competitive rates in the industry, but they require the kind of documented financial health that Kredline helps you build.

Next Steps: Prequalifying for the Future

The smartest time to look for money is when you don’t desperately need it. Waiting until your bank account hits zero limits your options and increases your stress. The 5-minute prequalification process is designed to give you a clear view of your current standing without impacting your credit score. It’s a low-risk way to see what your business is worth in the eyes of a lender today.

By prequalifying for business funding early, you gain a benchmark for your 2026 financial roadmap. You can consult with an advisor to discuss whether a line of credit or a term loan fits your specific expansion goals. This proactive approach ensures that when a growth opportunity appears, you already have the capital ready to deploy. Following these best practices for Kredline turns funding from a source of anxiety into a strategic tool for scaling.

Fueling Your Next Strategic Move

Securing capital doesn’t have to be a source of constant stress for your team. The most successful business owners in 2026 treat funding as a proactive tool rather than a last resort. By organizing your documentation early and matching your funding to specific needs like seasonal inventory or equipment upgrades, you put your business in a position of strength. Following these best practices for Kredline helps you navigate a national network of 3rd-party lenders to find the right fit for your unique situation.

Whether you’re dealing with a low credit score or lack traditional collateral, there are specialized paths available to keep your operations moving forward. You don’t have to wait weeks for a bank’s decision. Many businesses see funds in their accounts in as little as 24 to 48 hours. It’s about making the marketplace work for you so you can focus on what actually matters: serving your customers and building a sustainable future. Your business deserves a partner that understands the pace of modern commerce.

See what your business qualifies for with Kredline’s 5-minute prequalification tool and take the guesswork out of your cash flow management. Your next phase of growth is closer than you think.

Frequently Asked Questions

How does Kredline differ from a traditional bank loan?

Kredline evaluates your business based on real-time cash flow and digital data rather than just physical collateral or five years of tax returns. While a traditional bank might take 45 days to process a stack of paperwork, the Kredline approach uses automated underwriting to provide a decision in under 24 hours. This makes it a more flexible partner for companies that need capital to move on a 48-hour inventory deal.

What is the minimum credit score required to use Kredline?

You don’t need a perfect 800 score to qualify, as most options require a minimum FICO of 550 to 600. One of the best practices for Kredline users is to focus on consistent monthly revenue of at least $10,000, which often carries more weight than a credit score alone. We look at the health of your three most recent bank statements to ensure the funding fits your actual repayment capacity.

Can I get funding if my business has seasonal revenue dips?

Seasonal fluctuations are common in industries like retail or landscaping, and our partners account for these three-month or six-month cycles. If your revenue drops by 40 percent in January but triples in June, we look at your total annual performance to determine eligibility. This ensures you have the capital to stock up before your peak season starts without being penalized for a quiet winter period.

How fast can I actually receive funds through Kredline?

Most businesses see funds hit their account within 24 to 48 hours after final approval. The process is built for speed, starting with a 15-minute application that connects directly to your business bank account. If you submit your documents by 10:00 AM on a Tuesday, it’s common to have the capital ready for use by Wednesday afternoon to cover payroll or a sudden equipment repair.

What is the difference between a factor rate and an interest rate?

A factor rate is a fixed decimal, like 1.2, that’s multiplied by your total loan amount to determine exactly what you’ll owe from day one. Unlike an annual interest rate that compounds over time, a factor rate doesn’t change if you take longer to pay. If you borrow $10,000 at a 1.15 factor rate, you’ll pay back exactly $11,500, making it easier to calculate your precise profit margins.

Is there a penalty for paying off my business funding early?

There are no hidden penalties for early repayment, and in many cases, you can actually save money on the total cost. Some funding structures offer a 10 percent to 20 percent discount on the remaining factor cost if you settle the balance ahead of schedule. We believe in rewarding businesses that grow faster than expected, so we keep the terms transparent and free of any exit fees.

Can I use Kredline if I already have an existing business loan?

You can still secure funding even if you have an active SBA loan or a bank line of credit. Following best practices for Kredline involves ensuring your total daily or weekly debt payments don’t exceed 15 percent of your average revenue. This second position funding is a common way for businesses to bridge a 30-day gap while waiting for a larger, long-term loan to close at their primary bank.

Does Kredline offer personal loans for small business owners?

Kredline focuses exclusively on commercial funding designed to support your company’s operations and growth. We don’t provide personal loans for individual expenses like home renovations or personal car purchases. By keeping the focus on business health, we’re able to offer higher capital amounts, often reaching $500,000, based on your company’s 12-month revenue history rather than your personal debt-to-income ratio.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.