What if waiting for a “better” economic cycle to upgrade your fleet or machinery is actually costing your business 15% more in lost efficiency than the current interest rate? Many owners hesitate because equipment financing rates in 2026 feel unpredictable and lenders often hide their true costs behind complex jargon. It’s stressful to worry that a massive down payment might drain your cash reserves right before a seasonal dip.

We understand that you need clarity, not a sales pitch. You’ve worked hard to build your company; you shouldn’t have to choose between growth and financial stability. This guide shows you how to find the most cost-effective path to new equipment without sacrificing your daily working capital. We’ll walk through current market benchmarks, explain how to avoid the trap of hidden fees, and look at ways to get your application approved in as little as 24 hours so your projects stay on track.

Key Takeaways

- Understand how the 2026 economic landscape shapes current equipment financing rates and why using the asset as collateral increases your borrowing power.

- Identify the specific credit and “time in business” benchmarks that allow you to move from high-cost tiers to prime lending rates.

- Compare the long-term tax advantages of equipment loans against the cash-flow flexibility offered by modern leasing structures.

- Learn how to prepare a “use of funds” statement that demonstrates clear ROI to secure more competitive offers from lenders.

- Discover why a human-first marketplace approach offers the flexibility and industry-specific insight that traditional banks often lack.

The State of Equipment Financing Rates in 2026

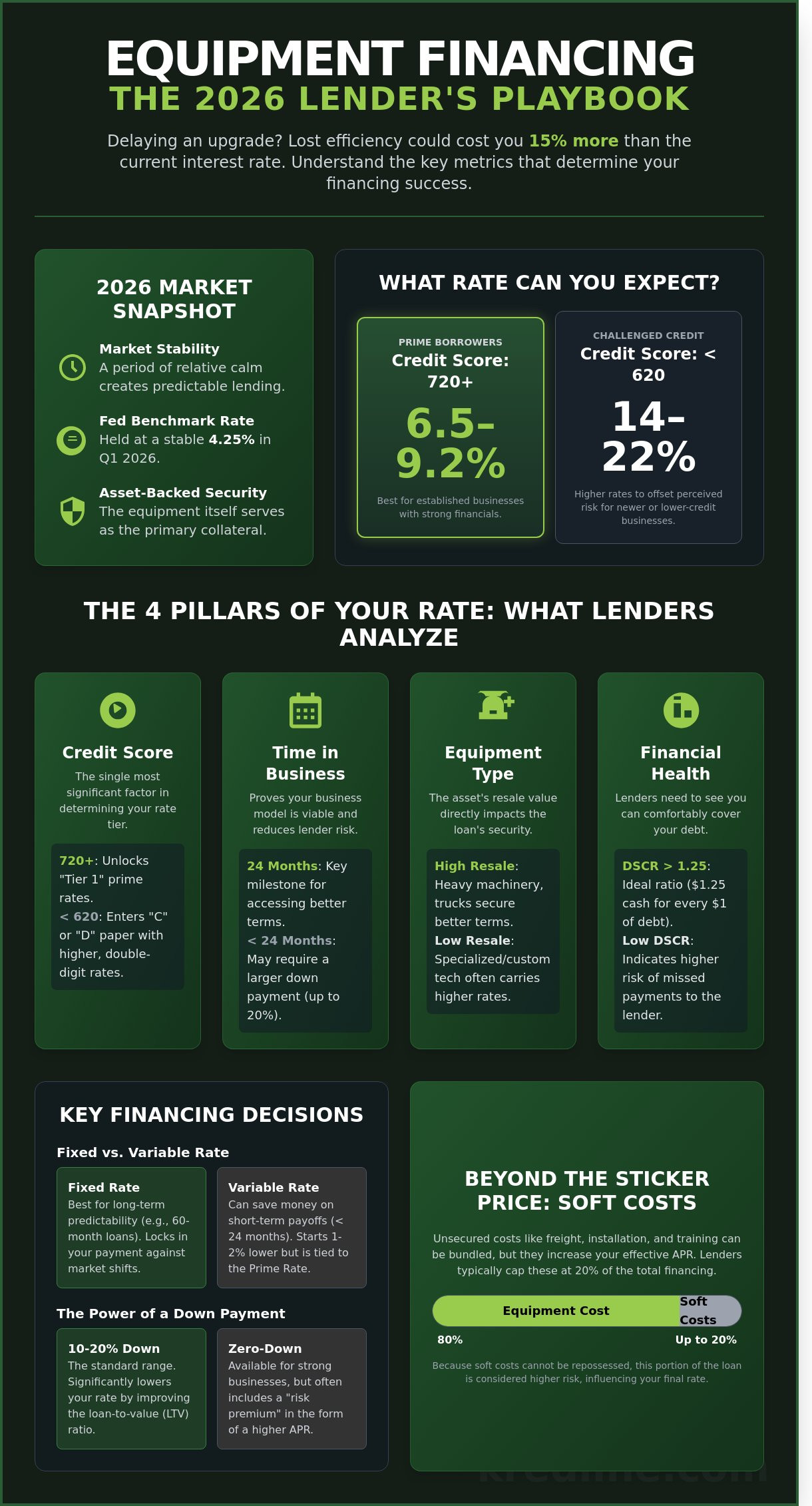

As we move through 2026, the lending market has finally reached a period of relative calm. The Federal Reserve held benchmark rates at 4.25% during the first quarter, providing a predictable foundation for commercial lending. This stability means equipment financing rates are more consistent than they were during the volatile shifts of 2024. Unlike a traditional term loan that might require a blanket lien on all your business assets, equipment financing is simpler. The machinery or vehicle you buy serves as the primary collateral for the debt.

Your specific rate depends heavily on your business’s financial health and the type of asset you’re purchasing. In the current climate, prime borrowers with credit scores above 720 can expect rates between 6.5% and 9.2%. For businesses with less established credit or those in “high-risk” industries, rates often scale between 14% and 22%. Lenders also weigh the equipment’s resale value. Heavy construction machinery often secures better terms than office technology because it retains its value longer on the secondary market.

Fixed vs. Variable Rates: Which is Right for You?

Fixed rates are the go-to for most small business owners in 2026. Knowing your exact payment for 60 months provides a safety net against future economic shifts. Variable rates might start 1% to 2% lower, but they’re tied to the Prime Rate. If you plan to pay off the equipment in under 24 months, a variable rate could save you money. However, for a long-term finance lease, the predictability of a fixed rate usually outweighs the initial savings of a floating one.

Understanding the Role of the Down Payment

A down payment isn’t just about reducing the loan amount; it’s a tool to lower your equipment financing rates. Most lenders look for a 10% to 20% contribution to offset their risk. This improves your loan-to-value (LTV) ratio, making you a more attractive candidate for lower interest brackets. Zero-down options are available for established companies with strong cash flow, but these often carry a “risk premium” in the form of higher annual percentages. If you want the most competitive terms, bringing some capital to the table is your best move. You can explore how your down payment affects your monthly costs by looking at equipment funding solutions tailored to your specific industry needs.

The Math Behind the Rate: What Lenders Are Really Looking At

Lenders don’t pull equipment financing rates out of thin air. They use a specific set of metrics to gauge how likely you are to pay them back. When you apply for funding, your business is essentially being put through a risk calculator that weighs your past performance against the value of the asset you want to buy. Understanding these variables helps you predict your equipment financing rates before you even apply.

- Credit Score: Your FICO score is the biggest lever in this process. Tier 1 borrowers, typically those with a 720 score or higher, usually secure the lowest rates, often staying within 2 to 3 percentage points of the prime rate. If your score sits below 620, you’re looking at credit-challenged “C” or “D” paper, where rates can jump into the double digits to offset the increased risk.

- Time in Business: Experience matters to a bank. Reaching the 24-month mark is a major milestone for most lenders. It proves your business model is viable. If you’ve been around for less than 24 months, expect to pay a premium or provide a larger down payment, sometimes as high as 20% of the equipment cost, to secure the deal.

- Equipment Type: The asset itself acts as collateral. A CNC machine or a heavy-duty truck has a high resale value, providing a safety net for the lender. If you default, they can sell the gear quickly. Specialized or custom-built machinery often carries higher rates because it’s harder to offload in a secondary market.

- Financial Statements: Lenders check your debt-to-income ratio and look for a Debt Service Coverage Ratio (DSCR) of at least 1.25. This means for every dollar of debt, you have $1.25 in cash flow to cover it. If your ratio is lower, the lender sees a higher risk of missed payments.

The Impact of “Soft Costs” on Your APR

Soft costs include things you can’t touch, like freight, installation, and staff training. Most lenders cap these at 20% of the total invoice. Since a lender can’t repossess “training hours” or “shipping fees” if you default, they see this portion of the loan as unsecured. This often pushes your effective APR higher than the base rate listed on the quote. To understand how these expenses factor into your long-term budget, you can consult this SBA guide to buying vs. leasing equipment. Including too many soft costs in one package can sometimes lead to a shorter repayment term to minimize the lender’s exposure.

Industry Risk Tiers

Lenders categorize businesses using NAICS codes to predict volatility. A restaurant might face a 2% higher rate than a medical practice for the exact same loan amount because the failure rate in food service is statistically higher. Industry risk functions as a direct percentage premium added to the base rate to compensate for the statistical volatility inherent in your specific business sector. If you want to see where your business stands, you can explore equipment funding options that match your industry profile and growth goals.

This risk assessment extends beyond just equipment financing. Industries deemed high-risk often face similar challenges when securing other essential business services, like payment processing. Finding a reliable partner is key, and companies like Merchant Solutions Corp specialize in providing these vital services to businesses that traditional providers may overlook.

Comparing Your Options: Loans, Leases, and Alternative Funding

Choosing the right structure is just as important as finding low equipment financing rates. A low rate won’t help if the repayment schedule chokes your monthly cash flow. You need to decide whether you want to own the asset eventually or simply pay for its use during its most productive years. Most business owners look at their 12-month projections before deciding which path to take.

Equipment loans work like a standard mortgage. You take ownership on day one, and the lender holds a lien on the asset. This is the best route if you plan to keep a machine for seven to ten years. It also unlocks Section 179 of the tax code, which allows many businesses to deduct the full purchase price of qualifying equipment in the year they buy it. In 2024, the deduction limit reached $1.22 million, and this incentive remains a cornerstone for profitable firms looking to reduce their tax liability. There are several reasons to finance equipment through a loan or lease, especially when you want to keep your liquid cash available for emergencies.

Leasing offers a different path. It’s often easier on your immediate budget because monthly payments are typically lower than loan installments. You aren’t paying for the full value of the machine; you’re paying for the depreciation that occurs while you use it. This keeps your debt-to-income ratio cleaner, which helps if you need to apply for other types of funding later.

Lease vs. Buy: The Tax and Cash Flow Implications

The choice often boils down to the type of lease. Capital leases feel like ownership; you usually own the equipment for a small fee like $1 at the end of the term. Operating leases, or Fair Market Value (FMV) leases, are different. With an FMV lease, you return the equipment or buy it at its current value when the term ends. This is perfect for medical hardware or IT infrastructure where you want to upgrade every 36 months without the hassle of selling old gear. You can explore different equipment funding structures to see which fits your balance sheet best.

When Traditional Equipment Loans Aren’t the Answer

Traditional bank loans aren’t always the fastest or most flexible option. If you’re buying used machinery from a private seller or an auction, a short-term business loan might be the better tool. These loans move faster, often funding in 24 to 48 hours, which is vital when you need to grab a deal before a competitor does.

For seasonal businesses like landscaping or hospitality, revenue-based financing provides a safety net. Instead of a fixed monthly payment that might be hard to hit in January, your payments fluctuate based on your actual sales. You’ll likely see higher equipment financing rates with these alternative products, but you’re paying for the speed and the flexibility to protect your cash flow during slow months. It’s about the cost of the opportunity, not just the cost of the capital.

How to Secure the Most Competitive Rates for Your Business

Securing the most competitive equipment financing rates isn’t just about having a high credit score. It’s about how you present your business’s financial health to a lender. Lenders reward transparency and preparation. If you start preparing 90 days before you need the funds, you’ll have a significant advantage in the underwriting process.

- Clean up your credit early. Review your business credit report at least 90 days before applying. Errors on reports affect 25% of small businesses; fixing these can boost your score and lower your offered rate.

- Define the “use of funds.” Prepare a clear statement that shows exactly how the equipment will generate revenue. Don’t just say you need a new truck; explain how that truck adds $4,500 in monthly billable capacity.

- Gather your documentation. The best equipment financing rates are often reserved for “full-doc” applications. Have your last 3 to 6 months of bank statements and your most recent federal tax returns ready.

- Use a marketplace approach. Comparing multiple offers through a single marketplace prevents your credit score from taking multiple hard-pull hits. This keeps your profile strong while you shop for the best deal.

The Power of a Strong Pro-Forma

Lenders want to see the return on investment (ROI) for the asset they’re funding. If you are buying an $80,000 CNC machine, show them how it pays for itself in 18 months through increased production speed and reduced waste. Use realistic revenue projections based on your current contracts to justify the monthly debt service. A documented ROI can often override a slightly lower credit score during underwriting. This shifts the lender’s focus from your past mistakes to your future potential.

Negotiating Terms Beyond the Interest Rate

The interest rate is only one part of the total cost. You should also look for flexibility in the contract. Ask about prepayment penalties; you’ll want the option to clear the debt early if your cash flow improves unexpectedly. If your business is seasonal, like a landscaping company or a retail shop, request “seasonal payments” to match your cash flow peaks. Watch out for the fine print regarding documentation fees, origination fees, and UCC filing costs. These hidden charges can add 1% to 2% to your effective cost if you don’t account for them upfront.

Ready to see what terms your business qualifies for? You can explore equipment funding options and compare offers without the usual bank-level stress.

Navigating the Marketplace: Finding Your Ideal Funding Match

Finding the right lender shouldn’t feel like a second job. While a traditional bank might offer a competitive rate, their approval process often takes weeks and requires mountains of paperwork. If your credit score doesn’t hit a specific threshold, you’re often met with a hard “no.” This is where a marketplace model changes the game. By looking at multiple providers at once, you gain the leverage to find terms that actually fit your industry’s specific cycle.

Talking to an advisor who understands your world matters. A human-first approach means you aren’t just a file number. You’re a business owner trying to solve a specific problem, like replacing a broken CNC machine or adding a third delivery truck to your fleet. Kredline bridges this gap by connecting you with vetted providers who compete for your business. This process often moves from initial inquiry to funding in as little as 24 to 48 hours. In 2024, nearly 32% of small businesses turned to non-bank lenders specifically for this speed and flexibility.

The goal isn’t just to get a loan; it’s to get the equipment working for you as quickly as possible. When you work with a marketplace, you aren’t limited by one bank’s rigid “appetite” for risk. Instead, you access a variety of capital sources that specialize in different industries, from medical practices to heavy construction. This variety ensures that even if one lender says no, three others might be ready to say yes.

The Kredline Advantage

Comparison is the best way to secure fair equipment financing rates. Applying to multiple lenders individually can hurt your credit score through repetitive hard inquiries. Kredline uses a single application to access a network of vetted providers. We help you decipher the difference between factor rates and APR. You can prequalify for business funding today without a hard credit pull.

Your Next Steps Toward Growth

Don’t let analysis paralysis stall your progress. A 0.5% difference in equipment financing rates shouldn’t stop you from acquiring a tool that generates immediate revenue. If the equipment helps you secure a $20,000 contract, the ROI outweighs the minor interest cost. Have your invoice and four months of bank statements ready. Focus on the utility of the gear rather than just the math.

To get started, ensure you have the following ready:

- A formal quote or invoice from your equipment vendor.

- Your most recent four months of business bank statements.

- A clear plan for how the new equipment will increase your monthly revenue.

Ready to see what you qualify for? You can explore your funding options with Kredline and get a decision in hours, not weeks. Our team is here to help you navigate the 2026 lending environment with confidence and clarity.

Putting Your 2026 Growth Strategy Into Motion

Navigating the current market requires more than just a glance at the numbers. You’ve seen how lender criteria and the specific type of machinery you’re eyeing can shift your total cost. Whether you decide on a capital lease for tax benefits or a traditional loan for long-term ownership, the goal is to keep your monthly cash flow predictable. Modern equipment financing rates are often more flexible than they were in 2021, provided you have the right data to back up your application.

You don’t have to spend weeks comparing bank terms or waiting on slow approvals. Kredline serves as a resource to help you explore your possibilities without any pressure. By tapping into a national network of third-party lenders, you can find terms that actually fit your balance sheet. The process is straightforward; you can complete a no-obligation prequalification and potentially see funding in as little as 24 hours.

See your equipment financing options and prequalify in minutes

Taking the next step is about giving your team the tools they need to succeed today. Your business is ready for its next chapter, and we’re here to help you turn that page with confidence.

Frequently Asked Questions

What is a typical equipment financing rate in 2026?

In 2026, equipment financing rates typically range between 8% and 25%. If your business has a credit score above 720, you’ll likely see offers at the lower end of that scale. Companies with more challenging credit profiles or those in high-risk industries usually land closer to the 25% mark. These figures reflect the current market’s balance between inflation and lending risk.

Can I get equipment financing with a credit score below 600?

You can still secure funding with a credit score below 600, though your options look different than traditional bank loans. Most subprime borrowers move toward alternative lenders offering Merchant Cash Advances or specialized high-rate equipment loans. These lenders focus more on your daily cash flow and the value of the machinery rather than just a three-digit score. Expect shorter terms and higher costs in this bracket.

How long are the typical repayment terms for equipment loans?

Most equipment loans come with repayment terms ranging from 24 to 72 months. Lenders usually try to match the loan’s length with the equipment’s expected useful life. For example, a heavy-duty excavator might get a five-year term; a computer system with a three-year lifespan would likely have a shorter 36-month window. This ensures you aren’t paying for gear that’s already obsolete.

Is equipment financing better than a business line of credit?

Equipment financing is better for long-term asset purchases, whereas a line of credit is designed for revolving working capital. If you’re buying a $50,000 CNC machine, the fixed rate of an equipment loan is usually cheaper. A line of credit is better for covering payroll gaps or buying inventory. Using the right tool for the job keeps your credit lines open for emergencies.

What documents do I need to apply for equipment financing?

You’ll need three main items: your last four months of business bank statements, a formal quote or invoice from the equipment seller, and basic business identification. Some lenders might ask for your most recent tax return if the loan exceeds $150,000. Having these documents ready can speed up the approval process from several days to just a few hours.

What happens if I can’t make my equipment loan payments?

If you miss payments, the lender has the legal right to repossess the equipment since it serves as the underlying collateral. This process is usually faster than a standard business loan default because the asset is clearly defined. Beyond losing the machinery, a default will drop your business credit score by 50 to 100 points. This makes any future borrowing much more expensive for your company.

Are equipment financing rates fixed or variable?

Most equipment financing rates are fixed, meaning your monthly payment stays the same for the entire term. While variable rates exist in some large-scale industrial leases, small business owners typically prefer the predictability of fixed costs. This stability helps you forecast your monthly cash flow without worrying about sudden interest rate hikes from the central bank during your 48-month or 60-month term.

Does equipment financing require a personal guarantee?

Almost all lenders require a personal guarantee, even though the equipment itself acts as collateral. This means you’re personally responsible for the debt if the business can’t pay. Lenders view this as a sign of your commitment to the project. If you’re looking for options, Kredline can help you understand which lenders have the most flexible guarantee requirements for your specific industry.

Article by

Billy Wagner Jr

Billy has 15 years of customer service experience and several years of experience in business loans and merchant services. His passion is helping business owners understand their options and assisting them in making confident decisions around funding and payment processing.